Top 25 Lower Middle Market Investment Banks | Q2 2026

Axial is excited to release our Q2 2026 Lower Middle Market Investment Banking League Tables. To compile this list, we…

Tags

According to Harrison Phillips, analyst at Viridian Capital Advisors, “the legalization of cannabis is one of the greatest social, economic, and political movements in the past century.”

As the legal cannabis industry grows, opportunities for investment professionals increase. But how do investors manage risk in a sector that is constantly evolving?

Viridian Capital Advisors is a strategic and financial advisory firm dedicated to the cannabis industry. We asked Phillips to share his insight on the industry’s unique opportunities and challenges, potential for growth, current valuations his firm is seeing for cannabis-related businesses, and more.

“Estimates for the size of the cannabis black market vary, but consensus puts the value of cannabis consumed yearly in the United States around $35 billion. The cannabis industry shows growth characteristics similar to the internet industry in the 1990s, but demand for the internet had to be created as it was rolled out. The billions of dollars of existing demand for cannabis can be captured as states legalize the sale of cannabis products. Currently, legal cannabis sales are around $5 to $9 billion per year (estimates vary widely as California represents approximately 50% of the overall industry but lacks a comprehensive seed-to-sale tracking system to accurately measure sales of cannabis in the state), representing only a fraction of the overall demand in the country and leaving much room for growth.

The cannabis industry shows growth characteristics similar to the internet industry in the 1990s, but demand for the internet had to be created as it was rolled out.

“The year 2016 will be a critical year in the process of developing the legal cannabis industry. The United Nations General Assembly Special Session in April will be readdressing the world’s stance on illicit drugs, including a potential reclassification of cannabis under the Single Convention for Narcotics. Furthermore, the U.S. Drug Enforcement Agency (DEA) has stated that it will be reconsidering the rescheduling of cannabis within the first half of 2016. Later in the year, numerous states will be voting on ballot initiatives to either legalize medical or recreational cannabis, likely opening up three to five new states with medical cannabis as well as five to nine new states with recreational cannabis (most of which have medical cannabis regulations already).”

“Growth over the next five to ten years will depend largely on the timing of new states creating legal and regulated cannabis markets. The more states the enact medical or recreational markets and the faster these regulations lead to active markets (i.e. the shorter the time between the law being enacted and sales beginning), the faster the industry will grow. Estimates for the size of the cannabis industry in five years’ time (end of 2020) are between $15 and $25 billion, with most estimates falling near $20 billion.

“Estimates for the long-term size of the cannabis industry ten years from now, assuming most if not all states create regulated cannabis markets and the federal government changes its stance to allow for the creation of a national cannabis industry with interstate commerce, range from $15 billion to over $50 billion, with consensus falling around $35 billion. These figures only cover the sales of cannabis and cannabis-derived products; when including ancillary products and services provided to and supporting the cannabis industry, estimates for the total value added to the economy range from about $75 billion to over $100 billion.”

“Some of the biggest challenges we continually see in this space have to do with the people. While the cannabis industry is coming out of the black market and “into the light”, there remain several characteristics from the black market. Individuals previously engaged in illegal cannabis activities, as well as opportunists seeking to make a quick buck through stock scams or other less-than-legal initiatives, have made their way into this space. Because of this, finding and vetting management remains one of the most important facets in due diligence. However, while there have been some less than savory individuals and groups in the industry, the industry is steadily becoming more professional as more sophisticated investors and operators enter the industry to capitalize on the high prospects for growth and profits.

While the cannabis industry is coming out of the black market and “into the light”, there remain several characteristics from the black market.

“Also, because cannabis is still illegal under federal law, companies in the cannabis industry are burdened with tax, banking, and interstate commerce issues. With regard to taxation, companies in the cannabis industry are prohibited from deducting expenses under Internal Revenue Service Internal Revenue Code 280E covering monies earned or spent relating to unlawful conduct. This imposes an extra financial burden on companies and reduces margins.

“Furthermore, because of banking regulations through the Federal Reserve, most cannabis companies are not able to get or maintain a bank account. While banks are allowed and able to provide depository services to cannabis companies, the extra burden of proving the monies are not tied to illegal activity as well as the relatively small size of the industry make the banks’ costs of holdings these accounts outweigh the benefits. As such, cannabis companies are stuck dealing largely in cash, necessitating additional security and risk management, adding additional costs to doing business in the space.

“On top of this, interstate commerce is prohibited in the cannabis industry. Cannabis and cannabis products from legal state markets must remain in that state and cannot be shipped to other states as crossing state boundaries would constitute interstate commerce and fall under federal jurisdiction. This has greatly limited the scalability of cannabis companies as well as the proliferation of brands in the space.”

“We typically engage in a top-down approach with regard to political and regulatory risk whereby we investigate the current rules and regulations as well as their trends in order to identify states that appear to be more friendly to cannabis businesses. There are several states that have enacted cannabis regulations that are friendly to businesses while being stringent enough to limit risk of federal intervention. The federal government has stated that companies doing business in states in which cannabis is legal and whose regulatory framework is stringent enough to adequately prevent infiltration by the black market are free to continue doing business without fear of DEA or other agency intervention.

“We do not see any existential threat to the cannabis industry as a whole. Popular support for both medical and recreational cannabis use continues to rise in the U.S., and more politicians are following up on the trends in the populace by coming out in support of cannabis, or, in the very least, additional research into the plant and its effects. With Pennsylvania enacting medical cannabis regulations, 24 states, in which over half of the U.S. population lives, have legalized medical marijuana. We expect additional states to legalize medical and/or recreational cannabis markets, and, eventually, for the federal government to remove cannabis from Schedule I to either Schedule II or III, enabling cannabis to be regulated and controlled at the federal level as well as allowing interstate commerce and the establishment of a truly national cannabis industry.”

“Originally, the vast majority of funding in this space came from friends and family of operators standing up legal cannabis businesses. This was largely due to the uncertain nature of the cannabis industry as well as the relatively small size of the industry at its beginnings. As more states have established legal cannabis markets, more sophisticated investors, such as ultra-high-net-worth individuals, family offices, venture capital firms, and private equity firms have begun investing in the space. While these more traditional sources of capital are beginning to enter the space in greater numbers, the federal illegality of the cannabis industry as well as the reputational risk associated with being involved in the space has kept many would-be investors from moving forward.

“Several companies have slowly started approaching the industry. The Scotts Miracle-Gro Company has invested in hydroponics companies whose products are utilized by the cannabis industry, but has not yet made a direct investment in a cannabis company. Tobacco farmers in states such as Kentucky are beginning to switch some of their fields from tobacco to cannabis or hemp. Furthermore, several biotechnology and pharmaceutical companies have begun investigating cannabinoids as potential drug candidates.

“There are essentially two categories of companies in this industry in terms of investment: those companies “touching the plant” and those providing ancillary products and services (the “picks and shovels”) to the prior group. Most investors are more comfortable investing in companies not directly engaging the cannabis plant. This is partly due to the reasons described above, namely reputational risk and federal illegality. These companies include lighting manufacturers, consulting companies, soil and nutrient providers, software companies, real estate investment firms, and others.

“As the industry has begun to mature and investors have watched state-legal businesses generate profits and tax revenue without harming their communities, more groups have begun investigating and making investments into companies “touching the plant”. Some cultivators, retailers (medical and adult-use), and infused product manufacturers have begun to differentiate themselves from their competition and have steadily attracted more investment from investors with greater risk tolerance. Biotechnology and pharmaceutical companies are generally considered to be where the greatest value lies in the long-run, but researching, developing, and commercializing cannabis drugs will take time, especially as the plant’s classification as a Schedule I controlled substance limits the ability to conduct clinical investigations.”

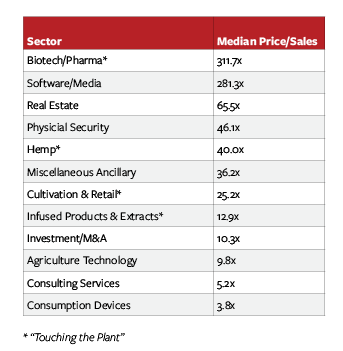

“Valuation multiples for cannabis companies vary wildly, not only between respective sectors in the industry but also between legal jurisdictions (i.e. between different states with legal cannabis as well as between different cities within those states).

“We at Viridian have compiled an Index of 50 publicly traded cannabis companies, separated into two groups (Ancillary Products & Services and “Touching the Plant”) containing 12 sectors total. Below is a chart detailing trailing twelve month (TTM) price-to-sales multiples for the sectors in our Index as of Q1 2016:

“Many biotechnology and pharmaceutical companies that are investigating cannabinoids and other cannabis-based molecules as prospective drug candidates have zero revenues but are trading at market capitalizations of tens of millions of dollars (in some cases more than $100 million) due to the anticipated value of future growth opportunities and value of cannabis therapeutics.

“The two largest companies in the biotech/pharma sector, GW Pharmaceuticals plc (NasdaqGM:GWPH) and Insys Therapeutics, Inc. (NasdaqGM:INSY), are outliers from the majority of the companies in this sector and trade at market caps above $1 billion. Both GWPH and INSY are more established companies (GW Pharma a pure cannabis play while Insys is an opiate drug manufacturer with cannabinoids as a secondary focus), and each generates tens of millions of dollars in revenue each year.

“The valuations for the Software/Media, Real Estate, and Physical Security sectors are only based on a limited number of companies so may not be accurately representative of the sector as a whole. For the rest of the industry, “Touching the Plant” sectors (Biotech/Pharma, Cultivation & Retail, Hemp, and Infused Products & Extracts) tend to engender higher valuation multiples than companies providing Ancillary Products & Services.”

—

Harrison Phillips currently assists with the firm’s M&A and fund raising assignments. His prior experience includes asset classification, database management, and spreadsheet programming at Black Diamond Performance Reporting and product research at Brower Financial Group. At University of North Florida, where Mr. Phillips received a B.B.A. in Finance, he held the position of co-manager and statistician of their student-run investment fund, Osprey Financial Group.