Introducing The Lower Middle Market Add-On Report

A survey of 150 deal professionals across the Axial network documents the extent to which financial sponsors have descended upon…

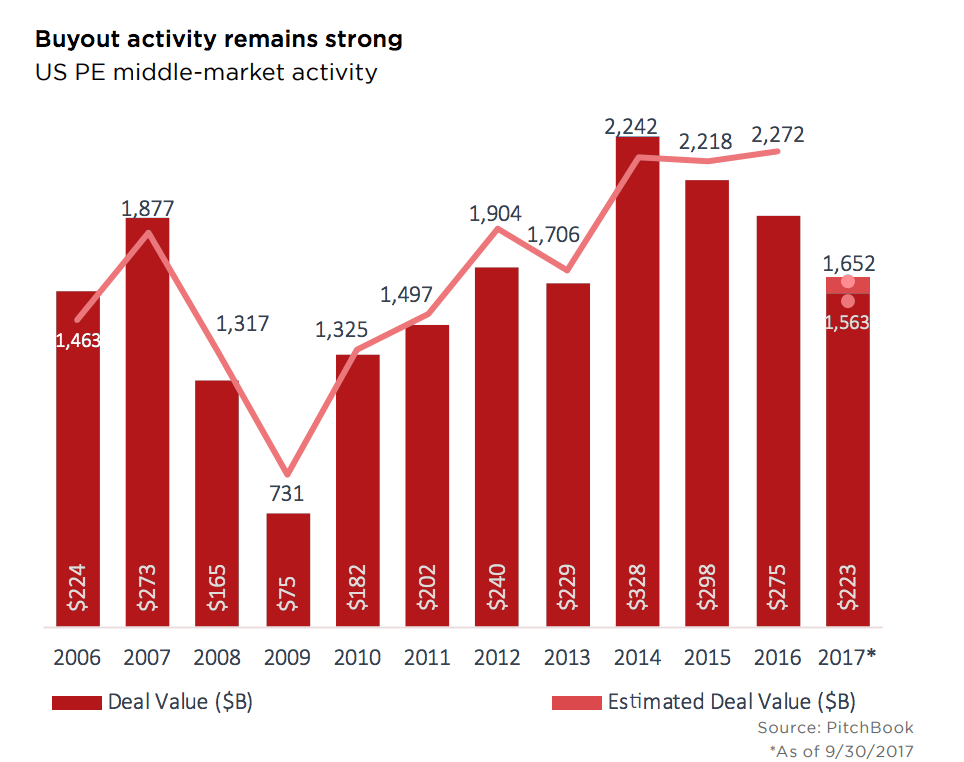

A recent PitchBook report shows that US middle-market deal flow has been robust through the third quarter this year, totaling $233bn across 1652 deals. The fourth quarter activity will continue to be strong with at least $51bn worth of middle-market deals announced, but not yet closed, according to the PitchBook data.

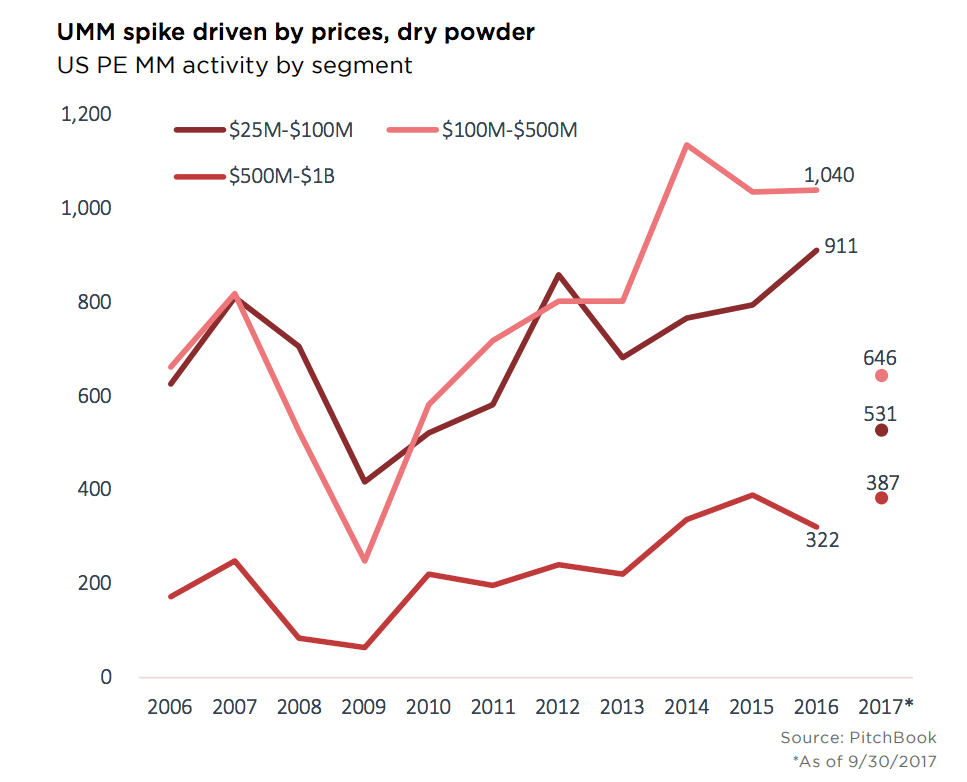

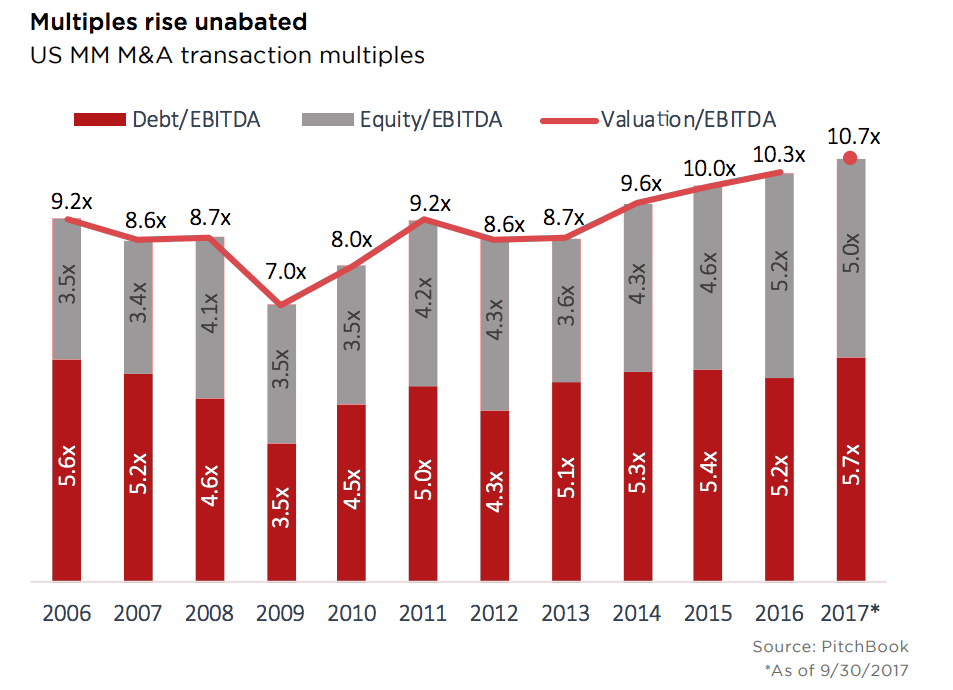

Based on PitchBook data, total deal value in Q3 is 13% higher than it was a year ago, while the total deal volume is 1.5% lower year on year. The reason is primarily a result of a spike in upper-middle-market (companies with $500m to $1bn in EVE), which witnessed 387 deals totaling $129.7bn in the third quarter, according to the report. PitchBook said that the abundance of dry powder and fierce competition for limited acquisition targets have led the median middle-market M&A ebitda multiples to climb to 10.7x through the quarter, the highest level on record.

Based on PitchBook data, total deal value in Q3 is 13% higher than it was a year ago, while the total deal volume is 1.5% lower year on year. The reason is primarily a result of a spike in upper-middle-market (companies with $500m to $1bn in EVE), which witnessed 387 deals totaling $129.7bn in the third quarter, according to the report. PitchBook said that the abundance of dry powder and fierce competition for limited acquisition targets have led the median middle-market M&A ebitda multiples to climb to 10.7x through the quarter, the highest level on record.

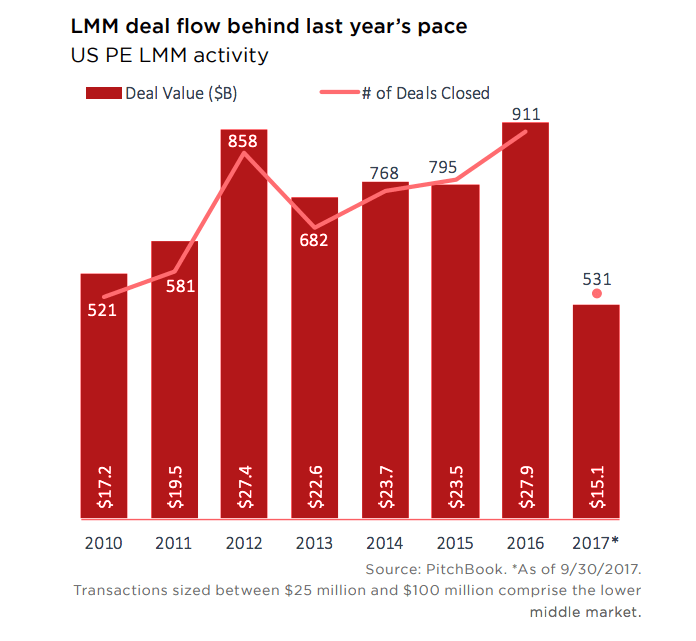

The lower-middle-market ($25m-$100m), though, after its record term in 2016, reported a lower PE activity level in Q3 2017, with only $15.1bn invested across 531 deals. “Rising enterprise value/ebitda multiples are likely playing a role, as companies that may have been classified as lower-middle-market in recent years have seen their prices inflated,” the report said.

PitchBook also noted that lower-middle-market companies are often ideal targets in buy-and-build strategies, which have experienced a groundswell of popularity as PE firms focus more on operational improvements. “To that end, many prime lower-middle-market targets have already been tacked on to larger platform companies.”

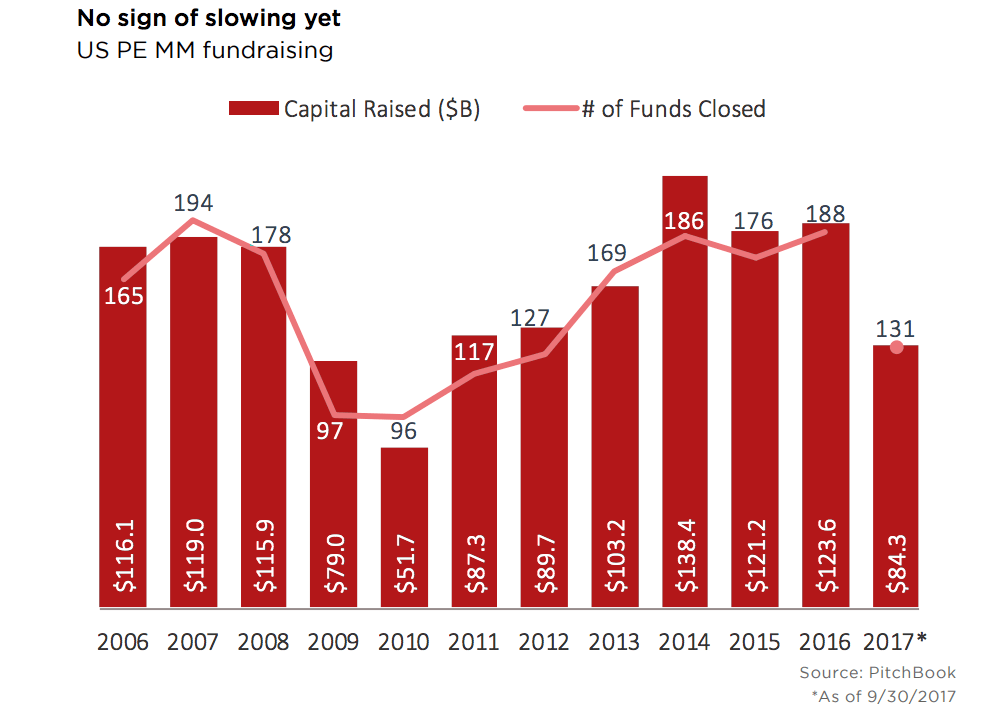

On the fundraising side, middle-market PE funds have raised $84.2bn across 131 funds through Q3, a 2.5% year-on-year increase in value and a 6.4% decrease in volume. The report projects that PE funds will have a stellar year of fundraising in 2017.

“Fundraising has grown in recent years due to PE’s long-term outperformance of most other asset classes, as well as positive net cash flows globally to LPs of PE funds every year since 2012, allowing them to recycle capital back into the asset class,” the report said.

The growing valuations in public equities, which create a reverse denominator effect for most LPs, have also fueled the growth of PE fundraising. PitchBook projects that one potential hurdle to PE fundraising in 2018 might be the aforementioned net cash flows to LPs are likely to turn negative due to the downturn in exits. “So LPs may have fewer dollars to reinvest into private markets; however, we think that overarching industry dynamics point to continued strength in fundraising,” the report said.

The report also notes that first-time managers, more than 99% of whom fall into the middle market, have made a comeback in recent years. PitchBook’s research findings show that 23 first-time middle-market funds held final closes in the US in 2016, taking in $8.6bn in total commitments – each of which is the highest since 2009 (when final closes were held for funds that began raising prior to the financial crisis).

“We expect more first-time managers to continue striking out on their own in the coming quarters, especially if overall PE fundraising continues at its rapid pace.”

Click here to see the report.