Top 25 Lower Middle Market Investment Banks | Q2 2026

Axial is excited to release our Q2 2026 Lower Middle Market Investment Banking League Tables. To compile this list, we…

Public companies at or near their all-time stock price highs, top-line pressure constantly bearing down on CEOs, and access to cheap debt as if it were 2007 have created a strategic buyer environment that has private equity firms getting blown out of the water trying to win good deals.

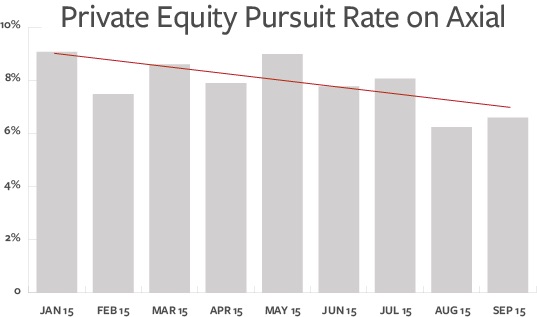

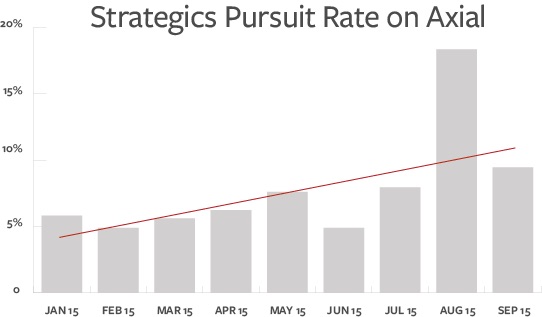

PE’s share of M&A deals is the lowest it’s been in 14 years: As of August, only 5% of the $2.6 trillion of deals announced this year were private equity backed. On Axial, the rate at which corporate buyers are pursuing deals has nearly doubled since the beginning of 2015, while the rate for private equity firms has decreased by 20%.

According to Preqin, private equity firms have raised $694 billion in 2014 and the first two quarters of 2015 — so they can’t really sit on their hands too long waiting for lower prices. When markets favor the strategic buyer, there are four things a private equity team can do to outcompete strategic buyers with lower costs of capital and credible post-M&A synergies.

“In my experience, most business sellers — especially in the lower middle market — care deeply about what happens to the company after they sell,” says Ed Irwin, partner at Shore Points Capital. “In some cases it’s because they’re retaining a stake, but in almost every case it’s because they are leaving behind loyal employees and managers who helped make the company successful. In addition to valuation considerations, they invariably want to leave their company in good hands.”

Entrepreneurs want to work with the sharpest financial partners in their industry. Some entrepreneurs will accept lower valuations for their business in exchange for getting to work with the best investors in their markets. “If we, as a buyer, can distinguish ourselves through our industry knowledge and experience, we have an edge over the less experienced buyer,” says Irwin. “With so much competition on the buy side, that experience is more critical than ever before.”

Being the best means focusing on specific markets and industries and breaking away from the the opportunistic generalist mindset that is private equity 1.0. “At Shore Points, we started out in 2006 with a purely generalist approach but now we are focused primarily on enterprise software and technology enabled service companies. It’s been a natural progression for us and I definitely see us continuing to move in that direction.”

Being the best usually also means you’re sharing your expertise with your industry — think publishing and speaking at conferences — and making sure people can find and engage you on the the right deals.

“As a private equity buyer in the lower middle market, we believe our primary advantage relative to strategic buyers is our ability to custom-tailor deals to those sellers who want to remain with the business post transaction,” says Eric Korsten, managing director at Branford Castle Partners. “We let sellers openly speak with senior executives at our existing portfolio companies to understand life within our organization. This generates a level of comfort with us as a private equity buyer and is a key competitive advantage.”

Korsten identifies a few specific deal terms that can benefit his firm over specific buyers, including:

Private equity organizations are (or should be) small and nimble compared to big public companies. Be faster than them and you’ll have a huge leg up. On Axial, the first member that responds to a privately shared deal is 20% more likely to close it than the second respondent.

This logic applies not just to the first response but to the M&A process as a whole. Most entrepreneurs would prefer to avoid a large and long formal M&A process, but they do it because it helps them keep buyers accountable to timelines. When you’re the smartest investor in a particular space and you’re able to move fast, many entrepreneurs will give you an inside look before running a broader process. It’s one of only a few remaining narrow alleyways through which investors can get a proprietary deal done.

Take a pause from investing in new platforms, take a careful look at your portfolio and who your best CEOs are, and bet big on a few of your portfolio companies, putting meaningful incremental capital to work with your existing platforms. Outperformance can come from executing on this strategy.

Jay Jester is managing director at Audax Private Equity, a firm founded specifically around a buy and build strategy. “We saw a real opportunity,” says Jester. “Buying in the lower middle market, and scaling up companies we can sell into the very frothy, very crowded middle market has been our strategy since day one.”

Financial sponsors seeking add-ons often have inherent advantages over strategics. “A lot of strategics may be thinking about corporate development on a part time basis. When they see an add-on acquisition they want to pursue, not only do they have to figure out how to compete in a hot market — they also have to construct a team from different parts of the organization,” says Jester.

“Our team of managing directors has been together on average well over a decade. We’re able to move a lot faster. The team’s ready to go, ready to deploy on these add-on acquisitions — just because it’s Monday. At a strategic, everyone has a day job to balance too. Build and buy is the only thing we do, and we’ve got the entire firm focused around it.”

Average buyout multiples are more than 10x right now — the highest level in two decades. With M&A activity nearing all-time highs and strategic buyers dominating the buyer landscape, private equity firms are on their heels trying to figure out how to win deals without paying huge multiples. To win in this new world, PE firms need to re-invent themselves. Otherwise, strategics will continue to rule the M&A roost.