Recognizing 20 Military Veterans in M&A

As America celebrates its 250th anniversary, we wanted to take the opportunity to highlight 20 military veterans who have successfully…

On March 2, 1901, Andrew Carnegie agreed to sell Carnegie Steel to J.P. Morgan in a transaction valued at $480 million. Morgan combined Carnegie Steel with several other companies to form U.S. Steel, the world’s first billion-dollar corporation.

The sale effectively ended Carnegie’s career in business. After building one of the nation’s largest steel companies, he devoted much of the rest of his life to philanthropy.

The creation of U.S. Steel was more than one of the largest business transactions in American history. It reflected broader changes in how large businesses were financed, owned, and organized as the United States entered the twentieth century.

Over the past 250 years, the sources of capital available to American businesses have changed dramatically. Individual entrepreneurs gave way to Wall Street financiers, public corporations, private equity firms, and, more recently, a growing mix of long-term investors active in the lower middle market.

This article traces that evolution. It examines how the people and institutions providing capital changed over time, and how each era reshaped the way American businesses were built, financed, and acquired.

Following the Civil War, the United States entered a period of rapid industrial expansion. Railroads connected the country, steel mills supplied growing cities, oil fueled industry, and manufacturing transformed the nation’s economy. Much of the growth of America’s leading industrial businesses was financed by the entrepreneurs building them, often through retained earnings and personal fortunes rather than dedicated investment funds.

Industrialists like Cornelius Vanderbilt, Andrew Carnegie, and John D. Rockefeller reinvested profits to expand their businesses through new facilities, acquisitions, and infrastructure. Vanderbilt consolidated railroads into the New York Central system. Rockefeller built Standard Oil through a series of acquisitions and vertical integration. Carnegie reinvested in steel production, helping build the nation’s largest steel company.

The model was straightforward. The founder controlled the business, supplied much of the capital, and made the long-term decisions. Ownership, management, and capital remained concentrated in the same hands.

As American industry expanded, so did its capital requirements. Railroads stretched across the continent, factories grew, and combinations of businesses became increasingly common. Financing the next generation of American enterprise required more capital than even the wealthiest industrialists could provide alone.

The era of the self-financed founder gave way to a new class of professional financiers.

As American businesses grew larger, so did their financing needs. Expanding railroads, industrial combinations, and national corporations required more capital than even the wealthiest founders could provide. Investment banks played an increasingly important role in raising capital from many investors and financing businesses at an unprecedented scale.

Few individuals had a greater influence on American finance during this period than J.P. Morgan. Through his banking syndicate, Morgan financed railroads, reorganized struggling companies, and assembled some of the nation’s largest industrial combinations. The creation of U.S. Steel in 1901, Northern Securities in 1901, and General Electric in 1892 illustrated how investment banks could organize capital for increasingly large industrial enterprises.

Wall Street’s role expanded beyond lending money. Investment banks underwrote securities, brought together investors, and helped finance the growth of America’s largest corporations. Capital became increasingly organized, institutionalized, and professionally managed.

By the early twentieth century, many of America’s largest corporations had become permanent institutions, with access to increasingly sophisticated public capital markets. As public securities ownership broadened and capital markets matured, corporations gained new ways to finance growth beyond traditional investment banking syndicates.

The next evolution in American capital would come from the corporations themselves.

By the middle of the twentieth century, acquisitions had become a central growth strategy for many of America’s largest public companies. Public companies increasingly used their balance sheets and publicly traded stock to acquire businesses and diversify into new industries.

Companies such as ITT, Ling-Temco-Vought (LTV), and Gulf + Western pursued aggressive acquisition programs across dozens of industries. Under leaders including Harold Geneen, James Ling, and Charles Bluhdorn, diversification became one of the defining corporate strategies of the era. Businesses with little operational connection were assembled into conglomerates under the belief that skilled management could improve performance across diverse industries.

Publicly traded stock became an increasingly important acquisition currency. Rather than financing growth with personal fortunes or investment banking syndicates, corporations increasingly used their own stock to acquire businesses and expand into new markets.

By the 1970s, investors began questioning whether larger always meant better. Many conglomerates began trading at a discount to the combined value of their underlying businesses, and shareholders increasingly favored companies with clearer strategic focus.

The stage was set for a new generation of buyers that increasingly viewed acquisitions as financial investments rather than corporate expansion.

The next evolution in American capital was driven not by public corporations, but by financial buyers. Rather than relying primarily on corporate balance sheets or publicly traded stock, buyout firms combined equity capital with significant debt financing to acquire businesses. Leverage became a defining feature of modern acquisitions.

The founding of Kohlberg Kravis Roberts & Co. (KKR) in 1976 helped establish the leveraged buyout as a distinct investment strategy. Michael Milken’s high-yield bond market expanded access to acquisition financing, while investors, including T. Boone Pickens, demonstrated the growing influence of activist shareholders and takeover activity. Transactions such as the 1986 Safeway buyout and the 1989 RJR Nabisco acquisition brought leveraged buyouts into the national spotlight.

Unlike the conglomerates that preceded them, financial buyers acquired companies with the goal of improving operations, reducing debt, and ultimately generating investment returns. Private equity emerged as a recognizable force in American business.

The collapse of Drexel Burnham Lambert in 1990 marked the end of the junk bond era, but not the end of leveraged buyouts. As pension funds, endowments, and other institutional investors increased their allocations to private equity, the industry became larger, more disciplined, and mainstream.

The next chapter in American capital would be defined not by leverage alone, but by the rise of private equity as an institutional asset class.

By the 1990s, private equity had evolved from a niche investment strategy into an established asset class. Pension funds, university endowments, and insurance companies increasingly allocated capital to private equity, providing firms with larger and more stable pools of long-term capital.

As institutional commitments grew, so did the industry. Firms including Blackstone, KKR, Apollo, and Carlyle raised larger funds, expanded globally, and developed specialized investment strategies across industries and transaction types. Their public listings between 2007 and 2012 reflected the industry’s growing scale and maturity.

Private equity firms also became more specialized. Many developed dedicated sector expertise, repeatable investment processes, and global fundraising platforms, transforming private equity into a mature segment of the capital markets.

As private equity expanded, institutional capital flowed beyond the industry’s largest firms. Smaller funds, co-investment strategies, and emerging managers attracted growing interest from institutional investors, broadening the range of buyers competing for privately held businesses.

The next chapter in American capital would be shaped not only by larger institutions, but also by a growing number of family offices, independent sponsors, search funds, and individual investors competing for privately held businesses.

Over the past decade, the buyer landscape has expanded well beyond traditional private equity firms. Today, a broader range of investors pursues acquisitions in the lower middle market through a variety of ownership models, investment horizons, and financing structures.

Several investment models have gained momentum during this period. Family offices have increasingly invested directly in private companies, while independent sponsors have expanded through deal-by-deal fundraising, often partnering with family offices and other long-term investors to complete acquisitions. The growth of independent sponsors is also reflected on Axial, where the number of new firms joining the platform has grown 3.34x since 2021

Read Axial’s 2025 Independent Sponsor Report for a deeper look at one of the fastest-growing buyer types.

Search funds have become an established pathway for entrepreneurs to acquire and operate businesses. Since 2021, the number of searchers on Axial has grown 6.94x, while new individual investors have increased 3.75x over the same period. SBA-backed 7(a) loans have become an increasingly important financing tool for many of these buyers, and recent program changes have expanded the amount of SBA-backed capital available for qualifying acquisitions.

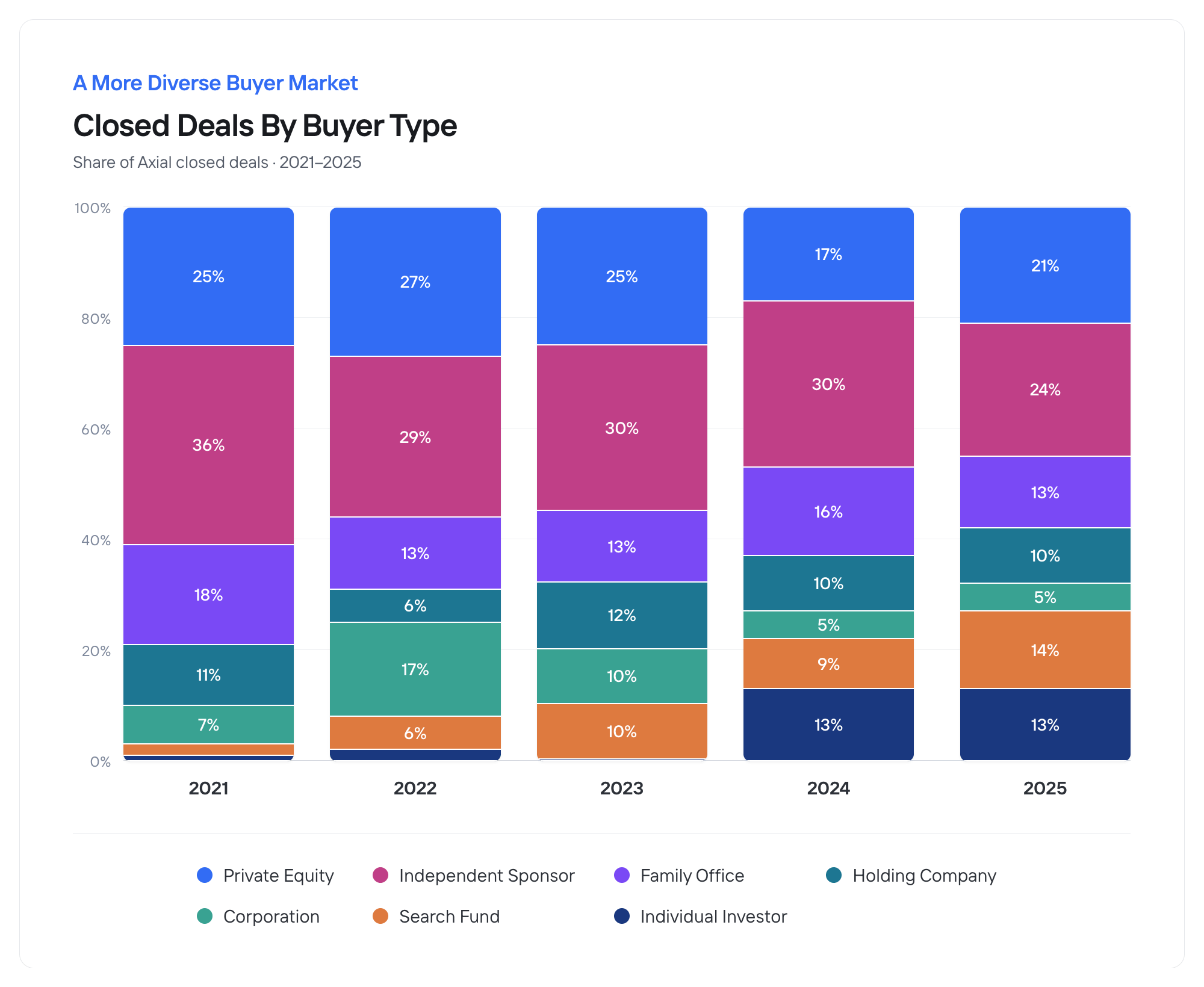

In 2021, private equity and independent sponsors together accounted for 61% of all closed deals on Axial. By 2025, that combined share declined to 45%.

The chart also illustrates a broader mix of buyers completing transactions on the platform. Individual investors have increased their share to 13% in both 2024 and 2025, while search funds accounted for 14% of closed deals in 2025, an all-time high. Family offices and holding companies remained relatively consistent, representing an average of 15% and 10% of transactions over the last five years, respectively. The overall result is a more balanced buyer landscape across the lower middle market than in prior years.

When Andrew Carnegie sold Carnegie Steel in 1901, the financing of American business was already beginning to change. Over the next century, the sources of capital continued to evolve alongside the businesses they financed, reshaping how companies were built, acquired, and owned.

Across every era, American business has changed alongside the people and institutions that financed it. The industries have changed. The financing structures have changed. The investors have changed. But the underlying objective has remained the same: identifying strong businesses, providing the capital to help them grow, and creating long-term value through ownership.

As part of Axial’s USA 250 series, we’re publishing a collection of articles that trace the history of American M&A, business ownership, and capital to commemorate the nation’s 250th anniversary. Read more from the series below.