Revisiting Private Credit and AI with Matt Plooster

Matt Plooster returns to the podcast to deliver a timely update on private credit and specifically its deployment in the…

Tags

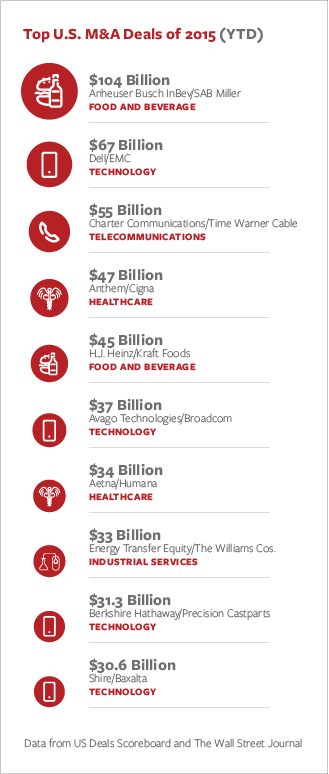

As we settle into the fourth quarter, it’s a good time to recap this year’s record-setting U.S. M&A deals to date. What are the trickle-down effects from these large deals to middle market activity? What are the notable drivers that keep buyers coming?

As we settle into the fourth quarter, it’s a good time to recap this year’s record-setting U.S. M&A deals to date. What are the trickle-down effects from these large deals to middle market activity? What are the notable drivers that keep buyers coming?

According to Dealogic, the first nine months of the year saw 45 global deals exceeding $10 billion each, for a combined total of $1.15 trillion. This amount already makes this year’s M&A volume and activity the highest first nine months on record, up 89 percent from the same period last year, at $610.5 billion across 27 deals.

Not surprisingly, global volume has been dominated by 33 U.S. targeted deals in the “transformative” $10 billion and over bracket totaling $858.7 billion, inching close to 2014’s U.S. deal total of $1.5 trillion according to Thomson Reuters — and there’s still two months left to go.

As forecasted by dealmakers and industry pundits, 2015 will be the highest U.S. M&A volume and activity on record.

Among large U.S. companies, as well as equity markets, healthcare sector deals have been the year’s headliner. Dominating the list of 2015’s largest deals are healthcare and specifically pharma deals — Teva/Mylan, Mylan/Perrigo Abbvie/Pharmacyclics, and Pfizer/Hospira — closely followed by technology and energy deals.

Should the recently-announced Pfizer and Allergan merger take place before the end of 2015, it will be the biggest of the year.

Healthcare deals are the result of massive sector changes, according to head of corporate finance and capital markets at Citizens Bank Bob Rubino. According to Rubino, “big pharma [is] chasing growth as anchor drugs go generic.” There is also an ongoing hunt for fast-moving life sciences and healthcare IT innovation, and hospitals are consolidating in the wake of the Affordable Care Act and declining reimbursements.

But in the middle market, healthcare isn’t the sector dominating the deals — it’s technology.

According to a September Firmex report, the tech sector is leading middle market deals, followed by energy, industrial services, financial services, and then healthcare.

This could be due to the simple fact that companies in the pharma, medical, and biotech sectors are typically well-established, and due to their regulation and workforce requirements, are also significantly larger in size.

Tech companies are not as heavily regulated as healthcare firms, can operate nimbly regardless of market size, have very sophisticated private equity matchmakers, and in some cases are flush with cash.

Aside from the sectors seeing the most activity, notable factors continue to drive buyers into the middle market, and will continue to do so even if large-cap growth slows down.

They are:

An obvious trend is that the baby boomer generation is nearing retirement, and now is the time for business owners to monetize their assets by selling their businesses.

Large companies are buying small firms to stay competitive, relying on them for innovation, accelerated growth, and immediate adoption of intellectual property.

While competition among private equity firms is growing, deal advisors are also seeing a resurgence in more aggressive and strategic buyers. “The mid-market acquirer now is more advanced than five years ago — the deal teams are more sophisticated,” according to West Monroe Partners Director Steve Sapletal, in a Firmex panel report.

The economy is in an upswing, and with the Fed unlikely to raise rates for the remainder of the year, the availability of cheap credit is favorable for borrowing and conducting leveraged transactions.

When the Fed does raise rates, those higher rates will affect the cost of capital and deal valuations, but the increase will be modest and the impact already priced into both equity and long-term debt markets.

On the flip side, a sense of urgency is also pushing acquirers to issue debt and close transactions in advance of any rate increase.

Strategic buyers may seek to reduce management costs and redundant R&D, as well as increase production efficiencies. A recent FBR & Co. report found that recent tech deals, for example, eliminated more than 10 percent of expenses in large acquisitions and as much as 20 percent in smaller acquisitions.

On the buyer side, valuations have been strong as a result of the substantial liquidity both within the debt financing markets as well as the private equity community, and on strategic buyer balance sheets.

Markets and share acquirer share prices have also reacted more positively following deal announcements and post-acquisition in more recent years. Historically, they were met with the acquirer’s share price coming under pressure.

Many large corporates are now focused on either growth or consolidation, and have the cash to expand. Where newer businesses are capturing market share, or have a new product or service that is superior to the offerings in the market today, larger companies and even overseas Asia-Pacific companies wanting a U.S. presence are seizing these buying opportunities.

Target companies are growing organically and as a result can capitalize on their success by bringing in capital to accelerate growth or by joining forces with larger companies to gain access to expansion opportunities.

Armed with company equity and significant voting power, activist investors are holding company boards and managers to a higher level. Companies are beginning to listen. Activists can oftentimes sway popular opinion regarding dealmaking.

Given the robust global M&A market and the many factors driving buyers in the middle market, 2015 will be a banner year, with even more strategic alliances and acquisitions to come in the year ahead.