Alex de Pfyffer and Ross Porter’s Journey from Self-Funded Search to a $220M Committed Fund

Today’s guests are Alex de Pfyffer and Ross Porter, Co-Founders of Heritage Holding, an investment firm that has completed nearly…

Tags

Axial is happy to release its 2026 publication of the Top 50 Lower Middle Market Technology Investors and M&A Advisors, a list featuring Axial’s 50 most active and sought-after members who specialize in transactions across various tech sectors over the past 12 months (methodology below). In addition to celebrating these Top 50 members, this feature includes reflections and insight from our recent 2026 Technology M&A Outlook survey.

Our Top 50 technology list was generated based on a weighted formula leveraging four key metrics:

Congratulations to these members for their achievements!

We asked deal professionals whose firms are featured on this list to share insights on the general industry landscape, business owner mentality, valuation expectations, and the biggest challenges and opportunities shaping the market today, and activity across key sub-sectors, including:

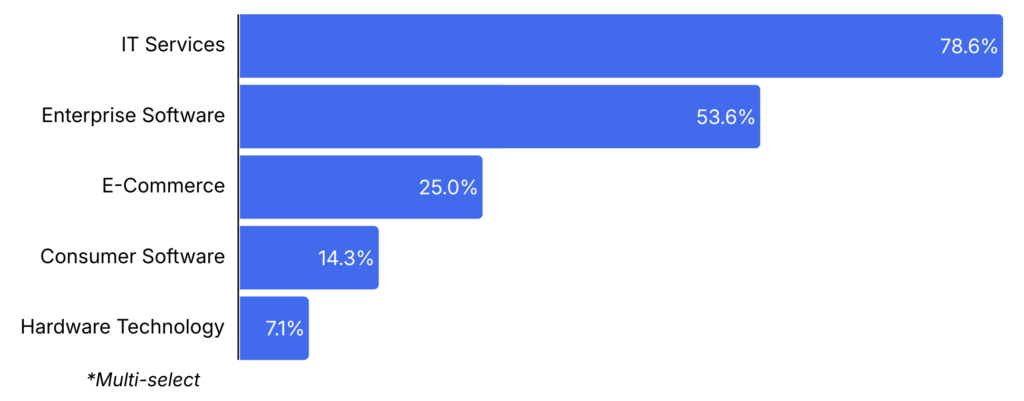

IT Services (78.6%) and Enterprise Software (53.6%) were highlighted as the sub-sectors seeing the most deal activity, well ahead of E-Commerce, Consumer Software, and Hardware Technology.

In IT Services, MSPs and cloud service providers continue to lead. Ryan Barnett of Revenue Rocket Consulting Group explains, “MSPs and cloud service providers remain the backbone of lower middle market tech M&A. Recurring revenue, sticky customers, and essential services make these businesses perennial acquisition targets for both strategics and PE roll-ups.”

Within Enterprise Software, activity continues to center on vertical SaaS and mission-critical applications. As Ali Evans of Metamora Growth Partners notes, “Vertical market software remains the most active sector; however, recent public market volatility and fears over GenAI decreasing demand have put a damper on transactions.”

–

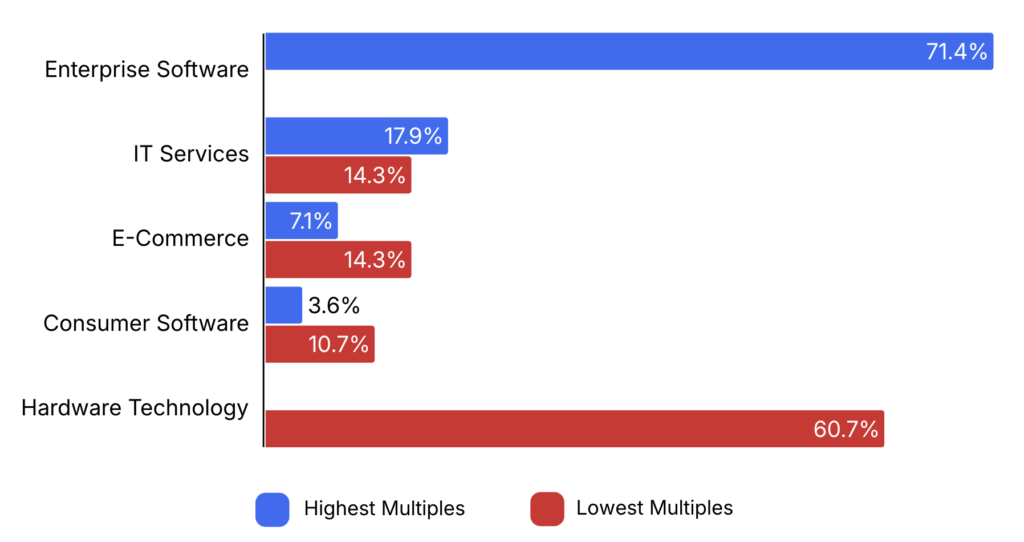

The survey results show a decisive spread, with Enterprise Software identified by 71.4% of respondents as commanding the highest multiples, and Hardware Technology was cited by 60.7% as having the lowest. The premium placed on Enterprise Software likely reflects its recurring revenue models, high gross margins, scalability, and mission-critical integration into customer workflows.

In contrast, Hardware Technology businesses tend to face capital intensity, supply chain risk, lower margin profiles, and more cyclical demand. The gap illustrated in the data reinforces a broader market preference for asset-light, subscription-based models over capital-heavy, operationally complex businesses.

| Member + Firm | Quote |

|---|---|

| Jonathan Haski, Adarna Health Group | There is a massive opportunity to acquire fragmented, labor-intensive services (like RCM) and immediately apply AI to expand profit margins. |

| Aaron Solganick, Solganick & Co. | Artificial intelligence, cybersecurity, cloud services and infrastructure, and data analytics seem to have the highest demand and largest growth opportunities today. The demand also drives up M&A transactions in these sectors. |

| Anonymous M&A Advisory Firm | Using directives from their partnership organizations, like Microsoft, to build in-house talent and offer the best possible solutions around new technology. |

| Charles Botchway, Madison Street Capital | Integration of AI into day-to-day company operations improves efficiency, helps create new services and products, and ultimately improves profitability. |

| Dudley Arbaugh, The Brydon Group | Apply rapid innovation to build/buy in previously underserved industries. |

| Rajib Kabir, Sunfield Advisors | There is a strong opportunity to acquire profitable, founder-led vertical SaaS and tech-enabled staffing platforms, where recurring revenue and operational discipline can drive multiple expansion. |

| Anonymous Investment Bank | Leveraging AI to improve efficiencies, cut costs, and bring new products/services to market |

| Ryan Barnett, Revenue Rocket Consulting Group | Everyone is watching the AI producers capture headlines and tech fund dollars, but it's the IT services firms that can actually put AI to work inside real businesses that are positioned for explosive growth. |

| Edward Solomon, Net at Work | Digital transformation of legacy solutions to new technologies. |

| Ali Evans, Metamora Growth Partners | Focusing on solving client needs first and hiring great talent at lower prices as they leave Big Tech. |

Across responses, a clear theme emerges: AI-driven transformation is the dominant opportunity in technology today. Respondents pointed to applying AI to improve efficiency, expand margins, and create new products and services, particularly within fragmented, labor-intensive industries.

Beyond AI, members highlighted strong demand in cybersecurity, cloud infrastructure, data analytics, and digital transformation of legacy systems. Founder-led vertical SaaS and tech-enabled services businesses were also cited as attractive opportunities, especially where recurring revenue and operational discipline can drive growth and multiple expansion. Overall, the emphasis is less on AI hype and more on practical application within real businesses.

–

| Member + Firm | Quote |

|---|---|

| Rajib Kabir, Sunfield Advisors | Valuation gaps between buyers and sellers continue to stall transactions as expectations reset to post-2021 realities. Profitability and cash flow now outweigh pure growth, putting pressure on high-burn models. AI is both driving deal activity and disrupting legacy business models, creating underwriting uncertainty. |

| Ali Evans Metamora Growth Partners | Integrating AI to meet real client demand, not just for the sake of having it. |

| Ryan Barnett, Revenue Rocket Consulting Group | AI is reshaping every corner of the technology industry, and the companies that haven't figured out whether AI is their friend or their existential threat are in the most precarious position. |

| Josh Robbins, Premara Group | Uncertainty around AI and what it will do to the industry. |

| Anonymous Investment Bank | The technology industry is navigating a complex, transitional phase defined by high-stakes AI adoption, mounting regulatory pressures, and a "cautious" hiring landscape. |

| Philip Kaczmarczyk, AYCE Capital | Cybersecurity is rapidly developing, and most SMEs are unprepared for this reality. |

| Jonathan Haski, Adarna Health Group | LMM technology companies are demanding historically high valuations, riding the tailwinds of generative AI. This is driving a movement of capital away from expensive software and toward tech-enabled services, like revenue cycle management, where investors can apply AI to optimize cash-flowing operations. |

| Dudley Arbaugh, The Brydon Group | Shifting defensibility landscape. |

| Zach Luke, Northbound Group | We are currently seeing a shift in traditional SaaS products: seat pricing is disrupted by AI deployment, and new product solutions are more easily replicated. |

| Cristian Anastasiu, Excendio Advisors | Uncertainty regarding the economy and AI adoption. |

While respondents identified AI-driven transformation as the industry’s greatest opportunity, they also view it as its most significant source of uncertainty. Many describe the current environment as one of adjustment, with valuation expectations resetting as buyers prioritize profitability and cash flow over growth, contributing to deal friction. At the same time, AI’s rapid evolution raises questions about defensibility, pricing models, and long-term competitive positioning. Layered with regulatory and macroeconomic uncertainty, respondents point to an industry in a recalibration phase where differentiation and disciplined execution matter more than ever.

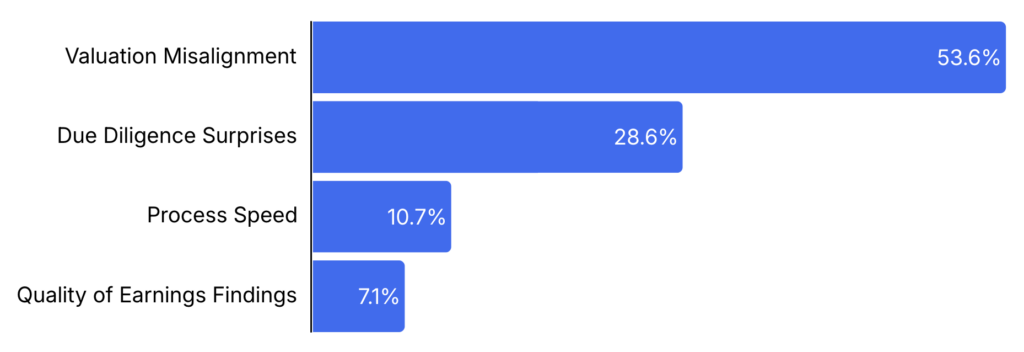

Survey responses indicate that valuation misalignment is the primary hurdle in closing technology deals, cited by 53.6% of respondents, followed by due diligence surprises (28.6%). With that context in mind, we asked survey respondents whether they expect valuations to increase or decrease over the next 12 months and which factors are most likely to influence valuations.

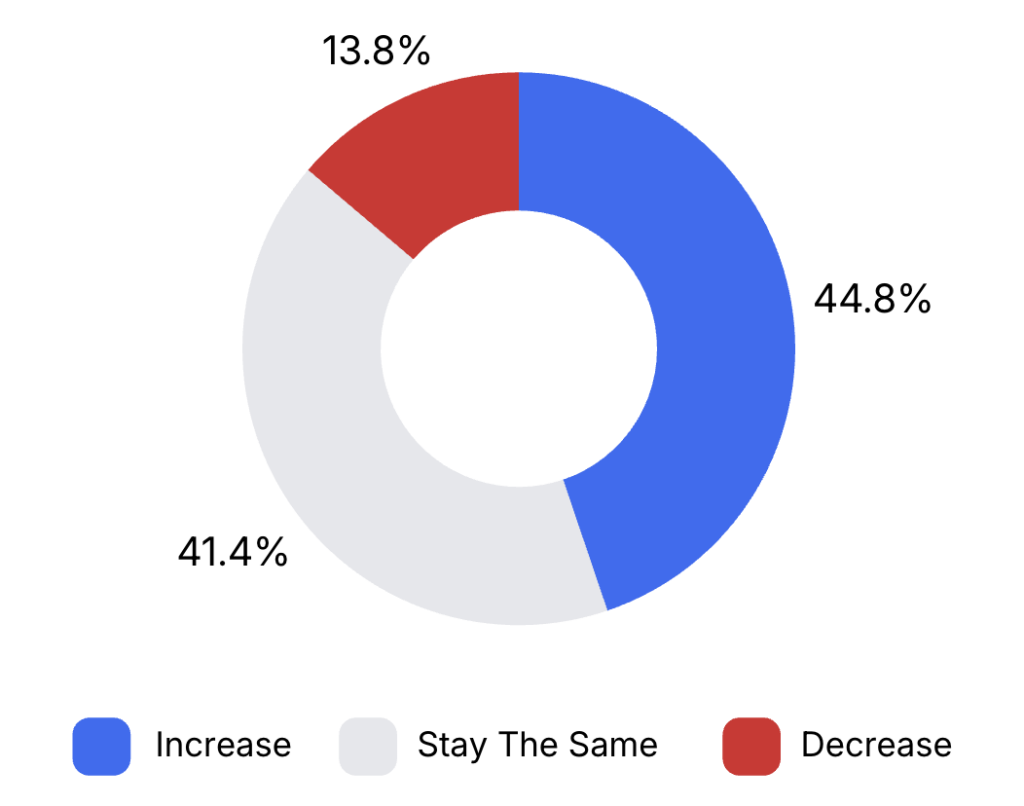

Respondents were fairly evenly split on whether technology valuations will increase or remain the same over the next 12 months. 44.8% expect valuations to increase, while 41.4% believe they will remain flat, and only 13.8% anticipate a decrease. The results suggest cautious optimism, with most participants either forecasting stability or modest growth. To better understand what may drive pricing from here, respondents were also asked which factors they believe will have the greatest impact on technology valuations in the year ahead.

| Member + Firm | Valuation Expectations | Quote |

|---|---|---|

| Philip Kaczmarczyk, AYCE Capital | Increase | Reduced interest rates, tariff impacts reducing investment in other sectors of the economy, and the continuous flow of funds to the private markets. |

| Charles Botchway, Madison Street Capital, LLC | Stay The Same | Revenue growth and margin consistency, profitability, AI adoption and inclusion, and overall capital markets mood based on activity. |

| Zach Luke, Northbound Group | Decrease | Speed of growth while maintaining profitability, as well as the ability to lean into AI enablement. |

| Cristian Anastasiu, Excendio Advisors | Stay The Same | Interest rate trends; the pace of AI adoption and implementation; sustainable revenue growth rates; customer concentration risk; and the relative attractiveness of technology as an investment compared to other sectors (such as healthcare, manufacturing, and construction). |

| Moses Elwon, BlackRose Group | Increase | The demand for AI services during the next few months. |

| Josh Robbins, Premara Group | Stay The Same | Stock prices of large tech companies and more certainty around how AI will impact white-collar jobs. |

| Anonymous M&A Advisory Firm | Increase | Supply of quality assets in the market. The AI bubble also brings questions of when the hype needs to translate into economics. |

| Ryan Barnett, Revenue Rocket Consulting Group | Stay The Same | In IT services, valuation comes down to a handful of fundamentals: absolute EBITDA size, recurring revenue, contract depth, customer concentration, service line mix, and growth trajectory. Get those right, and you're in a different conversation. |

Respondents point to a mix of macro conditions and company-level fundamentals as the primary drivers of technology valuations in the year ahead. Interest rates, capital markets sentiment, and the flow of capital into private markets are viewed as foundational influences, while growth durability, recurring revenue, and customer concentration remain critical at the company level. The pace and practical impact of AI adoption also loom large, with participants questioning how quickly demand translates into sustainable economics. With these factors in mind, we also asked whether they anticipate broader industry shifts driven by macroeconomic forces over the next 12 months.

| Member + Firm | Quote |

|---|---|

| Rajib Kabir, Sunfield Advisors | Yes. Over the next 12 months, higher interest rates and tighter credit conditions will continue to favor profitable, cash-flow-positive tech companies over high-burn growth models. |

| Charles Scripps, Black Lake Capital | We hope to see a settling of conflicts in Ukraine and the Middle East, making international talent more accessible. |

| Cristian Anastasiu, Excendio Advisors | We are likely to continue experiencing a high degree of uncertainty. Some companies will adapt more effectively to this environment of frequent change. In certain cases, taking calculated risks may lead to meaningful gains. |

| Aaron Solganick, Solganick & Co. | Artificial intelligence is a current and future "threat" to software and hardware applications. In addition, ongoing unstable political environments in the US and globally are a major risk over the next 12+ months. |

| Charles Botchway, Madison Street Capital | The China vs US tech competition could mean geopolitical factors play a role. If the sentiment that AI could dislodge saas starts to look like reality, that would have a significant impact on the industry as a whole. |

| Anonymous Investment Bank | Quality transactions will be the focus from investors as we continue to monitor changes in inflation and interest rates. |

Select responses suggest macroeconomic forces will continue to favor profitable, cash-flow-positive businesses, particularly in what is still considered a higher-rate, tighter-credit environment. Inflation, interest rates, and capital availability remain key variables, while geopolitical tensions and AI-driven disruption add another layer of uncertainty.

| Member + Firm | Quote |

|---|---|

| Aaron Solganick, Solganick & Co. | Solganick noted its busiest deal flow uptick yet in January and February 2026. We are seeing many companies come out to the M&A market that were on hold over the past year or two. Most of this seems show that companies have stabilized their financials and are on a growth path again. |

| Cristian Anastasiu, Excendio Advisors | I expect continued strong M&A activity involving well-positioned technology companies, as capital remains available and opportunities for market consolidation persist. Preparation will be critical. Companies that combine operational discipline with forward-looking innovation are likely to be in the highest demand. |

| Ryan Barnett, Revenue Rocket Consulting Group | The lower-middle-market IT services space is at a genuine inflection point. AI is reshaping business models overnight, a generation of founders is approaching their exit window, and buyer appetite for quality assets has never been stronger. But quality is paramount. The firms that will transact at premium valuations are those that have built something that doesn't depend entirely on them to run. |

| Rajib Kabir, Sunfield Advisors | As an operator-led M&A advisor, Sunfield remains focused on disciplined underwriting and partnering with profitable, founder-led technology businesses. We see significant opportunity in AI-enabled services and vertical platforms where operational improvement and strategic consolidation can unlock long-term value. |

Taken together, this year’s survey reflects a lower middle market technology landscape defined by opportunity, selectivity, and discipline. AI continues to reshape business models and investor focus, but the common denominator across responses is clear: quality matters. As 2026 unfolds, momentum appears to be returning, but success will favor those who approach the market prepared, realistic, and strategically positioned.