Industry Report: Home Renovation & Remodeling [Bridgepoint IB]

Key Report Highlights Homeowners Continue to Favor Renovation Over Relocation: The U.S. residential remodeling market reached approximately $523 billion in…

The healthcare system remains highly fragmented in the US, with care covered by a wide range of payers and providers. However, this fragmentation also represents a host of opportunities for engaged investors to address — from reducing costs and inefficiencies to improving the coordination of care. In addition, the healthcare system has undergone a period of radical change in response to the COVID-19 pandemic.

As Terry Wang, a partner with Regal Healthcare Capital Partners, recently observed during a virtual roundtable hosted by Axial’s founder & CEO, Peter Lehrman, “COVID has highlighted the importance of telehealth and home health. Those two areas look fundamentally sound for the future, but some businesses like urgent care are simply not going to have the same volume of testing as it did during the pandemic.”

Indeed, much of the pandemic’s disruption to existing patterns of care now appear permanent, while others are beginning to revert to historic practices. These complementary forces have served as accelerants to the consolidation trends already taking shape prior to the pandemic, with significant implications for providers, payers, and patients across the LMM going forward.

“All remote services will see sustained growth in the coming years,” Zak Eisenberg, a VP with Merritt Healthcare Advisors, remarked during the roundtable. “Another large trend is the shift to outpatient services, so while urgent care may not have as much volume due to COVID, they will have larger volumes of people who may have gone to the ER pre-COVID but are now trying to stay out of hospitals.”

The trend towards consolidation in the healthcare industry emerged in recent years as a response to a combination of factors, including how the Affordable Care Act created incentives for providers to improve efficiency and coordination of care. More to the point, private equity firms targeting the LMM have pursued substantial buy-and-build strategies to achieve economies of scale that lead to cost savings.

“From a structure and value standpoint, cost of debt is certainly a factor. We tend to be more conservative on the leverage side. In terms of volume, we have seen more on the add-on side rather than the new platform side,” Mike Forsyth, VP with Excellere Partners, pointed out during the roundtable. “Operationally, the supply chain has been a big factor for manufacturing-oriented businesses [in the space]. On the services side, wage inflation has also been a big issue in terms of turnover rates for clinicians and nurses.”

And consolidation trends are likely to continue well into the future as healthcare costs continue rising and the overall population continues aging in the US. Finally, several supporting factors should not be overlooked in this context:

Meanwhile, LMM healthcare providers often have fewer resources than their larger counterparts and are less likely to be able to offer their patients as wide a range of services. That has put the most promising targets into play. Not only have larger hospital systems increasingly turned to expansion via M&A, but PE-backed platforms have increasingly deployed a buy-and-build approach to create greater economies of scale with the resulting Managed Service Organization (MSO) turning these platforms into regional players capable of providing patients with a similar diversity of services. And cost reduction for these groups represents a real advantage.

“It’s a huge needle mover. A total joint in a hospital for example can be $30-50 thousand whereas it might be $12-15 thousand in an outpatient clinic,” Eisenberg observed during the roundtable.

This pricing dynamic has recommended physician-led clinical practices as attractive targets for healthcare investors. First, these practices tend to be very well-run and efficient, with lower overhead costs. Second, physician-led practices often have strong relationships with their patients, which can lead to higher rates of satisfaction and loyalty. Finally, these practices tend to be located in more lucrative markets for healthcare services.

Axial’s deal activity data confirm these accounts of the forces reshaping the investment opportunities across healthcare’s LMM coming into 2022. But before tucking into the numbers, a necessary caveat: deal activity conducted and tracked via Axial does not represent a comprehensive record of all LMM transactions. Rather, with thousands of active members using the platform, Axial’s dataset captures the drivers of dealmaking in this vibrant corner of the private capital markets.

In addition to aggregate value and total volume, Axial’s tracking of buy- and sell-side mandates reveals both a robust demand for and an even more profound supply of assets coming to market across healthcare’s LMM. The number of new buy-side mandates on the Axial platform for healthcare opportunities topped 150 last year, representing a leap of roughly a third year-over-year. And through early May, the count of fresh buy-side mandates has already reached 45, putting it on pace to match the annual tally recorded in 2021 with a strong performance predicted for the back half of this year.

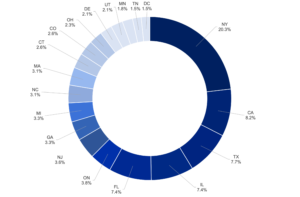

Axial’s data on deal activity across healthcare’s LMM also reveals some palpable geographic trends taking shape since the start of 2018. On the buy-side, a fifth of all mandates source from New York state, followed by 8.2% for California, 7.7% for Texas, and 7.4% for Illinois and Florida alike.

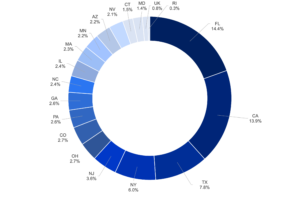

By contrast, New York represents just 6% of all sell-side mandates in Axial’s dataset over the same period. On this front, Florida leads at 14.4% of the healthcare asset supply followed close behind by California at 13.9% and Texas at 7.8%. Illinois, for its part, represents just 2.4% of the sell-side. Across the board, nearly all mandates on both the buy- and sell-side are for full acquisition of the business.

Axial’s data on healthcare reflects a LMM dominated on the buy-side by independent sponsors at 51.1% of all mandates since the start of 2018. These investors are followed by PE funds at nearly 20% and strategics at 15.5%. Altogether, investors targeting healthcare’s LMM have an appetite for assets generating a median maximum in revenue of $50 million and a median maximum in EBITDA of $10 million.

On the sell-side, the number of new mandates captured on the Axial platform reveals a supply glut that has only expanded since the start of the pandemic. Since the start of this year, 141 new targets have entered a robust pipeline. In 2021, more than 630 LMM healthcare assets came to market, representing a slight increase over the prior record set in 2020. By early May, though, 53.1% of sell-side targets first recorded last year are still seeking buyers.

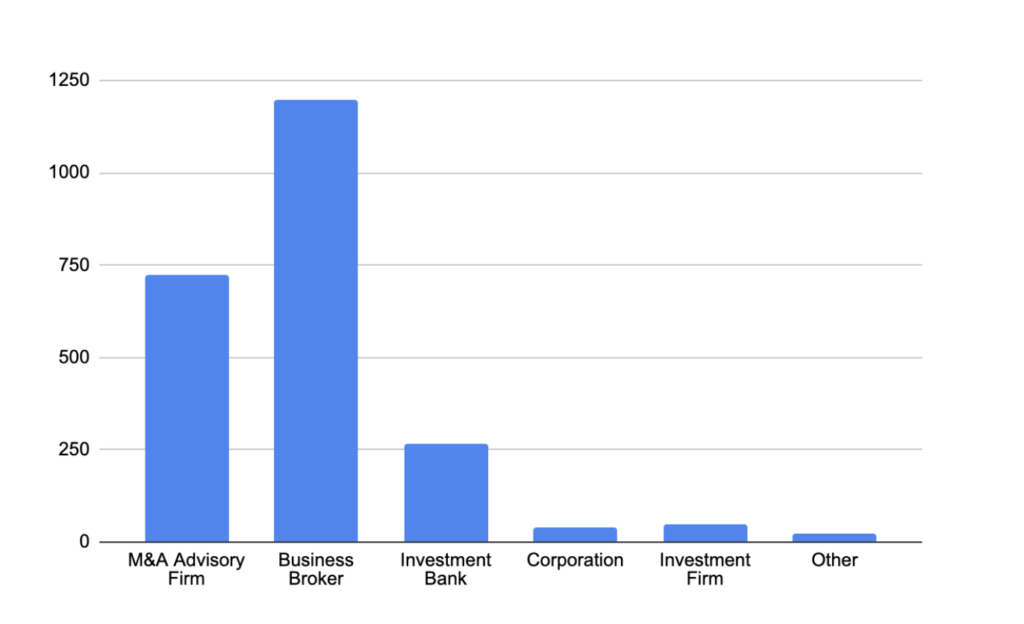

Activity on this side of the negotiating table is dominated by business brokers and M&A advisory firms, with investment banks running a distant third.

As the healthcare industry continues to consolidate, physician-led clinical practices are set to remain a key target for M&A activity. Investors are drawn to these practices for their efficiency, patient relationships, and geographic location. As a result, we are likely to see more private market consolidation across the LMM healthcare sector in the coming years.