The Advisor Finder Report: Q2 2026

Welcome to the Q2 2026 issue of The Advisor Finder Report, a quarterly publication that surfaces the activity occurring on…

Is technology in the early innings of fully automating the M&A banker?

Earlier this year, CB Insights put out a 45-page report titled Killing the I-Bank. This topic seems to gain a few attention-grabbing stories each year (see here, here, and here). The CB Insights report details the ways in which technology is affecting all aspects of investment banking — including M&A advisory, sales and trading, wealth management, capital markets, leveraged finance, and more.

With nearly half of Axial’s member base engaged in the M&A advisory profession, we study the topic deeply and continuously. The aforementioned report has led many of our members to ask Axial for our perspective on this subject. What follows is our consolidated thinking on the topic, which begins with a summarized breakout of what M&A advisors do and a corresponding assessment of how automation will and will not impact aspects of the sell-side M&A profession.

Our analysis leans heavily on some thoughtful work authored by McKinsey & Company, which has provided a useful framework for assessing the automation potential of various industries and jobs. In short, they assert that to accurately examine the technical feasibility of automation in a given field, one must study the discrete activities of that profession for their susceptibility to automation, not the profession as a whole.

To accurately examine the technical feasibility of automation in a given field, one must study the discrete activities of that profession for their susceptibility to automation, not the profession as a whole.

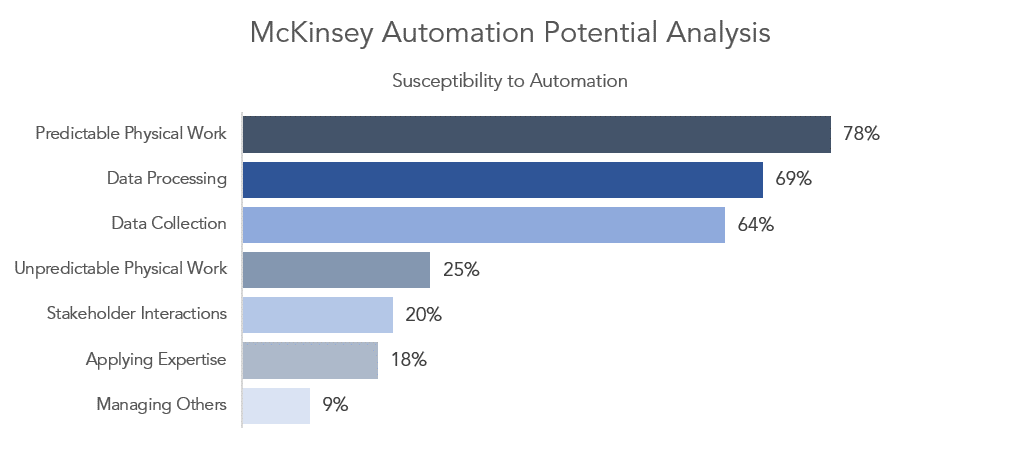

The chart below shows the broad categories McKinsey breaks out for this purpose — repeatable, predictable physical work is the most highly susceptible to automation, along with data processing and collecting. Other types of physical work are a somewhat susceptible, as are so-called “stakeholder interactions.” The least automatable types of activities involve applying professional expertise and managing others; in other words, these are activities where humans continue to have major and enduring advantages over computers.

Figure 1: The McKinsey automation susceptibility framework

To begin, we broke down the key activities of sell-side investment banking (note: we excluded the business development aspects of investment banking to maintain focus on transaction execution. Investment banking business development is arguably the least susceptible to automation given how business owners select their M&A advisor).

We placed the key activities into two major categories to provide guidance on the many activities that fall within them:

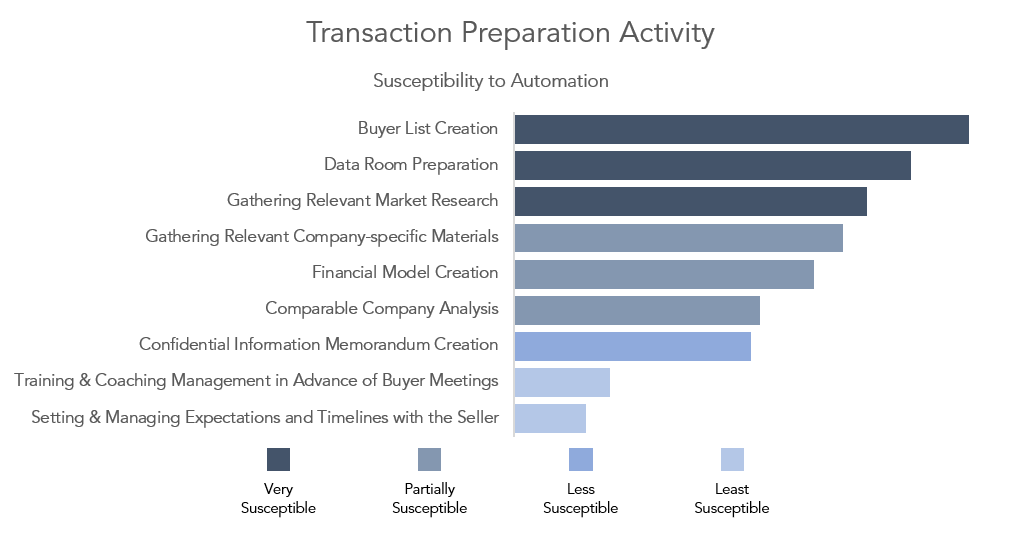

Transaction Preparation:

Transaction preparation includes gathering data on the business; creating buyer lists; and producing pitchbooks, historical and projected financial models, CIMs, and other necessary transaction materials and exhibits. Transaction preparation also involves preparing the owners/management for management meetings and subsequent negotiations.

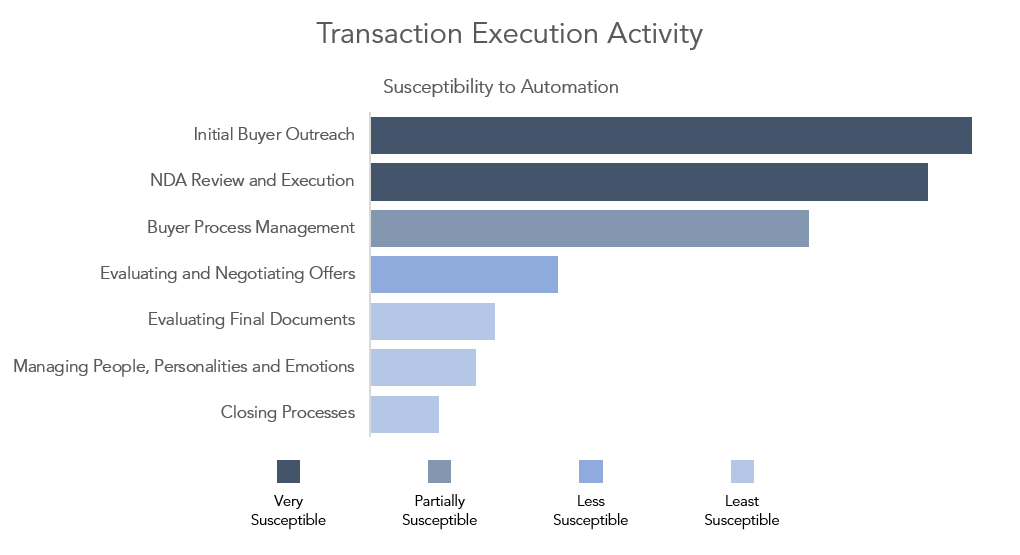

Transaction Execution:

Transaction execution refers to all activities involved, from initial buyer outreach to a closed deal. This includes all buyer outreach, all document sharing and execution (including NDAs, CIMs, and financial models), ongoing buyer process management, evaluating and negotiating offers, managing personalities and emotions, and the closing process itself.

Using the McKinsey automation feasibility framework above, we identified many of the activities in each category and employed our judgment and knowledge of the investment banking process and profession to predict their susceptibility to automation.

Figure 2: Transaction preparation activity applied to the McKinsey automation susceptibility framework

Figure 3: Transaction execution activity applied to the McKinsey automation susceptibility framework

These charts show clearly that for every activity that may be automated, there are an equal or greater number of activities that machines cannot assume. And even in the most susceptible activities — arguably buyer list creation or initial buyer outreach — the sell-side investment banker is continuing to apply a significant amount of expertise and judgment.

As an example, the Axial buyer list generator is one of the most heavily used tools on our platform. It saves bankers hundreds of hours on every single sell-side investment banking assignment. But the tool creates no value if not employed by a professional who reviews the list; assesses it against client objectives; and executes a professional, curated outreach process.

Another example is Axial’s buyer outreach tools, which allow bankers to send to potential buyers highly personalized messages with the help of templates and other software-enabled tools. The efficacy of the note, the copy drafted by the banker, and many other judgment calls remain in order to achieve success.

As was the case with the arrival of Microsoft Excel, Capital IQ, and other transformative capital-markets-oriented databases and technologies, the banker’s human-centered capacity to employ judgment remains critical to client success.

The banker’s human-centered capacity to employ judgment remains critical to client success.

In sum, we continue to view the investment banking profession as highly resistant to automation based on an analysis of the activities that it entails. We therefore view software and technology as positive sum sustaining technologies. It is in these types of industries where the questionable assertion that “technology creates much more opportunity than it replaces” appears to in fact remain true.