The Advisor Finder Report: Q2 2026

Welcome to the Q2 2026 issue of The Advisor Finder Report, a quarterly publication that surfaces the activity occurring on…

Tags

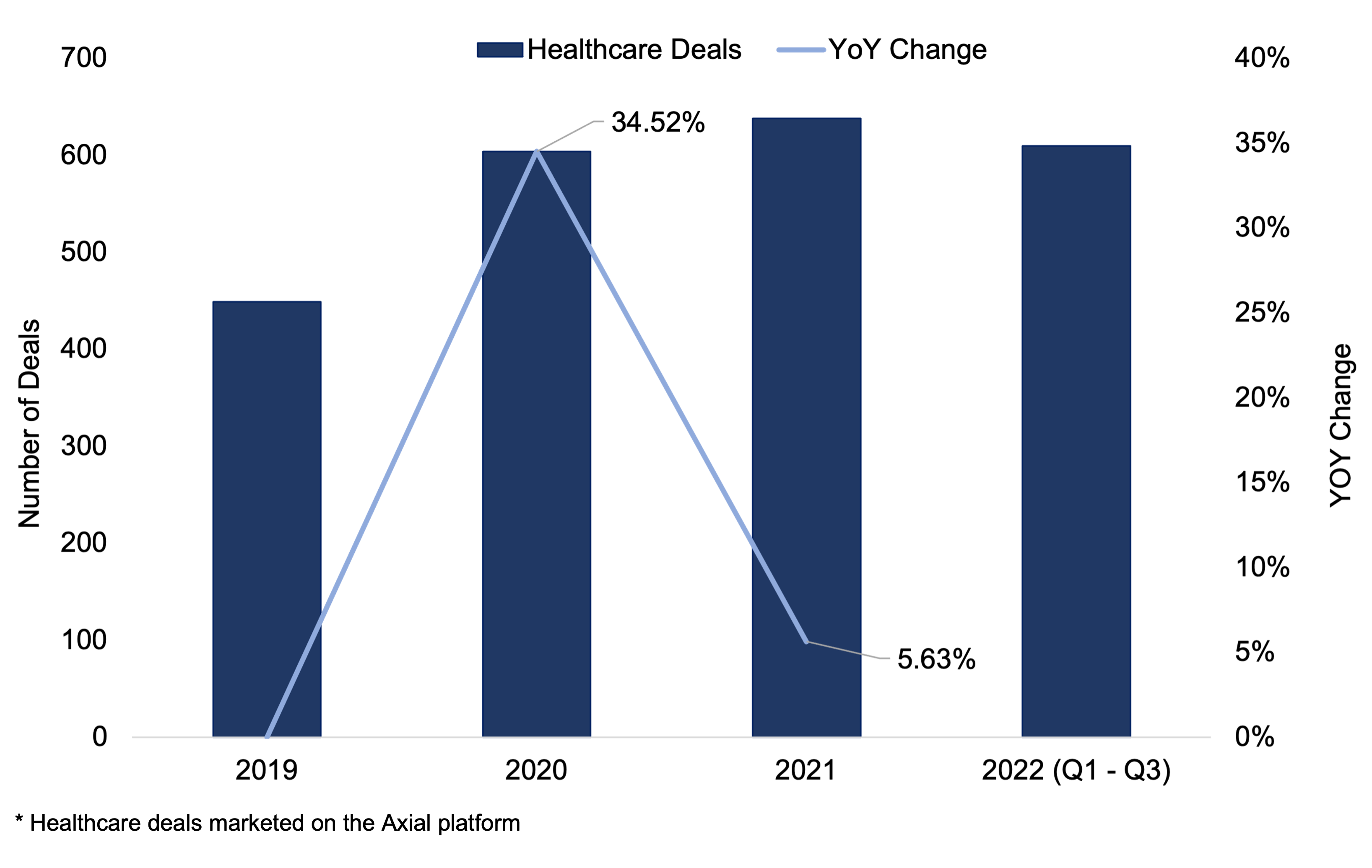

By all accounts 2021 was a banner year for healthcare M&A. According to KPMG’s Q3 2022 healthcare M&A report, “more than 600 deals were announced or completed per quarter” this year. Some of the most robust activity occurred in sectors such as healthcare IT and digital health, health care systems and payor and pharmacy benefit management (PBM) targets, the firm noted.

But how is 2022 faring in comparison? In a nutshell, not great. M&A volume in the healthcare space continued to plummet in the third quarter this year compared to the first two quarters, and “was far below any quarter in 2021”, KPMG reported. The number of healthcare deals conducted on Axial’s platform dropped almost 29% in 2021 compared to 2020. All signs indicate a “mild recession” starting by the end of the year, and KPMG’s experts anticipate interest rates rising over the next two quarters.

On the M&A front, hospital systems are likely to see fewer suitors going forward, buyers and sellers may have more difficulties agreeing on deal terms since acquirers will be more selective — and sellers may balk at valuations that come in lower than a year ago, KPMG noted.

“As with many other industries, we saw valuations in healthcare reach a peak in 2021 and early 2022,” stated Scott Mitchell, managing director of investment bank SDR Ventures, in a recent healthcare-focused survey conducted by Axial. But Mitchell predicts multiples will “dip down to pre-COVID levels, and possibly further for the first half of 2023, until there is some more clarity on interest rates and the recessionary environment.”

Axial recently surveyed its 2022 top 50 healthcare firms about current trends they are seeing in the changing healthcare market, along with predictions on what’s to come in 2023. This report cites seven of those leaders, a mix of buy- and sell-side firms:

Adam Ginsburg, Vice President, Salt Creek Partners

Brett Lacher, Principal, Latticework Capital

Dan Nguyen, Partner, Abacus Investments

Gary Grote, Managing Director, Bridgepoint Investment Banking

Jonathan Sadock, CEO & Managing Partner, Paragon Ventures

Scott Mitchell, Managing Director, SDR Ventures

Shawn Earl, Founder & President, Pinnacle Pharmacy Group

Despite some gloomy news about the state of the healthcare market, more than half of the sources surveyed said deal volume is actually increasing, and two-thirds noted that valuations in healthcare deals remain high.

High valuations are driven by demographics, namely an aging Baby Boomer population, medical and technological advancements, and stability of revenue, among other things, sources say; and as such, the outlook for healthcare M&A remains strong in the near term. “Prospective buyers still have a high capacity to drive M&A activity and valuations post-pandemic,” said Ginsberg. “Reputable brands and product portfolios, strong fundamentals, and growth outlook positions will always be attractive, and the institutional barriers for new entrants means established companies will always be in favor positions.”

What’s more, stated Sadock, “Healthcare has always had inherent reimbursement risks and challenges, but the over-reaching opportunities for population health will continue to enhance the valuation metrics for those deploying a strategic M&A mandate.”

So why are healthcare deals dipping in some subsectors? By and large it depends on the sector and on the “risk/return appetite of investors”, said Nguyen. Strategic acquirers in particular may face potential headwinds ahead, due to rising interest rates, lower deal volume with sellers pulling out, and “lower cash flow conversion in core businesses due to turnovers,” he added.

Some strategic acquirers are facing challenges in the healthcare sector partly due to regulatory and reimbursement headaches along with other factors. “Strategics who focused on operations and technology will face slowing, blowing winds,” Earl noted.

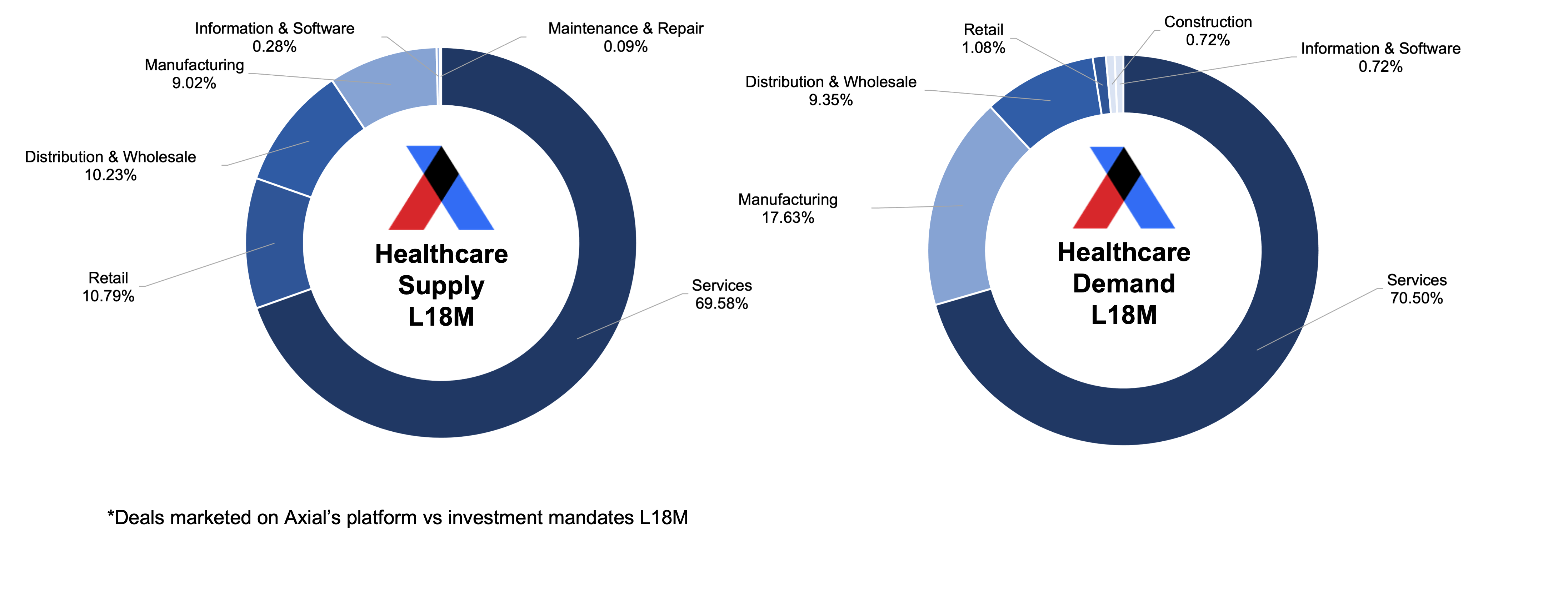

According to data from Axial, more than 70% of all healthcare deals marketed on Axial’s platform were in the services subsector over the past 18 months, followed by manufacturing, and distribution and wholesale on a much lesser scale.

Despite some ups and downs in the industry, the bottom line seems to be this: “Similar to your heartbeat, healthcare businesses always have periods of fluctuation,” Sadock summarized. “These peaks and valleys reflect the health of these businesses.” Some subsectors — such as ventilator manufacturing and telemedicine – saw huge growth during the pandemic, while other sectors are now “returning to their pre-pandemic growth trends,” he said.

Many business owners in the healthcare sector struggled in 2022, largely due to the current economic crisis with rising supply and labor costs. “A lot of owners/founders are having difficulties with staffing and operations,” said Earl. “The mentality is less than optimistic.”

As we head into 2023, business owners are trying to remain steadfast and to maintain their core businesses, reduce turnover and improve their margins, Nguyen noted. “If they can achieve those fundamentals, they should weather this storm,” he said. “We believe that this is the time that will separate great business from mediocre business.”

This weakened mentality could spur some owners toward M&A. “Owners are seeing more uncertainty ahead, which might push more individuals to want to sell in the next six months and be more open to a structured deal at a more reasonable valuation than riding through another recession on the heels of recently getting through COVID,” Lacher predicted.

Investors on the Axial platform are bullish on numerous subsectors: homecare, dental, pharmaceutical services, staffing, geriatric care services, dermatology, cardiology, behavioral health, and digital and telemedicine. But some are bearish on brick-and-mortar clinics, diagnostics, optometry, primary care, travel nurse businesses, and hospitals. “Large healthcare systems will continue to see margin pressure with staffing, inflation, and alternative delivery methods stealing business,” Grote said.

Others agree that hospitals could face pressures. “Every day I receive emails talking about a hospital closing,” Earl said. “I predict we will see an evolution in the sector, focusing on profit-generating services.”

New Year, New Challenges, New Opportunities

New Year, New Challenges, New OpportunitiesInvestors are cautious about 2023, but still optimistic. “We’re already seeing rising interest rates affect deals, mostly in increased due diligence around lending,” Ginsburg said. As a result, buyers” need to have high levels of confidence in the forecasts and growth strategies underpinning the opportunities,” and confidence in “the abilities of management teams to deliver on those strategies,” he noted.

What’s more, lenders are more stringent now, with fewer deals being completed, which could impact M&A volume temporarily. This lending environment will cause private equity to “be more selective on their targets,” Ginsburg added. And private equity firms will likely continue looking for targets in the coming months, “especially deals for under $200 million,” KPMG predicted.

“Lenders are concerned about the default rate,” Nguyen said. “They have increased their due diligence effort[s] in the net asset and cash flow of the business.”

Telehealth and healthcare IT are two sectors that may weather this storm just fine. “The pandemic brought rapid and increased adoption of telehealth, and shined a brighter light on the importance of technology in healthcare to explore new delivery channels,” Grote said. “I would expect increased reimbursement for telehealth to become permanent.”

One thing is clear, KPMG noted in its Q3 recap: The need for healthcare isn’t going away anytime soon, which bodes well for healthcare M&A overall. “The industry’s overall strengths will endure–people need care, drugs, and medical devices in good times and bad–but some subsectors should see more action than others,” KPMG reported.

Like this report? It’s part of a quarterly series (click here for the 2022 Consumer Top 50, click here for the 2022 Industrial Top 50, and click here for the 2022 Software Top 50).

Axial’s Top 50 healthcare list was generated based on a weighted formula leveraging private transaction data from the Axial platform.

Metrics in the formula include: