The SMB M&A Pipeline: Q2 2026

Welcome to the Q2 2026 issue of The SMB M&A Pipeline, the quarterly series that surfaces a top-of-the-funnel breakdown of…

Earlier this year, public indices entered bear market territory for the first time since panic over the COVID-19 pandemic derailed one of the longest bull runs in history—albeit for only a month—in early 2020. By contrast, today’s markets are flashing signs of a more sustained downturn going forward. The S&P 500 posted its worst first-half performance in more than half a century this year, while IPOs have all but disappeared for the time being at least.

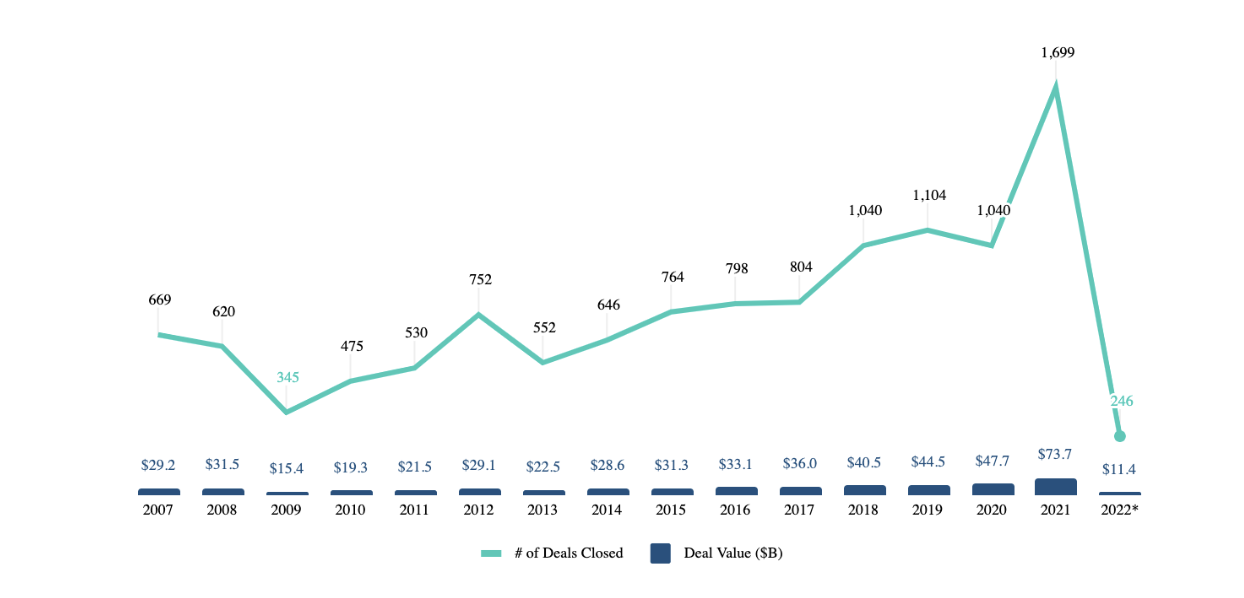

However, deal flow through the wider middle market has proven far more resilient following record-setting results for aggregate value and overall volume coming into 2022, per PitchBook’s latest report on this part of the private markets. And that general trend holds true of LMM deals as well. Private equity investors have generated $11.4 billion in deal value on 246 completed transactions. Those figures hold up against many opening quarters of the past decade and considerably outpace those for, say, Q1 2012 at just $8.1 billion in sum on 187 deals closed.

Despite deteriorating macroeconomic conditions and a recession looming on the horizon, the lower middle market in the US remains a notable bright spot. Dry powder represents a factor not to be ignored in this assessment. Moreover, the LMM is expected to continue growing in the coming years. That has investors primed to enter this corner of the market even as challenges may dog other areas. And this growth will be driven in no small part by small businesses scaling their operations as never before thanks in part to the expanded reach available from widespread digitization.

But there are several additional reasons for this resiliency. First, many companies in the LMM have been able to adapt their business models to changing conditions in recent years, with the pandemic proving something of a trial-by-fire period for small businesses forced to innovate on the fly. Second, financial sponsors have been increasingly able to help their portfolio companies to benefit from economies of scale. And third, they have diversified their revenue streams, which has helped to expand the scope of operations and to insulate small businesses from shocks to any one particular sector or region.

Of course, no shortage of challenges still confronts the LMM in the near term that savvy investors must tackle—some of which have not played a major role across markets for decades.

“The investor’s biggest challenge is to understand how supply chain issues would impact the potential investment. Unfortunately, there are still some unknowns,” Karen L. Small, a partner with Sterling Commercial Credit, has observed. “The other challenge is rising interest rates and inflation. A rising interest rate environment is familiar to investors around in the 80s and 90s. For new investors that have entered the market in the past two decades, this will be something they will have to learn how to cope with.”

While there are certainly risks to the LMM’s growth prospects, there are also significant opportunities thanks in no small part to one hallmark, above all, unique to the LMM: buyer and seller alignment.

If these charts were represented as Venn diagrams, there’d be some not inconsiderable overlap. Over the past several years, buyers and sellers have grown increasingly aligned across the LMM in the US. But before tucking into the numbers, a necessary caveat: deal activity conducted and tracked via Axial does not represent a comprehensive record of all LMM transactions. Rather, with thousands of active members using the platform, Axial’s dataset captures the drivers of dealmaking in this vibrant corner of the private capital markets.

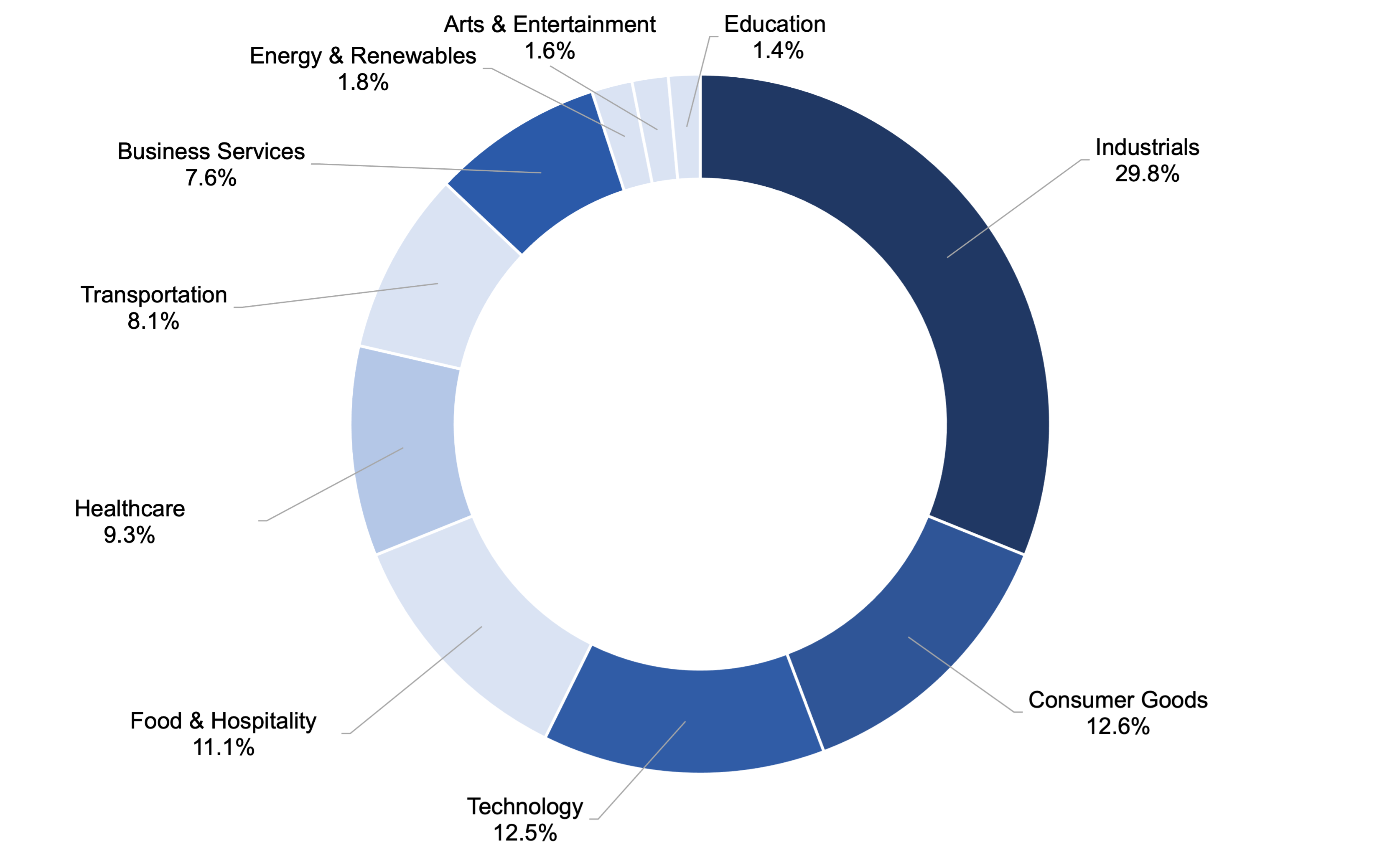

Since the start of 2019, seller activity has originated in the greatest number from the LMM’s industrials sector at nearly a third of overall supply followed at 12.6% by consumer goods, including retail as well as manufacturing and distribution & wholesale. Finally, technology, including information & software and maintenance & repair, represented 12.5% of deal activity.

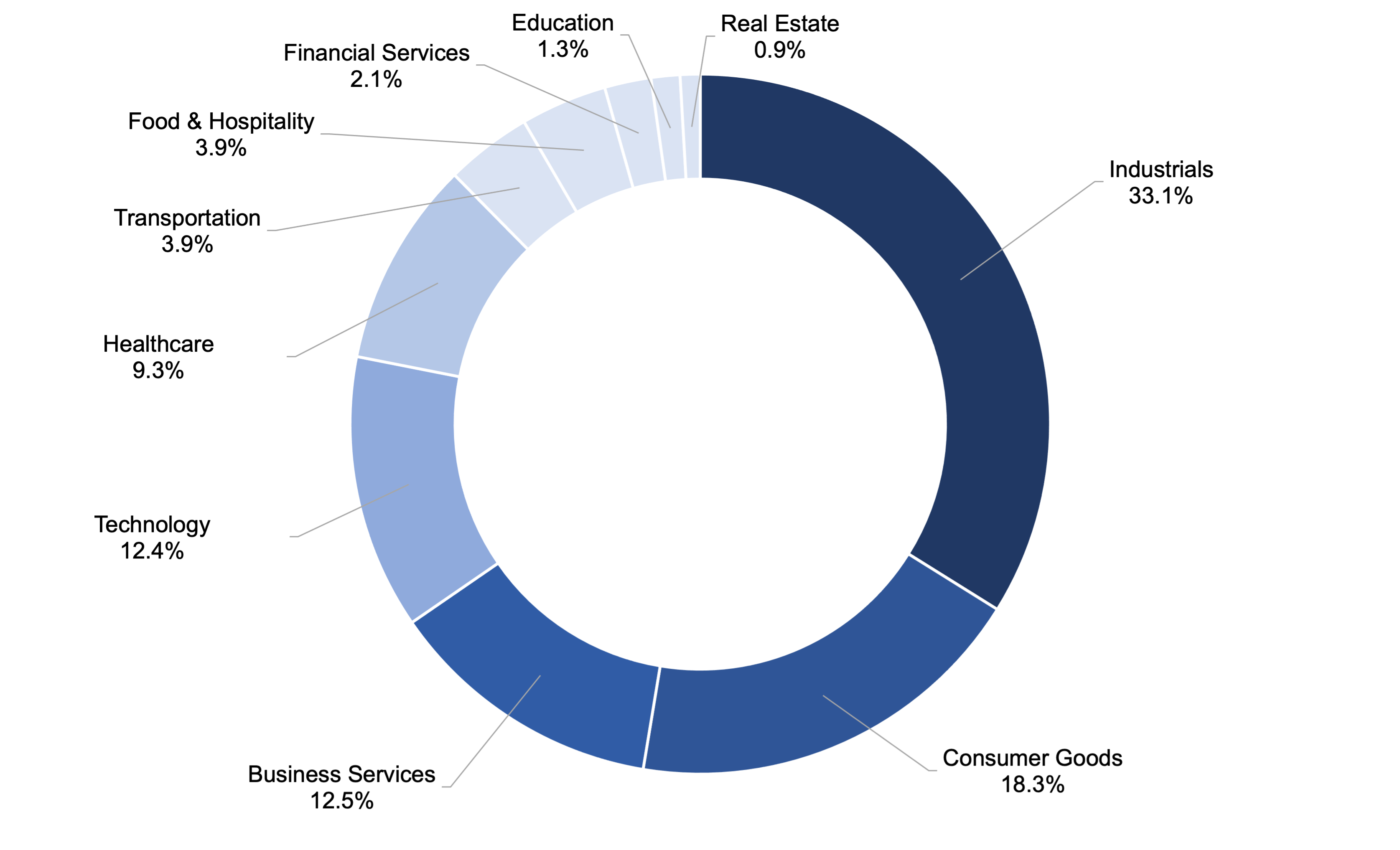

Although somewhat more concentrated than the sell-side, demand on the buy-side has largely replicated these results over the past few years. Industrials, including manufacturing and distribution & wholesale, has led all other verticals at 33.1%. Meanwhile, consumer goods, business services, and tech rounded out the top sectors in demand at 18.3%, 12.5%, and 12.4%, respectively.

These data on buyer and seller alignment comport with Small’s advice for investors going forward: “Stick to what you know best. This is not a time to experiment with industries you may not necessarily be familiar with.”

The LMM is a segment of the economy that includes companies with annual revenue between $10 million and $250 million. These companies are typically too small to be listed on major stock exchanges, but they are still larger than most privately held businesses. LMM companies are typically family-owned businesses or private equity-backed firms.

Despite their size, LMM companies play a vital role in the economy. They account for a significant portion of economic activity and employment in the US. In fact, LMM firms make up about one-third of all private sector businesses in the country.

What’s more, LMM companies are often at the forefront of innovation. They are often able to move quickly to take advantage of new opportunities than their smaller peers, and they are not burdened by the same organizational complexities as larger businesses. This agility has helped LMM firms weather many economic storms. And the present prospect of another recession is no exception. LMM firms have demonstrated a remarkable ability to adapt and thrive in the face of macro-level disruptions. This resiliency is likely to continue in the coming years, as LMM firms continue to innovate and grow.

All the same, it’s important to remember that not all markets are created equal. The LMM in the US has shown resiliency in the face of macroeconomic conditions. In particular, private equity firms have been quick to take advantage of lower valuations and increased buying power. In fact, the current environment presents a unique opportunity for private equity firms to buy LMM companies at a discount.

What makes the LMM so attractive to private equity firms? There are a few key factors:

In short, the LMM provides a unique opportunity for private equity firms to invest in companies with strong fundamentals that are well-positioned to weather economic challenges. By taking advantage of lower valuations and increased buying power, private equity firms can position themselves for success in the coming months.