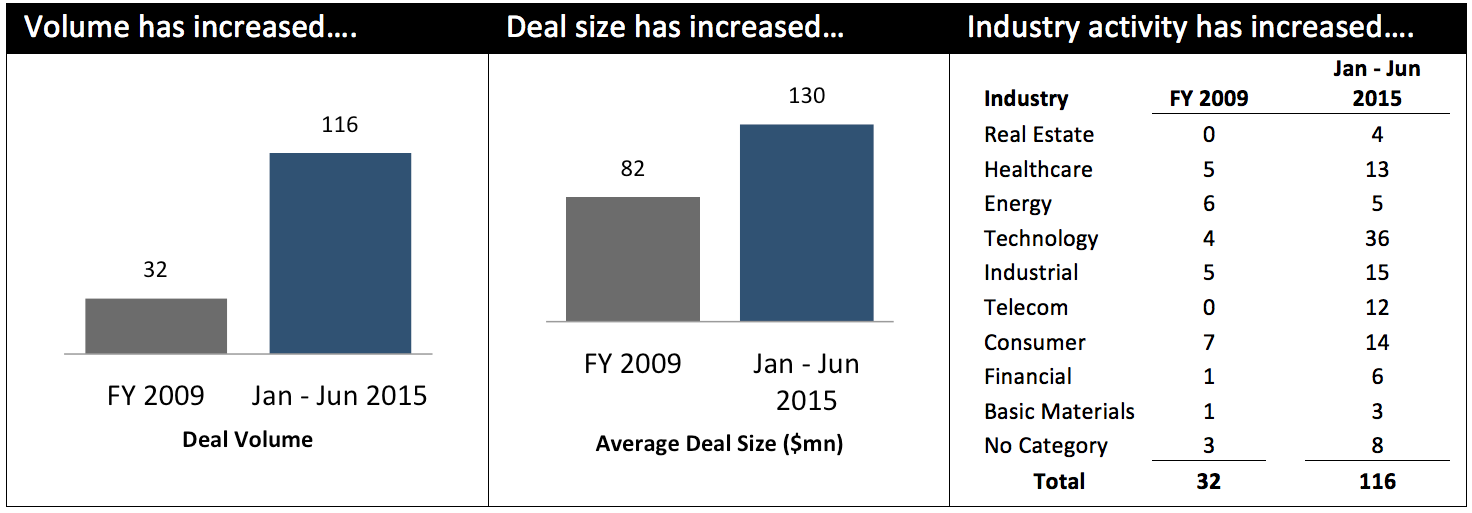

The Advisor Finder Report: Q2 2026

Welcome to the Q2 2026 issue of The Advisor Finder Report, a quarterly publication that surfaces the activity occurring on…

Tags

There has been a lot press lately about China – mostly about their stock market and real estate bubble and pollution. More interesting to us is the fact that China has been aggressively buying US real estate, and more importantly, US businesses across multiple industries. If you are considering a sale process, Asia buyers should be on your list. Properly managed, this strategy can create additional price competition from a universe of buyers with a strong competitive incentive to establish a US presence.

China is the third largest overseas investor with foreign direct investment (“FDI”) approaching $100 billion dollars annually, nearly doubling since 2009. Much of this investment flow has historically been focused on acquiring natural resources and basic materials that fueled the rise of China’s core manufacturing base and infrastructure build out. Resource rich, under developed countries were the main beneficiaries of China FDI over the last 10 years.

Today, as China moves decidedly into a more consumer driven economy (with support from the government and a rising middle class) it must also move up the value chain by acquiring technology, brands and service capabilities. Furthermore, rising wage pressures at home and pricing pressure in the market place are squeezing already tight margins among (largely undifferentiated) manufacturers. Controlling more of the value chain is a strategy that is gaining momentum among founders and senior management teams across China. Reflecting this new reality, outbound M&A from China to the USA has increased 3.6x from 2009 through the first 6 months of 2015.

As a case in point, we recently engaged with a client who manufactures certain professional metal and woodworking equipment for well-known brands in the US and Europe. This company provides all the design, engineering and manufacturing for these brands. The Company is being squeezed by labor costs and customers. Moving operations to Vietnam or another low labor cost country is only a short term solution and would require a few years to transition successfully. The only viable option for this client, and many more like them, is to move up the value chain and acquire brands or customers in the key markets they serve. Companies like this make natural and motivated buyers for certain US assets.

Opening the sale process to overseas buyers – some considerations

A sale process that contemplates non US buyers has to be configured differently than a purely US centric process. The practical challenges include language and time zones (we will dive into cultural considerations in another article). Expect turn-around times during the due diligence process to take longer, to be more iterative and require a lot more hand holding than might otherwise be expected. However, these are manageable challenges provided they are considered ahead of time and the process remains flexible enough to accommodate an overseas buyer. Insisting that an overseas buyer have an M&A Advisor as a prerequisite to being allowed into the process can also minimize disruptions and delay. Cross border experience and a track record of actively (perhaps overly) managing buyer expectations and timetables is a plus. In our own practice, conducting an “M&A Readiness” assessment is a critical process we undertake when contemplating a relationship with a potential buyer. A few of the things we look for:

Outbound M&A from China to the US will continue to grow, driven by economic and strategic imperatives. In many situations, these buyers can be very competitive bidders. With some additional planning and proper management, there is every reason to include Asia buyers in a sell side process.