Top 25 Lower Middle Market Investment Banks | Q2 2026

Axial is excited to release our Q2 2026 Lower Middle Market Investment Banking League Tables. To compile this list, we…

Not since Lehman Brothers has mid-market deal volume been so low.

Mergers & Acquisitions reports that just 330 middle-market transactions were closed in Q1 2016, compared to 493 in Q1 2015 and 427 in Q1 2014. (The number for Q1 2009 was a paltry 236.) Deal value is also relatively low at $59.4 billion.

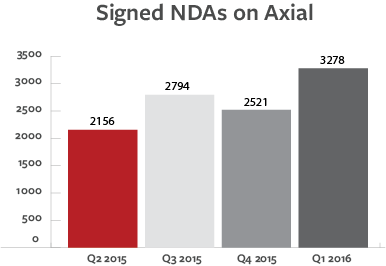

However, activity on the Axial network suggests the chance of a rebound in coming quarters. The number of signed NDAs increased 30% from Q4 2015 to Q1 2016 — suggesting the possibility of an accompanying surge in deals moving down the M&A funnel later this year.

Despite glimmers of hope, dealmakers today are looking at what is at best an uncertain future. Here are some of the key factors driving the downfall in M&A.

According to Eric Mattson, Principal at Excellere Partners, “The biggest factor impacting deal volumes right now is high valuation expectations, especially given the relative quality of the businesses and the implausible growth scenarios.”

As Mattson noted in a previous post, “Historically speaking, M&A value gaps are generally a result of specific market changes… that impact buyers faster than sellers’ expectations. It’s a little different in this market, as there hasn’t really been that shockwave event; rather, it seems that the strong valuations have simply caused sellers’ expectations to accelerate faster than most buyers’ pricing thresholds.”

For sellers, the first step in bridging the valuation gap is to come to terms with it. “Typically, owners overestimate business value because they appreciate how difficult it was to start and build a business to its current state,” writes Gary Ampulski, Managing Partner at Midwest Genesis. “Owners often use [their] optimism and lack of knowledge as license to postpone taking the actions necessary to take the outcomes they desire.” The job of an advisor is to help owners come to terms with the realities of the market and the negotiation process ahead.

Mattson notes that in addition to the valuation gap, “there has been some tightening within the debt markets, which makes it even harder (especially for PE sponsors) to get high priced deals done.” As John Finnerty, a group head at NXT Capital Corporate Finance, observed earlier this year, “We are definitely seeing tightening across credit markets due to concerns over the global economy and volatility in the stock and broadly syndicated markets.” However, experts note that tightening credit seems primarily to affect larger deals, particularly those above $250 million — good news for the lower-mid and mid-market.

Still, the overall trend has led to a decline in private equity-backed deals, as strategics or other well-capitalized buyers acquire targets that in another market, could have been anyone’s game.

Uncertainty like that surrounding a presidential election is inevitably disruptive to investment markets, says Mattson. “Also, because Donald Trump is a relative political unknown, there’s an additional level of uncertainty around him.”

However, Mattson says, “anecdotally, there doesn’t seem to be the same election ‘paralysis’ in M&A that we’ve seen in the past. Perhaps that’s because no one is giving Mr. Trump much of a chance in November, so there’s less perceived uncertainty; or perhaps it’s because there’s less economic policy (that impact M&A) between Trump and Clinton as there has been between prior candidates.”

In a March Forum survey, 55% of dealmakers chose Trump from a still-crowded field as the best candidate to represent corporate interests.