How Coronavirus Is Impacting Lower Middle Market M&A Activity

Last week, Axial convened a virtual roundtable of members to review the impact of the coronavirus pandemic on lower middle…

Tags

The independent sponsor business model combines the rigor of traditional private equity with deal-by-deal investments and economics. Many independent sponsors pitch that their model has stronger limited partner investor alignment on issues such as fees, carry, and discretion to review each investment opportunity when highlighting the attributes of their model.

Independent sponsors’ limited partner capital generally comes from four sources: private equity firms, friends and family, hedge funds, and family offices. Depending on the deal, some sources of capital may be more suitable than others. For instance, established private equity firms with capital ready for deployment will be more likely suited for larger deals in which they can play an integral role in the deal closing and insert a representative of the firm in the acquired company in an operational function. On the other hand, family offices are more likely to participate in smaller deals; they will likely permit the independent sponsor to run the deal and expect the independent sponsor to handle the operational role post-closing.

What makes independent sponsors attractive to financial partners?

First, they provide exposure to deals that the financial partner may not have otherwise come across. The independent sponsor may have relationships stemming from an industry or geographical expertise that exposes a financial partner to previously unrecognized investment opportunities and possibly to companies that are not even officially for sale. Second, independent sponsors can offer operational and industry expertise that many investors, whether established private equity firms or otherwise, find attractive and which may ultimately contribute to the success of the investment post-close.

Why does the independent sponsor business model continue to gain momentum?

Over the past several years, aspiring private equity fund managers looking to launch funds have faced unprecedented barriers to entry. Dodd-Frank’s fund registration requirements have made it more difficult than ever for start-up funds. Also, it remains extremely challenging for first- time funds to raise capital. Limited partners generally have begun to put greater sums of capital in fewer funds and have gravitated toward well-known funds with proven management track records.

Meanwhile, there are few barriers to entry for the independent sponsor business model. Today’s experts believe there are about 1,000 firms acting as independent sponsors. Any deal professional willing to take the risk to start their own independent sponsor platform can do so. Technology and outsourced service providers will continue to make it easier and cheaper to start a platform. At the same time, the independent sponsor model continues to garner increased acceptance among lower-middle market sellers and investors.

What do successful independent sponsors credit for their success?

Axial polled their independent sponsor members to find out how they approach the market and why they chose the independent sponsor model. Below are some highlights from their survey:

What are the typical economics for independent sponsored deals?

What is clear after analyzing the data surrounding the independent sponsor market is that there are “standard” economics. Markets do tend to standardize economics as they formalize, but this process seems to still be nascent in the independent sponsor space. At a recent independent sponsor conference the following structural themes were highlighted by limited partners that have invested in the space.

Closing Fees to Independent Sponsor: 0% to 3% (most require at least 50% to be rolled into deal)

Management Fees to Independent Sponsor: $100K – 6% of EBITDA (largely dependent on activity level of IS post-closing and the size of the company)

Promote to Independent Sponsor: 7% to 50% after an 8% – 10% hurdle. This is a very wide dispersion. Factors that influence include hard dollars invested by the IS, time devoted by the IS to deal, and IS track record.

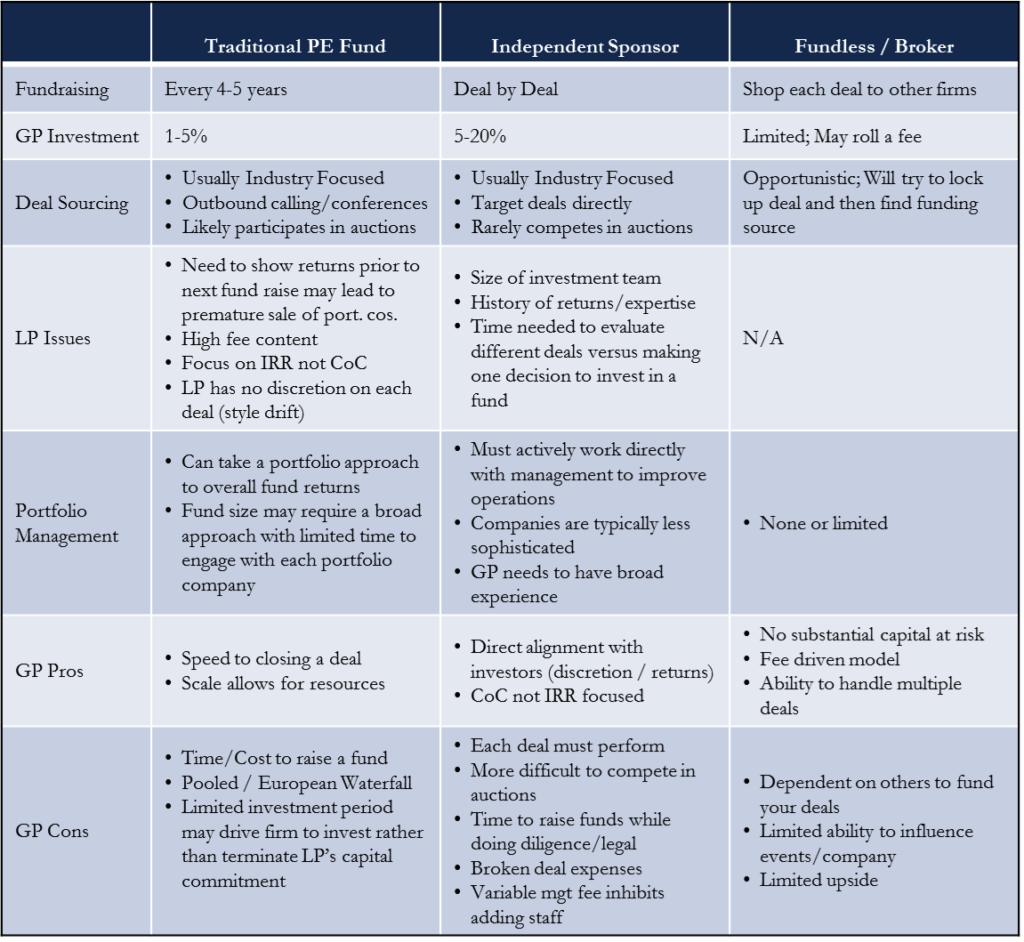

The chart below from Rotunda Capital shows the major differences between the three private equity models: