Trustworthy Searchers, SBA Policy, and Underwriting ETA Investments w/ Grant Hensel

Today’s guest is Grant Hensel, founder of Entrepreneurial Capital, a fund that partners with self-funded searchers acquiring small businesses through…

This is a guest post from FOCUS Investment Banking, an Axial member since 2010 and an Axial sell-side partner since March of 2021. The FOCUS team has represented 243 total deals on the Axial platform, with 18 in market at the time of this publication. The firm was recognized on three 2022 Axial Top 50 lists — Software, Industrials, and Consumer — and has also been featured on Axial League Tables eight times since 2020.

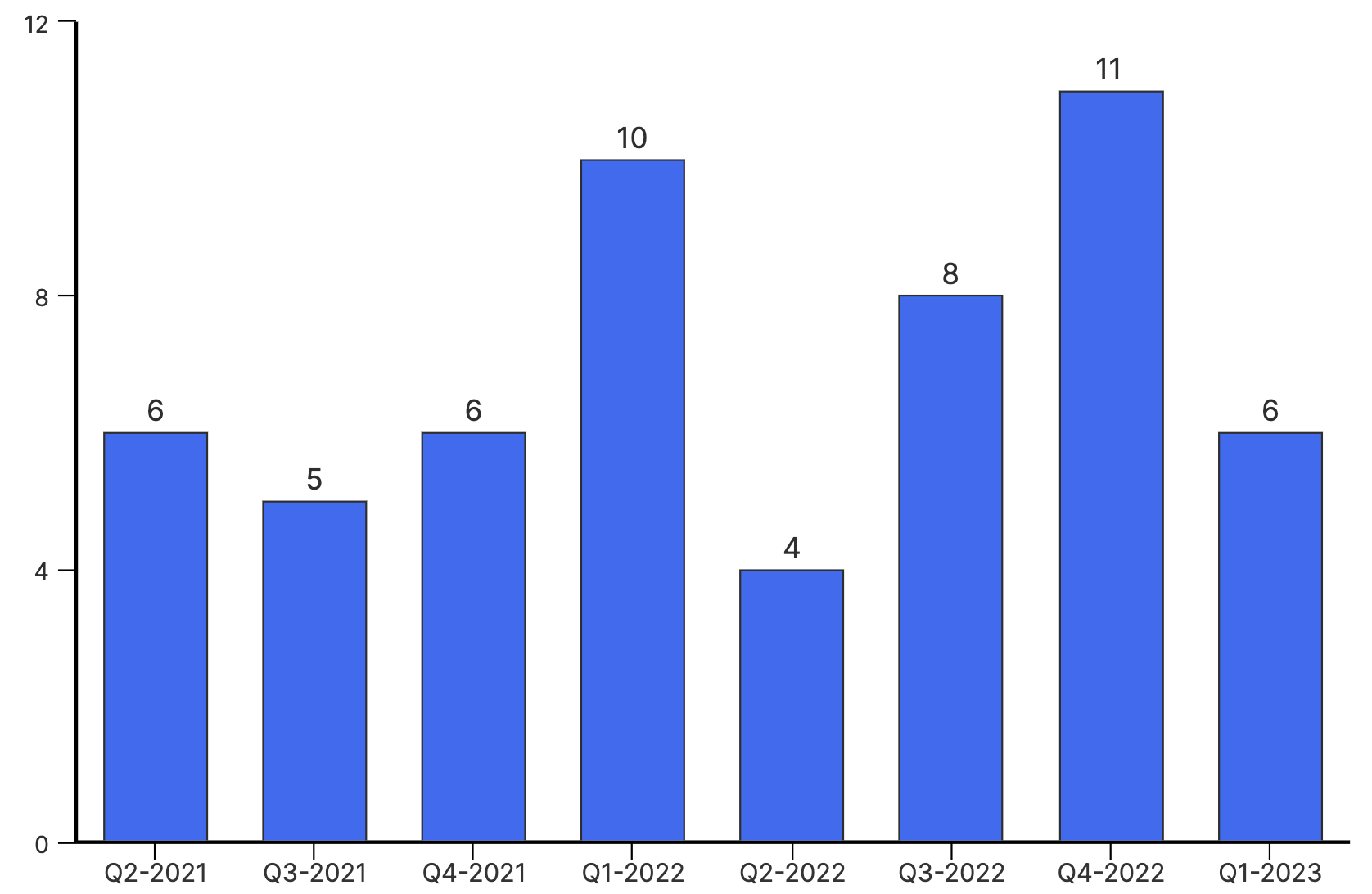

With the article topic in mind, we decided to exclusively drill down into Tire & Services M&A activity on Axial over the last 24 months. Results below.

| Firm Name | Company Type |

| Cornerstone Business Services, Inc. |

Investment Bank

|

| Parkwest Business Partners |

M&A Advisory Firm

|

| Impact Health | Corporation |

| Oaklyn Consulting |

Investment Bank

|

| ACT Capital Partners |

M&A Advisory Firm

|

| Firm Name | Company Type |

| Tenaz Capital Co. | Family Office |

| Northern Rock |

Holding Company

|

| Kynance Equity Partners | Private Equity |

| LP First Capital |

Independent Sponsor

|

| Gravity Star Capital | Search Fund |

Private equity has been an important source of capital for businesses of all kinds seeking growth. It provides working capital, management expertise, and access to a broad range of resources required for strategic planning, management development, financial restructuring, and operational improvements.

Historically tire retailers largely steered away from PE backing—and the consolidation that often accompanies it. Larger regionals have started to work with private equity, but many others have turned away. But is that the right strategy?

PE firms—which according to some estimates still have $2 trillion to $3 trillion of “dry powder” they are eager to put to work—are now targeting large amounts of capital to the automotive aftermarket, and they’re not alone. Tire sales account for about 30% of revenue across the entire auto aftermarket industry—the biggest segment within that space.

According to the Automotive Aftermarket Suppliers Association (AASA), the aftermarket for U.S. light-duty vehicles totaled $324 billion in 2021, up 11% from $292 billion in 2020, mainly due to the impact of the Covid-19 pandemic. (The figures exclude the market for medium- and heavy-duty vehicles.) Industry growth is projected to slow to about 4% a year through 2024, which means there’s not a lot of room for PE firms to grow in the business without acquisition.

The main objective of PE firms is to grow their investments and then sell them several years down the road. The most obvious way to do this is through organic growth, but that seems less likely to happen in the tire business. That leaves acquisitions, which leads to consolidation.

To many retailers, consolidation carries a number of potentially negative consequences for the industry, including reduced competition, job consolidation, higher prices, lower quality services and most of all giving control of a family run generational business to professional investors. But forward-thinking players in the retail tire and service business believe consolidation brings a number of benefits.

Acquisitions enable an increase in market share and expansion into new markets, which might otherwise be difficult to achieve due to geographic distance and an owner’s aversion to risking his or her own capital. A larger company will be able to achieve greater economies of scale and thus lower costs through M&A. This could in turn lead to improved customer service and quality while increasing profitability at the same time—all good things for customers and shareholders! One of the greatest benefits of partnering with a private equity backed consolidator is the exit ramp provided for businesses owners looking to sell their companies, or the option to stay along for the ride and get a ‘second bite of the apple’ in a few years.

As consolidation within the auto aftermarket accelerates, suppliers and vendors can expect to see a continuation of the trend towards fewer, but larger, ownership groups, as well as the emergence of a new generation of entrepreneurs who will lead those groups once they reach critical mass.

In the U.S., PE buyers will most likely be looking to buy regional brands and expand them, using their brand strength, scale, lower costs, and larger coverage area to beat local chains that have already consolidated their footprints in their markets. They will also be looking for growth in the service market, as well as an opportunity to use the U.S. market as a test bed for international expansion. I believe you will see some private equity groups start to invest further into the automotive aftermarket by targeting parallel markets such as auto parts and tire wholesale.

The good news for retailers interested in consolidating is that they can expect well-funded operators with strong balance sheets who have no intention of cashing out of their investments quickly. We also expect that service outlets will be looking for buyers willing to pay a premium to build a national footprint, as well as having access to capital in order to make those acquisitions happen.

Consolidating private equity might appear intimidating at first, but with the right research it can be leveraged to benefit both buyers and sellers alike. Although the automotive aftermarket industry presents some degree of uncertainty in terms of growth rates, tires offer reassurance as they are predicted to grow nearly four percent in 2024. It is essential that decision-makers look at both the short-term and long-term outlooks when evaluating if consolidation is beneficial or not. Though fear is natural when faced with a significant change, understanding what comes next helps us prepare for its effects. Critical analysis should be applied to preparing for the opportunities ahead, making sure that the move towards consolidation will foster more positive than negative outcomes for those within the industry.