Trustworthy Searchers, SBA Policy, and Underwriting ETA Investments w/ Grant Hensel

Today’s guest is Grant Hensel, founder of Entrepreneurial Capital, a fund that partners with self-funded searchers acquiring small businesses through…

Tags

Looking back at the last two years, we can see that the U.S. healthcare industry responded to the extreme challenge of the Covid pandemic with extraordinary resilience and innovation. While the virus is not fully controlled, the industry is far from the dark spring of 2020, when intensive care units were overflowing and much of the rest of the healthcare system simply froze.

Today, hospitals have new treatment protocols. Outpatient providers have developed new ways to deliver their services safely in person or by video link. And retail pharmacies deployed testing and vaccination capabilities with speed and scale that has never been seen before.

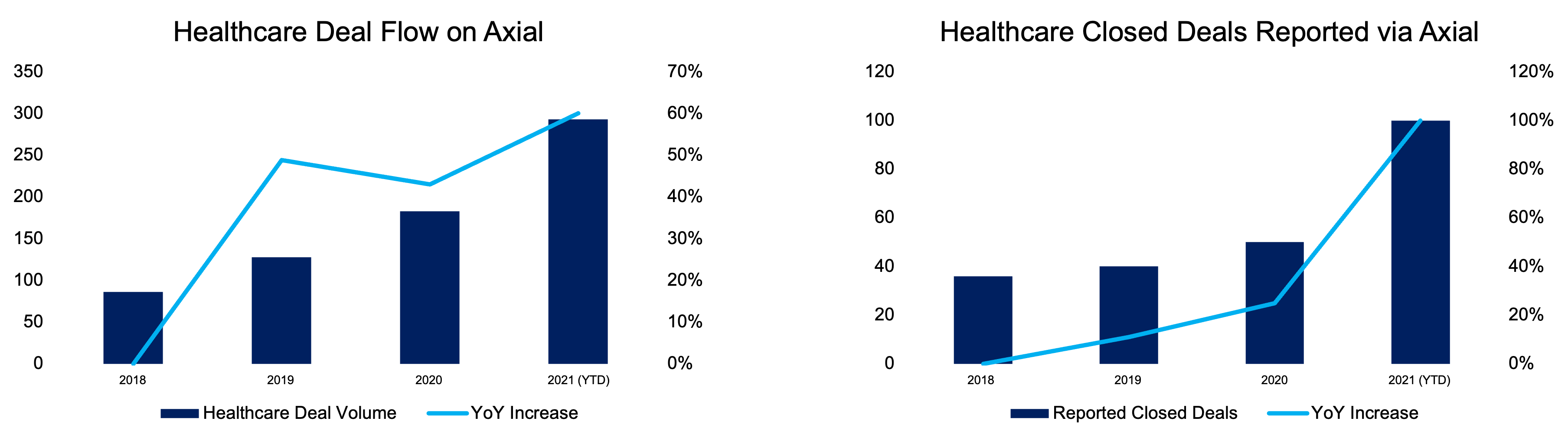

In 2021, investors recognized the underlying strength of the healthcare industry, and indeed identified new opportunities illuminated by the pandemic. Accordingly, merger and acquisition activity in the healthcare market has been strong. New healthcare transactions brought to market via Axial’s platform increased by 60% in the first 10 months of 2021 compared to all of 2020. The number of deals that were reported as closed by members doubled.

In this report, we’ve identified 50 of the top healthcare-focused private equity firms and M&A advisors. (See the methodology section below for our criteria.)

Click here to see the full list

We also talked with experts at four of these top firms to explore the many forces driving healthcare deals in 2021 and what they expect in 2022:

Like this report? It’s the sixth in an ongoing series (click here for the 2021 Business Services Top 50, click here for the 2021 Industrials Top 50, click here for the 2020 Software Top 50, here for the 2020 Consumer Top 50, and here for the 2019 Healthcare Top 50). Email us at [email protected] if you have questions, ideas, or additions.

The vigorous market in 2021 was in part a reaction to the shock of the year before. Like most every other aspect of the economy, healthcare M&A deals froze in the spring of 2020. After tentative resumption later that year, deal-making accelerated this year.

“The term for 2021 is frothy,” says Jonathan Sadock, CEO of Paragon Ventures, a healthcare M&A advisory firm with over 300+ transactions under its belt. “The private equity firms have a lot of dry powder, and they really want to take advantage of the momentum that healthcare has.”

On the other side, the experience of making it through the pandemic appears to have convinced many smaller providers they no longer want to remain independent.

“Covid was a black swan event that changed physicians’ perspective on risk,” observes Rich Searles, Partner at Merritt Healthcare Advisors (#7 on Axial’s Q3 2021 investment banking league tables). “Before, things were going well, even if there were decreasing reimbursement rates and increasing compliance pressure. Then they had to shut down, and they said, ‘I can’t predict what’s going to happen over the next five or ten years.’ It’s been a major driver of sellers.”

Many healthcare business owners were also prompted to try to sell this year by proposals in Congress that could have substantially raised capital gains taxes.

Covid has also thrown a wrench in the traditional methods of valuing companies based on a multiple of trailing 12-month EBITDA. “When we’re representing an investor, we have to normalize what part of the pandemic was temporary,” says Sadock. “Instead of EBITDA, we want EBITDAC, with the C for coronavirus.” This involves looking at the businesses’ trends in 2018 and 2019 then trying to factor out the Covid effect, down and up, in the last two years.

After this sort of adjustment, multiples in the market this year have been as high and often higher as they were before the pandemic, the bankers and investors said

“We didn’t do any platform deals in 2020 because there was too much uncertainty,” says Jon Santemma, Co-Founder of Regal Healthcare Capital Partners, a leading lower middle market PE firm. “Now the multiples are super high. The Fed has been free and easy, so leverage has been high too.” Accordingly, he adds that Regal has been trying to avoid competitive deals in the hottest parts of the market. Instead, it’s focusing on buying smaller providers that it has the expertise to evaluate in a way that new investors to the market don’t.

“A middle market private equity fund may be paying multiples of 10, 12, even 14,” Santemma said. “We can get something done in our end of the market for 8 or 10, and we can do bolt-ons at 5 because they are very small businesses.”

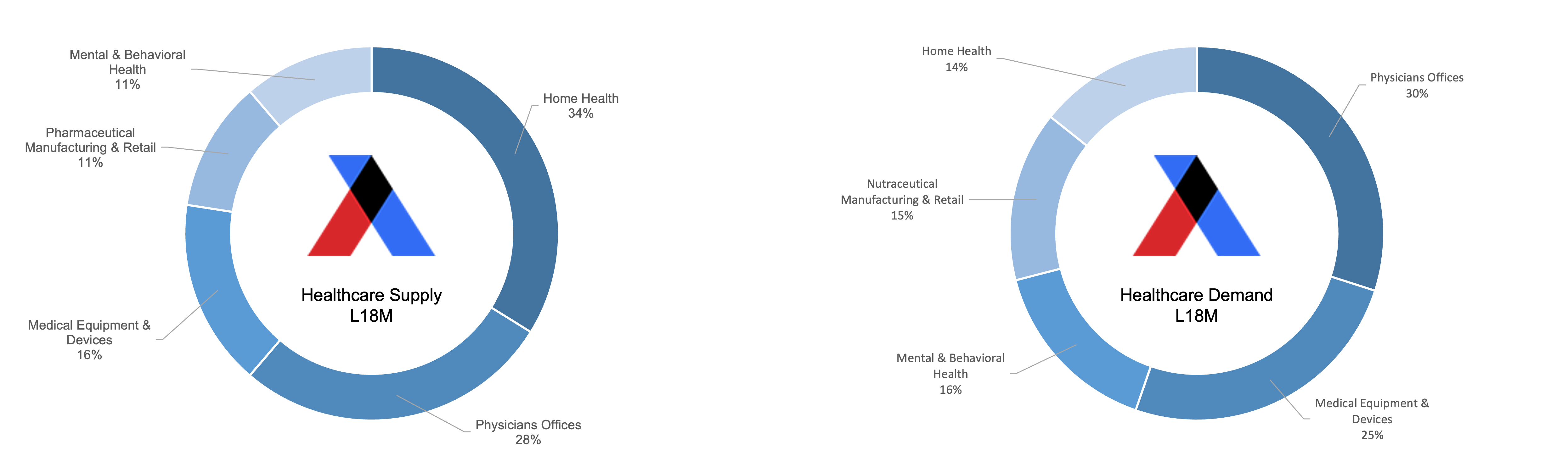

On the Axial network, the healthcare verticals with the most activity from sellers have been “home health, home care & senior care,” “physicians’ offices & care centers,” and “medical equipment & devices.” The top verticals for buyers were “physicians’ offices & care centers,” “medical equipment & devices,” and “mental & behavioral therapy.”

Compared to our 2019 report, home and senior care fell from No. 1 to No. 5 among buyers. The pullback of buyers from nursing homes, in particular, is one of the most significant effects of the pandemic on the M&A market.

“Senior care has gotten pretty ripped up because nobody wants to work in a nursing home post Covid,” Santemma says. The industry has also faced pressure, he adds, from lower reimbursement rates and competition from technology-driven home care.

Investors are also identifying more specialized areas that may see accelerated growth after the pandemic. Sadock points to the experience of ambulatory infusion centers, outpatient facilities where patients can get chemotherapy. They were hurt at first but now are doing better than before the pandemic. “When Covid hit, that business was pretty much shut down and the revenue declined,” Sadock says. “Once things started to open up, what they found was that patients no longer wanted to go to a hospital to get their infusion.”

Mental health is another area where the pandemic has exacerbated need. Investors, however, are still debating whether the best way to fill the demand is through traditional face-to-face therapy, telehealth providers, or other more technology-based approaches.

Nonetheless, it’s getting increasing attention in Washington. Recently, U.S. Surgeon General Vivek Murthy called adolescent mental health problems a “public health crisis” and called for more prevention and treatment. More funding for behavioral services should create additional opportunities for providers.

“The country is facing a mental health issue, with rising overdoses and now Covid,” says Brett Lacher, VP at Latticework Capital, a Dallas-based PE firm with over $140M of AUM. “It’s a big cost to the system, with people going to the emergency room or prison. So there is bipartisan support for trying to do something about it.”

As in recent years, private equity has been driving most of the consolidation in the healthcare industry. Typically, a fund will buy one or two well-run providers in a sector to create a platform from which to add in multiple local practices or facilities.

Some of these deals have worked out remarkably well, and that’s drawing even more capital to the market. A dramatic example is Regal’s acquisition of 75% of Thriveworks, a chain of mental health clinics, in November 2019. In August, Regal sold about one-third of its stake in a recapitalization led by Wellington Management valued at 1.2 billion, a 29X return in less than two years. With results like that, it’s no surprise that Regal, itself less than four years old, closed its third fund recently with $415M invested.

Strategic buyers are emerging slowly in many sectors of the healthcare industry. Hospital systems in some parts of the country are buying up physician practices and other service providers. United Healthcare’s Optum unit had bought providers in urgent care, ambulatory surgery, and other specialties. CVS may evolve into another strategic buyer. It recently announced it would close 900 traditional drug stores over the next three years while building out facilities with primary care providers.

Heading into 2022, healthcare investors and bankers generally expect the vigorous deal making and high multiples to continue.

The specter of inflation isn’t a direct concern. Healthcare prices have been rising faster than the rest of the economy for years. If the Fed significantly raises interest rates, it will doubtless slow the pace of new deals and could endanger the most precisely leveraged of the existing roll-ups.

A potentially greater worry is the labor shortage, which has hit the healthcare industry particularly hard. Companies whose growth may be limited by a staff shortage may see lower valuations.

“Now one of our top questions for a company is employee turnover,” Santemma says. “If it’s high, we ask if it is something we can help with. If it’s going to be high, we will bake higher costs for more generous benefits and more flexible work schedules into our financial projections.”

The omicron variant, at least at this early stage, is not having much of an impact on the healthcare M&A market.

“Even if we have some softness because of another surge in Covid, I think we’ve figured out how to operate in this new normal,” Lacher says. “That gives me some comfort.”

To conclude, we’re excited to present Axial’s 2021 Top 50 healthcare Investors and M&A Advisors, whose work both advising and partnering with healthcare business owners deserve recognition.

Axial’s Top 50 Healthcare list was generated based on a weighted formula leveraging private transaction data from the Axial platform. Metrics in the formula include the number of healthcare deals brought to market via Axial (sell-side), how much interest those deals generated from Axial’s buy-side member base (sell-side), the number of specific healthcare-focused investment mandates created in the platform (buy-side), and the number of healthcare deals that progressed through the deal funnel achieving an executed LOI or successfully consummated transaction (buy- & sell-side).