Alex de Pfyffer and Ross Porter’s Journey from Self-Funded Search to a $220M Committed Fund

Today’s guests are Alex de Pfyffer and Ross Porter, Co-Founders of Heritage Holding, an investment firm that has completed nearly…

Tags

Industrials remains the dominant sector on Axial, accounting for 27% of all deals brought to market via the platform last quarter and 40% of Axial closed transactions so far in 2026.

Today, we’re excited to release the 2026 publication of the Top 50 Lower Middle Market Industrials Investors and M&A Advisors, a list featuring Axial’s 50 most active and sought-after members who specialize in industrials transactions over the past 12 months (methodology in the footnotes).

In addition to celebrating these Top 50 members, this feature includes reflections and insight from our recent 2026 Industrials M&A Outlook survey.

Congratulations to these members for their dealmaking achievements!

We asked deal professionals whose firms are featured on this list to share insights on the general industry landscape, valuation expectations, the biggest challenges and opportunities shaping the industrials market today, and activity across key sub-sectors, including:

Survey responses indicate that deal activity in the industrials sector remains concentrated in sectors tied to essential services, infrastructure, and electrification trends. HVAC led all responses by a wide margin, followed by Construction & Engineering, Electrical Equipment, and Machinery & Equipment. Energy and Aerospace & Defense also ranked prominently, reflecting continued interest in businesses benefiting from infrastructure investment, manufacturing demand, and government spending trends.

At the sub-sector level, respondents most frequently pointed to data center build-outs, power infrastructure, electrical contracting, and residential service trades. HVAC, plumbing, mechanical services, facility services, and preventative maintenance businesses were repeatedly cited as active areas of the market, alongside automation, aerospace and defense manufacturing, and other mission-critical industrial services.

HVAC multiples carry the widest spread of any sector this year, with respondents consistently pointing to revenue mix and end-market exposure as the primary valuation drivers. Rob Chepak of TREP Advisors anchors the typical range at 5x to 9x adjusted EBITDA, noting that “service and maintenance heavy beats installation and new construction every time.” Josh Gladtke of Good Hope Advisors similarly cited service mix as the biggest determinant of valuation, particularly for companies with maintenance-heavy revenue profiles.

The highest valuations within the category appear concentrated in specialized niches tied to infrastructure and AI-related demand. Scott Mitchell of SDR Ventures cited commercial HVAC maintenance businesses trading at 10–15x, while data center cooling specialists can reach 12–20x multiples.

Not every respondent agreed that double-digit outcomes are becoming commonplace. In smaller HVAC businesses, John Murray III of Sligo Strategies noted that “everyone shoots for that 10x but just not happening lately it seems,” adding that “companies asking 10x usually trade for 8x.”

Those who named A&D as the top multiple sub-sector pointed to one primary theme: accelerated defense spending. Joe Bieshelt of The Venture North Group sees multiples moving above the 10x range, attributing the premium to global geopolitical instability and an “overt posture of the U.S. to invest further in large defense projects.” Michael Schuster of Cross Keys Capital placed quality LMM defense businesses at “high single-digit multiples,” while Keith Wegen of Flatirons Capital Advisors anchored the floor at 8x+, citing the broader macro environment.

Industrial Technology pulled 12.9% of the highest multiples vote, anchored by niche domestic manufacturers serving technology end markets. Pete Phillips of Madison Street Capital cited 10–12x multiples for that profile, reflecting steady buyer appetite for differentiated manufacturers tied to long-term technology demand.

Metals & Mining drew the lowest multiple vote from 30.8% of respondents. Scott Mitchell of SDR Ventures pegged the range at under 5x, attributing the discount to “choppiness of market due to trade policy uncertainty.”

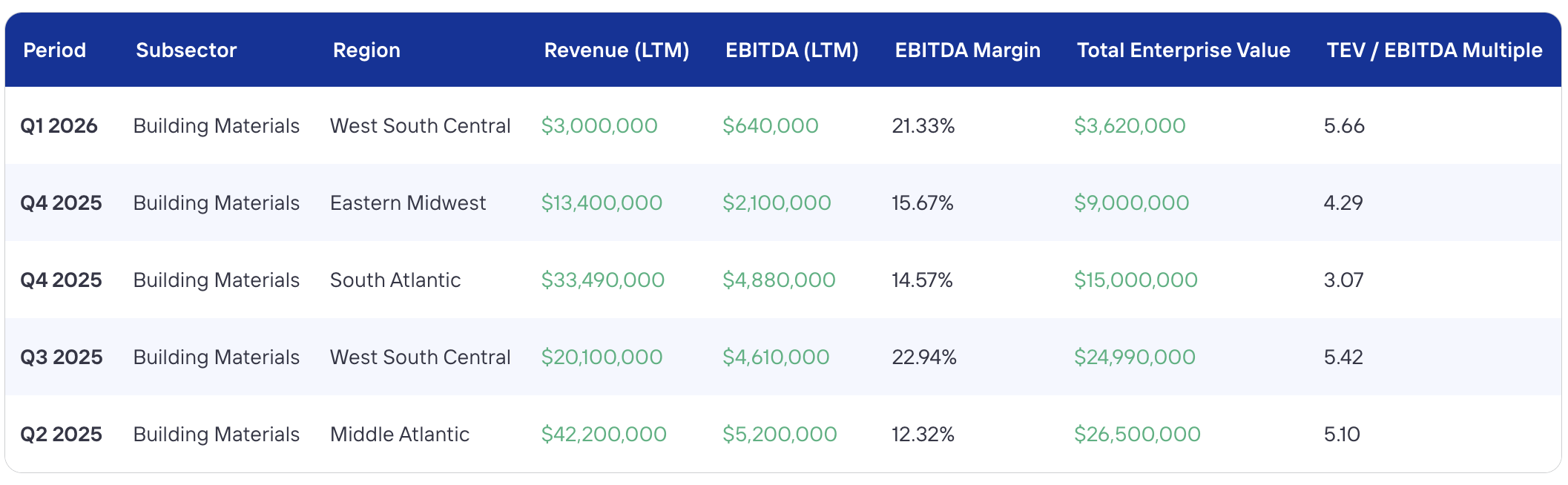

For C&E businesses, surveyed members most frequently pointed to project-based revenue streams and lower forward visibility as the primary factors weighing on valuations. Josh Gladtke of Good Hope Advisors said average multiples in the space are 4–5x, describing the sector as “very project specific, cyclical industries with low visibility compared to service-based industries.” Without a recurring revenue mix, he added, “these design and build businesses trade at lower multiples.” See the table below for construction comparables from executed LOIs on the Axial platform.

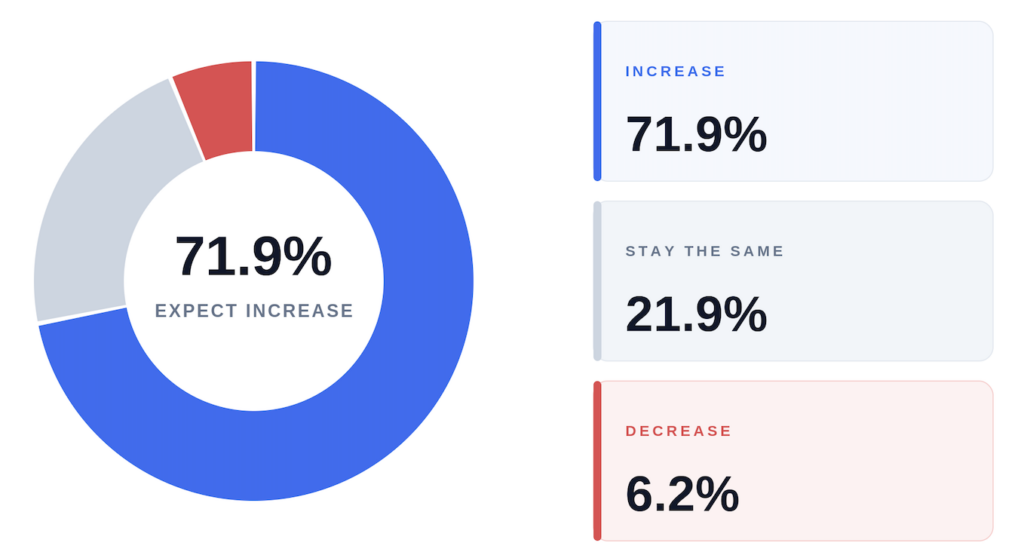

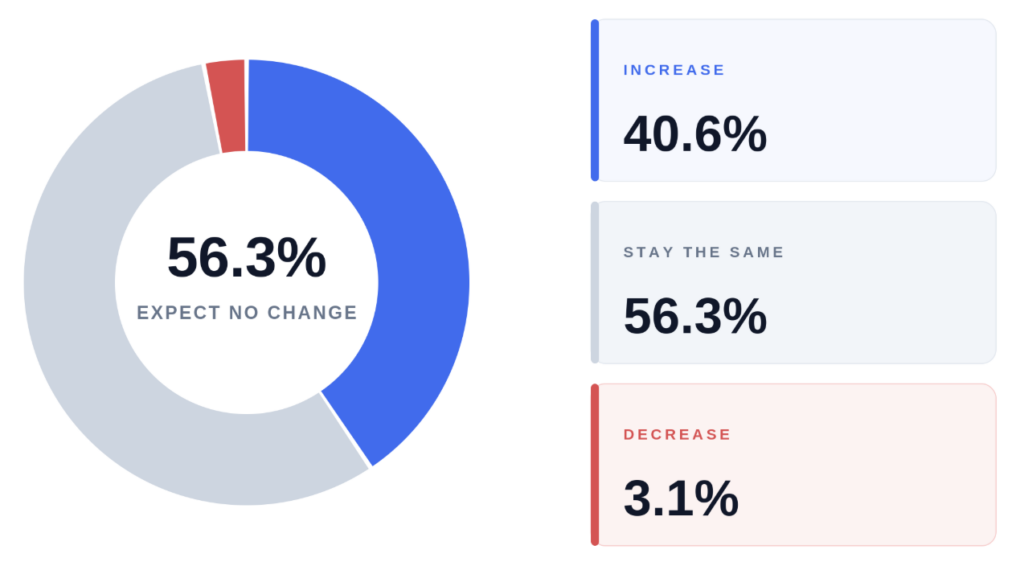

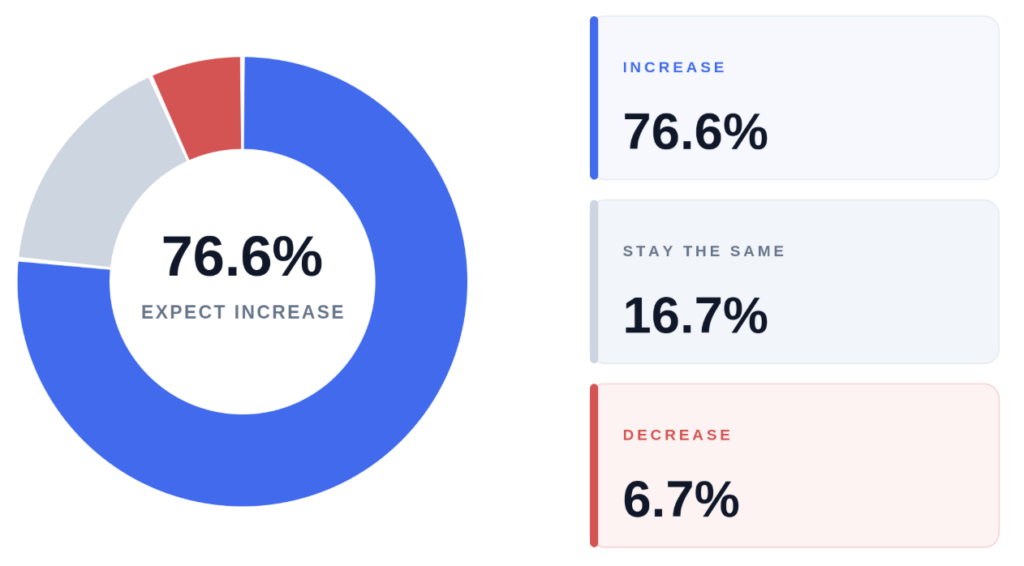

Sentiment among surveyed industrials dealmakers appears cautiously optimistic heading into the next 12 months. More than 70% of respondents expect both overall deal flow and closed deal volume to increase, while only a small minority anticipate a decline in activity. Views on valuations were somewhat more balanced, with most respondents expecting multiples to remain steady and 40.6% forecasting higher valuations. Overall, the results point to ongoing confidence in transaction activity across the sector, even as buyers remain disciplined on pricing and underwriting.

→ Track lower middle market deal activity, valuation trends, and sector performance on Axial’s Deal Flow Intelligence Dashboard.

Survey responses revealed a market focused on a relatively concentrated set of themes across both opportunities and challenges. On the opportunity side, dealmakers most frequently highlighted power infrastructure, electrification, AI-related data center demand, and recurring-revenue industrial services businesses. At the same time, respondents pointed to labor availability, rising input and energy costs, and increased buyer scrutiny around earnings quality and revenue visibility as some of the most persistent challenges shaping the industrials landscape today.

| Member + Firm | Quote |

|---|---|

| Josh Campbell, NorthEnd Associates | Anything connected to power grid, utilities, and defense industry expansion is attracting major interest in the market, as key economic drivers in those industries continue to expand. |

| Scott Mitchell, SDR Ventures | The data center halo effect: any company that is directly or indirectly serving the data center build-out, including electrification, cooling, building products, etc. |

| Anonymous Private Equity Fund | Opportunities tied to data center buildout, power services, automation, environmental services, and engineering. |

| Joe Bieshelt, The Venture North Group | With the emergence of AI data centers, EV production, and the reshoring of U.S. manufacturing, creating electric demand to surge, I believe operations in the electrical infrastructure arena will be in high demand for years to come. |

| David Hartland, Del Monte Capital | The biggest opportunities are in water and wastewater-related areas, but power-related opportunities remain attractive as well. |

| Rex Reinhardt, Great Plains Capital Partners | I think any companies that feed into AI or data centers are going to be attractive. |

| Member + Firm | Quote |

|---|---|

| Pete Phillips, Madison Street Capital | Niche manufacturing and industrial services. |

| Josh Gladtke, Good Hope Advisors | The biggest opportunities in industrials right now are in service-driven HVAC, plumbing, and electrical businesses tied to recurring maintenance and replacement work, where demand is driven more by aging infrastructure than new construction. |

| Gurkaran Tiwana, Heritage Holding | Service and preventative maintenance shops. |

| Anonymous Investment Bank | Value-added services, niche manufacturing, facility retrofits, and maintenance. |

| Member + Firm | Quote |

|---|---|

| Leonardo Ferreira, Hill View Partners | The biggest opportunities lie in aerospace and defense manufacturing, which is shifting toward a ‘war footing’ to meet a massive global backlog for munitions, drones, and missile systems. |

| Brian Santana, Schmidt Industrial Services | Automation, leaning into industrial policy, pivoting to government needs. |

| Rex Reinhardt, Great Plains Capital Partners | I think Aerospace & Defense will trade up here for the foreseeable future. |

| Member + Firm | Quote |

|---|---|

| Michael Schuster, Cross Keys Capital | The demand for technical labor. |

| John Murray III, Sligo Strategies | Really seems like whoever I speak to, the blue-collar workforce or lack thereof is a major limiting factor to growth and profits. |

| Josh Gladtke, Good Hope Advisors | The biggest challenges in industrials today are labor shortages and rising input costs, which continue to pressure margins and limit growth for otherwise strong operators. |

| Member + Firm | Quote |

|---|---|

| Ben Luchow, SDR Ventures | Petroleum prices and the downstream impact on companies that produce, sell, or buy petroleum-based products. |

| Emery Ellinger, Aberdeen Advisors | Rising energy prices. |

| Rex Reinhardt, Great Plains Capital Partners | Niche manufacturers are still struggling with sourcing offshore raw materials. If they don’t rely on such, they’re a step ahead of their peers who do, as they don’t have to pass on price increases to their customers. |

| Josh Campbell, NorthEnd Associates | Interest rates, fuel costs, and general price inflation are creating supply chain bottlenecks downstream of power, data center, and defense demand. |

| Member + Firm | Quote |

|---|---|

| Rob Chepak, TREP Advisors | Customer concentration and project lumpiness are a drain on valuation. The buyer market has gotten more disciplined about this. Any business owner with significant top-three customer concentration or a few large projects sees more earnouts, escrows, and seller notes in their structures than clean cash exits. |

| Arthur Petropoulos, Hill View Partners | Growing need to clearly illustrate repeatable, durable processes for sales and execution to assuage concerns driven by macroeconomic or broader risks (or perceived risks). |

| David Hartland, Del Monte Capital | Demonstrating credible, stable, normalized earnings over a multi-year period. |

The 2026 outlook is defined by concentration and discipline. Survey responses reflected continued activity in HVAC, power infrastructure, and data-center-adjacent businesses, alongside premium valuations for recurring-revenue industrial services and aerospace & defense companies. At the same time, respondents consistently emphasized buyer focus on revenue quality, labor stability, and operational visibility. The industrial businesses best positioned in the year ahead appear to be those that can demonstrate recurring revenue, a stable, skilled workforce, and clean financial reporting.

Our Top 50 industrials list was generated based on a weighted formula leveraging four key metrics:

Survey insights are drawn from Axial’s 2026 Industrials M&A Outlook survey, conducted in May 2026. The respondent pool consisted of M&A advisors, investment bankers, and investors, all of whom are members of this year’s ranked list.