The Middle Market Review Insights on the Middle Market.

Thanks for subscribing!

Will IPOs Ever Return to the Middle Market?

IPOs are in vogue right now. In the last month alone there was the best IPO week since 2006 and PE IPOs reached their highest ever level.

But, not all companies are getting access to the IPO party. These flotations have largely been reserved for much larger firms with significant market caps.

The small- and medium-sized businesses have largely been ignored in the IPO market for years. And chances are — due to regulatory concerns, investor preferences, and the increasing effectiveness of the private capital markets — the smaller IPO will not return.

Here’s why…

Compliance Challenges

In a recent interview, Marc Andreessen explained that regulatory burdens are one of the primary reasons that IPOs became unfeasible for smaller companies.

“The compliance and reporting requirements are extremely burdensome for a small company,” explained Andreessen. “It requires fleets of lawyers and accountants who come in and do years of work.” While these regulations are intended to protect the small company, he believes it has “the opposite effect.”

Andreessen is primarily referring to the Sarbanes-Oxley Act of 2002 (aka Sarbox), whose controversial Section 404 dealt a blow to small company IPOs. The section was so problematic that the SEC learned that 70% of small companies considered going private again after Sarbox’s Section 404 was implemented in 2002.

While compliance may have driven down the small company IPO, it isn’t these regulations that are keeping smaller IPOs dead. After all, the JOBS Act modified Section 404 to be more accommodating for small firms. The results have been underwhelming. As Steven Davidoff and Paul Rose explained in their research paper on The Disappearing Small IPO, “Percentagewise, the number of small IPOs [in 2013] was one of the lowest since 1996. The trend instead is toward ever larger IPOs. The number of large IPOs was the largest since at least 1996.”

Investor Savviness

If not regulation, then what killed the small IPO? Many pundits point to investor savviness as a factor in the demise. Back in the 1990s, the primary investor in a company’s IPO was an individual. Today, hedge funds and mutual funds dominate the stage.

As Andreessen continued in his interview, “The problem is the shareholder base itself has changed dramatically. You’ve had a dramatic rise in hedge funds. Very short-term trading and dramatic rise in short-selling. If you’re a public company, you become the shuttlecock between warring longs and shorts. They bat your stock around like it’s a chew toy.”

Axial Member Tom Courtney, of The Courtney Group, identified a similarly important impact from mutual funds. “Most mutual fund managers do not want to own more than 5% of a company (because they have to report it to the SEC) and want to be able to sell a position in 3-5 days without moving the price of the stock. Add to this the economics of the mutual fund business, that an equity mutual fund typically becomes a profitable business at around $200 million in assets under management (charging 1% a year for expenses) and you can calculate that a stock must have a market capitalization of about $300 million.”

The changing nature of the average public investor made the opportunity for small- and mid-cap companies much less appealing. Since these savvier investors cared less about smaller IPOs, these companies received less coverage from analysts and were traded less frequently. As a result, many of small companies in the public market became unprofitable. The consequence of poor trading can still be felt today — just look at Crumbs’ recent bankruptcy.

Since the mass return of the individual investor to the stock market is unlikely, these developments in investor habits have proven much more problematic — and permanent — for the smaller IPO than the more transient regulatory matters.

The Growing Effectiveness of M&A

Although shifting regulations and investors accelerated the initial decline in small company IPOs, the primary factor that has kept small companies off the public markets is the effectiveness of the private capital markets and M&A.

Over the past twenty years, there has been an explosion of deal professionals around the United States. The growing number of private equity firms, search funds, investment banks, and M&A advisors has dramatically increased a private company’s ability to tap into the private capital markets. The opportunities have only improved as technologies — like Axial, AngelList, etc. — have developed.

Many business owners and entrepreneurs have realized that partnering with financial sponsors or strategic acquirers can offer comparable opportunities as an IPO, without the additional headaches or risks. As a result, even if the investors and regulators changed back, many private companies would still remain private.

As John C. Coffee, Jr. explained, “Issuers conduct IPOs for multiple reasons: (1) to raise capital; (2) to create a public market and give their founders liquidity; and (3) to generate the highest valuation for their firm through the efforts of underwriters.” With a slight exception for #2, partnering with the right financial sponsor or strategic acquirer can be just as effective as going public.

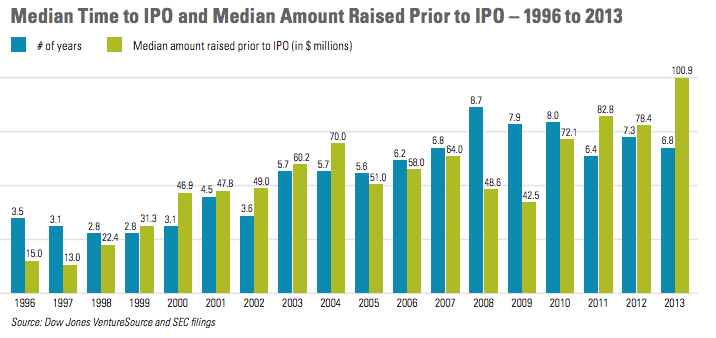

The fact that SMBs are favoring a first stop at the private capital markets can be seen in the amount of capital raised by a company before it goes public.

(Source: WilmerHale)

The companies that went public over the last four years had raised on average more than $70M pre-IPO, leaving many of them simply too large to be acquired. After raising that much money, you generally are seeking a $250-1B+ exit, which is well beyond the means of most strategic and PE acquirers. As such, the only option still available is an IPO.

The appeal of staying private has become even more important in recent years. As baby boomers begin to retire, they are concerned about the legacy of their business, and are seeking strategies that can ensure a dynasty of their choosing. Choosing the buyer/investor of their business can help secure that strategy.

Learn More About Joining Axial

Subscribe to Middle Market Review