Trustworthy Searchers, SBA Policy, and Underwriting ETA Investments w/ Grant Hensel

Today’s guest is Grant Hensel, founder of Entrepreneurial Capital, a fund that partners with self-funded searchers acquiring small businesses through…

With the latest edition of Axial’s Pursuits Report, we explored how the overall profile of buyers in Q3 2022 broke with trends dating to the start of 2020. In particular, we found that private equity funds fell from an average of 28.4% of all fresh buyside mandates to pursue lower middle-market assets to just 15.4% last quarter. Indeed, private equity groups pursued deals at a rate of roughly 10% less quarter over quarter in Q3 to the apparent benefit of search funds.

So, what happened?

Search funds, alongside individual investors and holding companies, have all expanded their presence across the LMM this year — and quite considerably. Taken together, these buyers represented a third of all new mandates in Q3. And search funds alone jumped from 85 new pursuits in Q3 2021 to 135 last quarter — good for an increase of 37% year over year.

Investors on the ground have taken note of this uptick in activity as well.

“Over the past few years, I have noticed more search funds contacting me to participate in various sell-side processes that I am running,” Robert Monahan of Triangle Healthcare Advisors, has observed.

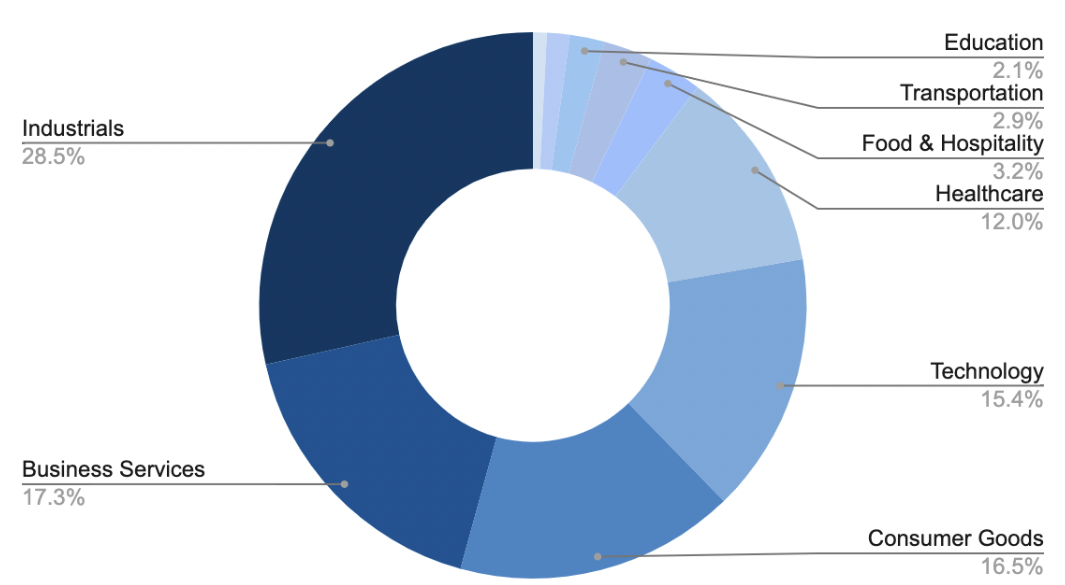

Meanwhile, search funds have formed an appetite for targets in industrials and B2B services that mirrors the wider market’s preference for these sectors in recent years.

Not only can search funds serve as a less expensive entry point for newer LPs than traditional private equity funds, but these firms can also provide more flexibility in their investment strategies. That has meaningfully helped to expand their presence across the LMM, making search funds appealing investment targets in their own right.

Not only do Axial’s data on search funds capture this trend, but these data also fall in line with the most recent findings from the Center for Entrepreneurial Studies at Stanford Graduate School of Business. Search funds are private equity firms that bring just a handful of entrepreneurs — often recent MBAs — together to find and acquire small businesses. Their targets typically comprise lower-middle market companies with annual revenues between $10 million and $250 million.

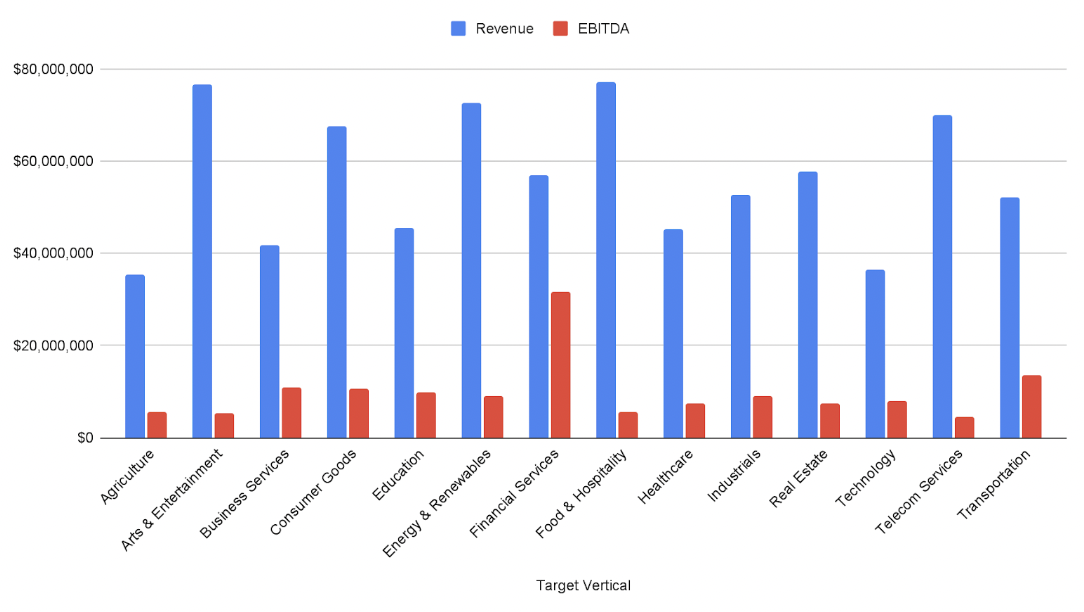

Among the top target sectors in Axial’s data, that average revenue range looks more precisely like $67.7 million for consumer goods to $77.2 million for food & hospitality since the start of 2020.

Another appealing quality of working with search funds is that they represent a form of talent recirculation as individuals or teams of entrepreneurs with experience but limited capital resources can buy and rebuild existing businesses by playing a role in day-to-day operations. Although a frequent first port of call for freshly minted MBAs, search funds would appear just as discerning as their larger peers while managing smaller pools of capital. In Q3, search funds pursued targets generating on average between $4.2 million and $41.9 million in revenues. Meanwhile, private equity targeted between $6.5 million in revenues on average at the low end and $153.4 million at the top.

And the diligence of search funds has caught the attention of investors on the ground.

“I personally enjoy working with search fund buyers,” John Chaffee, a senior broker with Transworld Business Advisors, has said. Transworld has closed three deals via Axial this year, one of which was with a Search Fund. “They are typically a bit more motivated to find and complete a good transaction. For example, I secured a 5x deal at the end of Q2 with an individual leading a search fund. He wanted to find a good fit for his particular background within a given industrial sector and was persistent even when things were tough. He (and his investors) remained very fair-minded in pushing through due diligence to closing.”

Before “search fund” became a term of art, the concept originated at Harvard Business School in 1984 and was then popularized at Stanford over the next decade. By most accounts, there are now 100+ active search funds worldwide, with over $5 billion in capital under management. It’s a small but active set of acquirers. For example, Stanford’s most recent study captures the financial returns and key characteristics of 526 “traditional” search funds formed in North America since 1984. But they operate in much the same manner as their far larger, and far more numerous counterparts in private equity.

Like PE firms, search funds typically raise capital from limited partners. And like PE firms, these LPs include family offices, endowments, foundations, and pension funds that share the same vision and ambition as the search fund’s founders.

In addition to greater access to management, investors in search funds enjoy a number of other benefits. For example, search funds provide a way to get exposure to small businesses that are often hard to access out of larger funds since many fund managers must cut larger check sizes. And for entrepreneurs, it provides them with the capital and resources they need to grow their businesses — not just returns.

“Search funds tend to be more flexible than PE firms in terms of their deal criteria,” Brugner has observed. “They will do smaller deals with nuances to the business model that may deter PE buyers. The personal involvement of the principal and the relationship they develop with the sellers can help overcome issues over the course of a deal. I also think they try harder to stick to timelines than the PE firms do. Overall, the search fund process is a little more transparent from a buyer perspective and a little more friendly.”

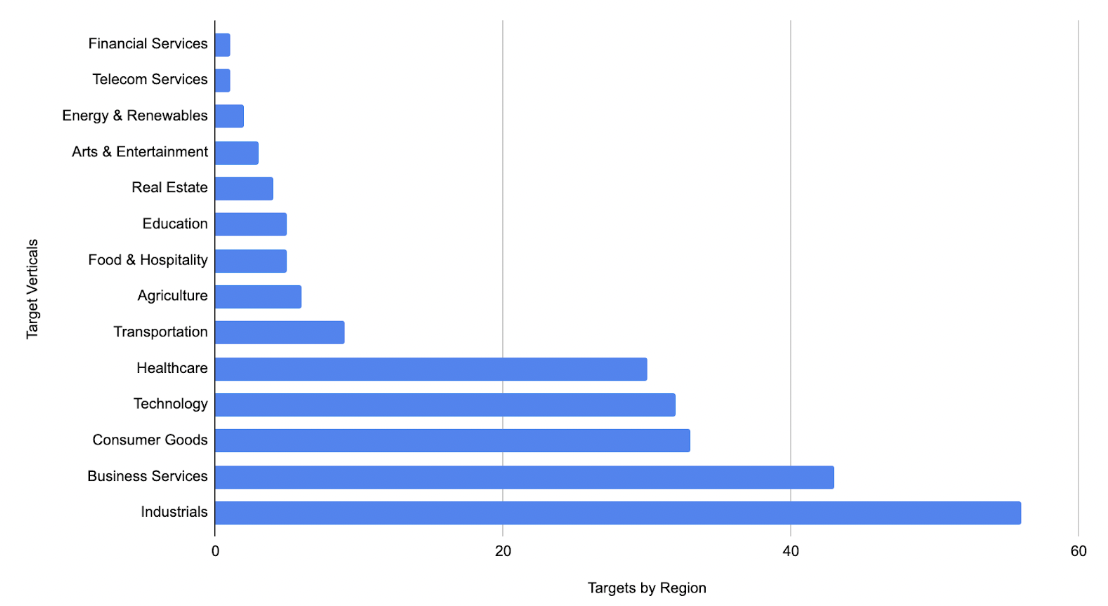

The geographic spread of small businesses sought by search funds ranges considerably by sector.

And search funds generally come in three basic flavors: private equity-backed, venture capital-backed, and corporate-backed.

The search fund model has a number of advantages for its investors. First, it gives them a way to access small businesses that are often hard to reach. Second, it gives them a chance to invest in companies at an earlier stage, before they have been through the rounds of funding from other investors. Finally, it provides a level of confidence to investors that the new operator understands the business and industry deeply.

Private Equity firms have also been using search funds to help source larger M&A deals. In many cases, private equity firms will work with a search fund to support what are, effectively, corporate development initiatives by identifying potential acquisition targets. The search fund will then conduct due diligence on the target company and provide information to the private equity firm.

Although the use of search funds in this way is a relatively new development, it is becoming increasingly popular. Back in the first half of 2018, private equity firms invested $13.6 billion in search fund-backed companies, according to PitchBook data. That was more than double the amount invested in the same period last year and has grown in the years since then. With a significant pool of capital at its disposal, search funds have the resources required to sustain their recent run of success.