Alex de Pfyffer and Ross Porter’s Journey from Self-Funded Search to a $220M Committed Fund

Today’s guests are Alex de Pfyffer and Ross Porter, Co-Founders of Heritage Holding, an investment firm that has completed nearly…

Tags

It turns out that there is more to the American economy than cubicle culture and coffee bars. Manufacturing employment started rising in 2010 after a 30-year decline. And the disruptions in the global supply chain have redoubled interest in domestic production.

The blue-collar revival can clearly be seen in Axial’s latest review of industrial merger and acquisition activity in the lower middle market.

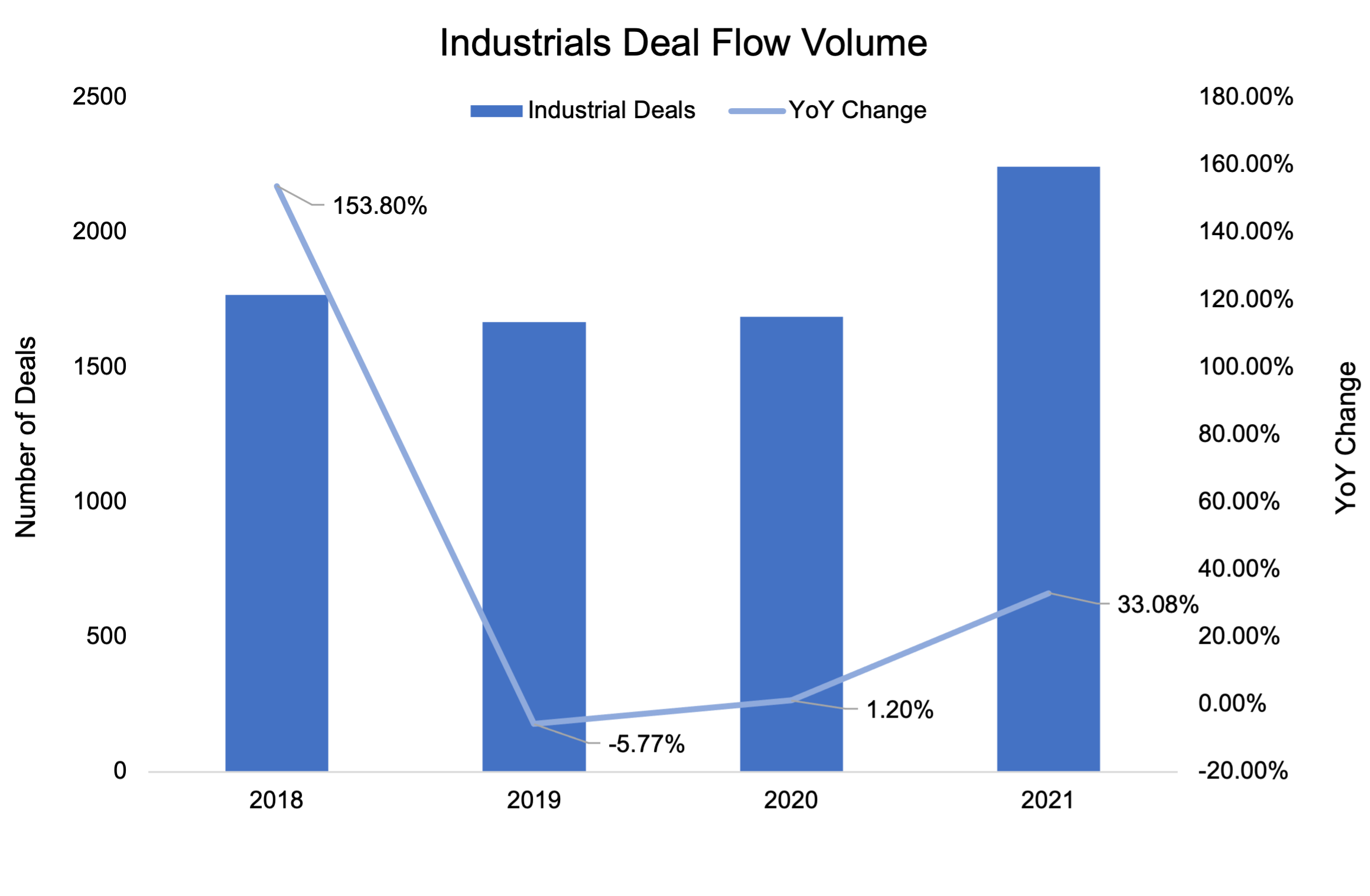

Activity in the industrial sector has been vigorous. In 2021, new industrial transactions brought to market via Axial’s platform increased by 33%. In the first three months of 2022, new transactions increased by 1% compared to the same period the year before.

“There is a renaissance in manufacturing,” says Scott Bushkie, the managing partner of Cornerstone Business Services of Green Bay, WI. “With everything happening in the world, there is a lot of interest in making things in America again.”

Cornerstone is one of the top 50 private equity firms and M&A advisors active in the industrial market that Axial has identified in this report. (See the methodology section below for our criteria.)

Click here to see the full list

For commentary, we have reached out to leaders at several of the top 50 firms to explore the many forces driving industrial deals:

Like this report? It’s part of a quarterly series (click here for the 2022 Software Top 50, here for the 2021 Healthcare Top 50, and here for the 2021 Business Services Top 50). Email us at [email protected] if you have questions, ideas, or additions.

These experts consistently say the pace of industrial deals has been brisk.

“Last year was the best year we’ve had on record, and we did more deals in the first four months of this year than we did last year,” Bushkie says.

Interest from buyers is surging. Last year, there were an average of 43 buyers who signed nondisclosure agreements to look at each deal, up from 30 just two years before. And the average deal received nine bids in 2021, up from 2.5 in 2019.

“It’s a perfect storm for sellers,” Buskhie says. “There’s so much competition out there for good quality deals that they can maximize their value.”

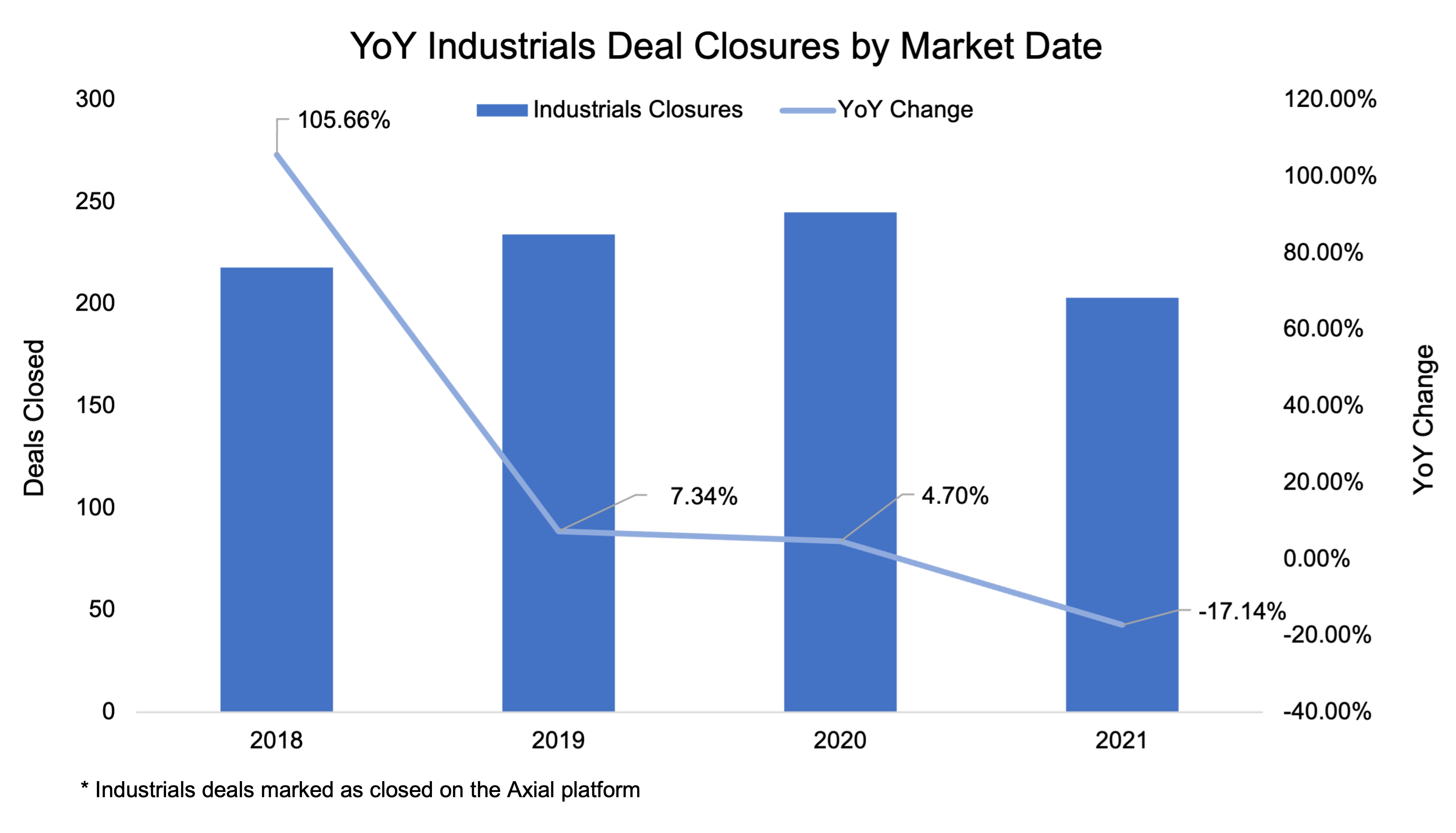

That said, there may be a bit more testing the waters by business owners who aren’t sure they want to sell. The number of deals that were marketed on the Axial platform in 2021 that closed fell by 17% compared to the same measure for 2020.

Much of the surge in demand for industrial companies is now coming from financial buyers.

“Private equity continues to rule the day, and family offices are becoming more and more prevalent,” Short says. “You have strategic buyers in every deal, but they are not nearly as prevalent as they were ten years ago.”

Over that period, the multiples that private equity firms are willing to pay for industrial companies has increased as well. “Go back seven or eight years ago, and private equity was often coming in second place,” Short says. “They had promised their investors a 25% return, and they didn’t win auctions. Then the world changed on a dime. They said we can deliver 17% returns. That’s still a lot, and we can get deals done.”

After the disruptions from Covid, some financial investors see an opportunity to get ahead of the demand for manufactured goods made in the United States or North America through the United States-Mexico-Canada Agreement (USMCA).

“Made-in-America and USMCA supply chain is becoming more important than ever,” says Slonim, who manages a New York lower middle-market private equity fund. “We’re highly focused on whether companies we look at can do the high-volume work needed by customers who are re-shoring.”

At the same time, existing industrial companies are more interested in growing through acquisition than ever. Most have strong balance sheets, and unless they have been crippled by supply chain problems, they are very profitable.

Their challenge is expansion, so they are turning to acquisitions to get around labor shortages and to secure their supply chain.

“There is a growing trend of ‘onshoring’ or ‘near shoring’ that will continue to drive demand from strategic buyers who are looking for more reliable supply chain participants for core components,” says Goodrich.

In the industrial sector, sellers are driven by the same forces as in the rest of the lower middle market. Aging baby boomers are looking to exit if they don’t have a family member to take over their businesses.

“We are seeing that family owners and founders have reset personal priorities coming out of the pandemic, following an unprecedented bull market, there has been a renewed interest in exploring a sale, Goodrich says. “The uncertainty in the markets (inflation, interest rates, and global turmoil) and operating challenges (labor, supply chain, and taxes) have only accelerated this trend.”

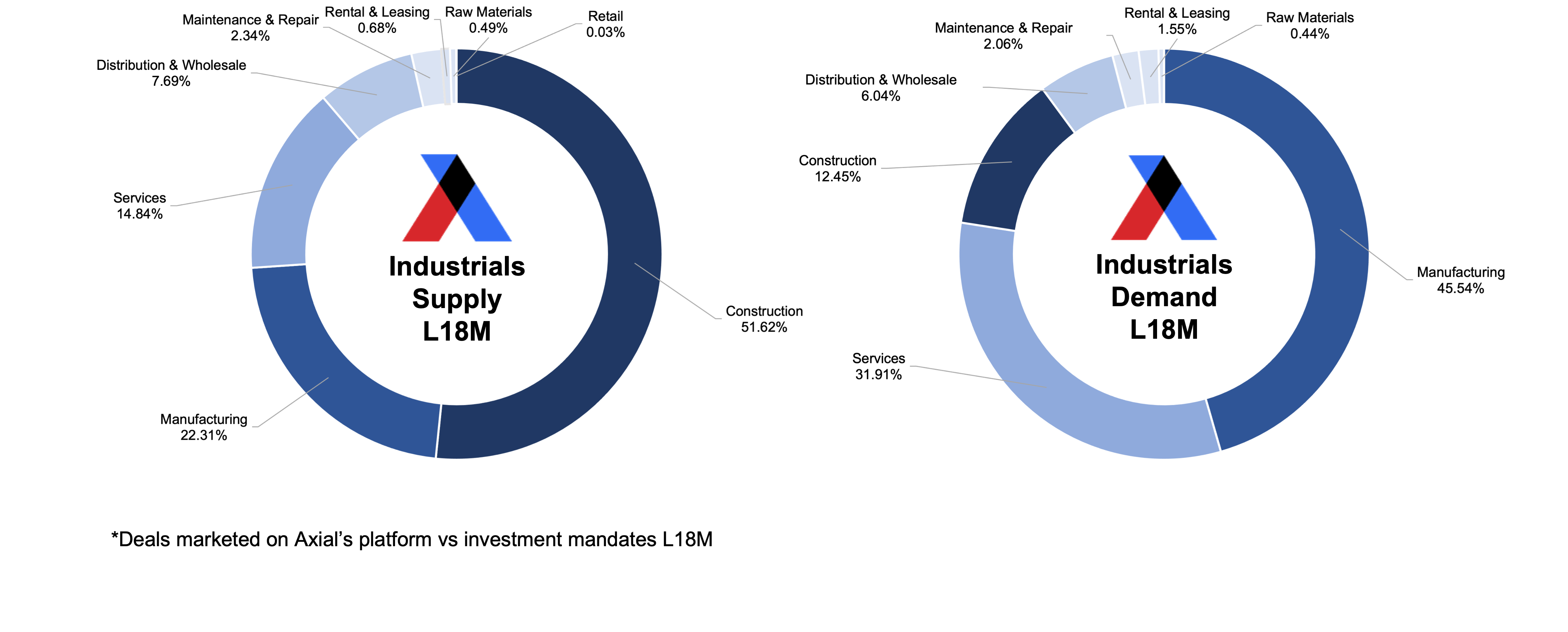

On the Axial network, the industrial vertical with the most activity from sellers over the last 18 months has been construction, followed by manufacturing and industrial services. Construction, in fact, has consistently represented about half the deals brought to market on Axial for the last five years.

The interests of buyers are very different, however. The highest demand was for manufacturing companies, which represented 45% of the interest in the last 18 months. Industrial services followed with 32%. Only 12% of the expressions of interest were for construction deals.

Buyers are very selective about the types of acquisitions they make in the construction sector, explains Short. “They don’t want to pay much of a multiple for general contractors because they are only as good as their last shot. There is no repeat business. Every job has to be bid,” he says.

There is somewhat more interest in subcontractors, he adds. “And there are a lot of buyers for building materials companies. They are a manufacturer with repeatable business spread across a bunch of customers,” Short says.

For manufacturers, the greatest interest is in companies that can differentiate their products from lower-priced commodity goods produced overseas.

“We get buyers all the time looking for companies where there’s some value add, or it’s a bit more complex or highly engineered,” Buskhie says.

Most of the bankers and investors said valuations for industrial companies are at or near their high-water mark. What’s less clear is whether multiples will fall as public markets have been doing.

Some argue that turmoil among larger firms will increase demand for middle-market companies.

“I believe that middle-market private equity will become a more attractive investment class for investors seeking a safe haven from more volatile asset classes,” says Luchow.

Others suggest the global disruptions will inevitably slow down all activity.

“The macroeconomic and geopolitical environment is creating a level of uncertainty in the market right now,” says Fridman. “Investors are likely to tread more cautiously as they assess the risk profile of potential deals.”

The pent-up desire to consummate deals, both by buyers and sellers, may keep volume and values up for a while.

“We are at the market peak, but it will take some time for sellers to recalibrate their valuation expectations,” says Hild. “There is still a lot of PE and strategic capital looking for quality companies. Sellers had a strong 2021 performance, but they are that multiples will decline as interest rates increase.”

Even as the Federal Reserve sharply increases short-term rates, it’s not clear yet how this will influence the capital available for industrial acquisitions.

“We are seeing senior lenders become slightly more conservative in light of the current economic outlook,” Goodrich says. “There is still ample capital to fund M&A.”

Indeed, Short says he sees banks that are raising their rates on business loans at only half the pace of the Fed increases.

“Interest rates are kind of a false signal at the moment because there’s so much money out there,” Short says.

Inflation, so far, has not been a huge drag because most companies have the pricing power to pass their increased costs to their customers. That’s even true in areas dependent on markets that have been disrupted by the war in Ukraine.

“In my world, it is primarily steel prices that have been affected by the war, and companies are finding other sources besides Russia,” says Short. “For trucking companies, obviously fuel is a big deal, but we still have done deals for a number of large trucking companies.”

Even as dealmaking continues, the question of an eventual slowdown looms.

“When we hit this next recession, which we all know is coming, values will come down, and volume will come down,” Buskhie says. “Until that, we’re on a rocket ship.”

To conclude, we’re excited to present Axial’s 2022 Top 50 Industrial private equity investors and M&A advisors, whose work both advising and partnering with industrial business owners deserve recognition.

Axial’s Top 50 industrial list was generated based on a weighted formula leveraging private transaction data from the Axial platform. Metrics in the formula include the number of industrial deals brought to market via Axial (sell-side), how much interest those deals generated from Axial’s buy-side member base (sell-side), the number of specific industrial-focused investment mandates created in the platform (buy-side), and the number of industrial deals that progressed through the deal funnel achieving an executed LOI or successfully consummated transaction (buy- & sell-side).