Dead Deal Report: Unpacking 2025’s Broken LOIs

Transactions can fall apart for a variety of reasons, including financing challenges, diligence-related findings, quality-of-earnings (QoE) discrepancies, or changes in…

Tags

The lower middle market is entering 2026 with a familiar mix of cautious optimism and hard-earned discipline.

Following a somewhat choppy 2025 shaped by macro volatility, shifting financing conditions, and persistent valuation gaps, dealmakers are beginning to see signs of stabilization. Capital remains active, advisors expect to win more engagements, and buyer interest in high-quality assets is holding firm—though alignment between buyers and sellers continues to determine whether deals ultimately get done.

This report draws on insights from a recent Axial member survey of 107 lower middle market participants across both the buy- and sell-side. It also incorporates comparisons to Axial’s mid-year 2025 sentiment survey, highlighting how perspectives on deal activity, valuations, and market dynamics have evolved over the past 6-9 months.

Together, the data and commentary offer a snapshot of what’s changing, what’s holding steady, and what it will take for improved sentiment to translate into completed transactions in 2026.

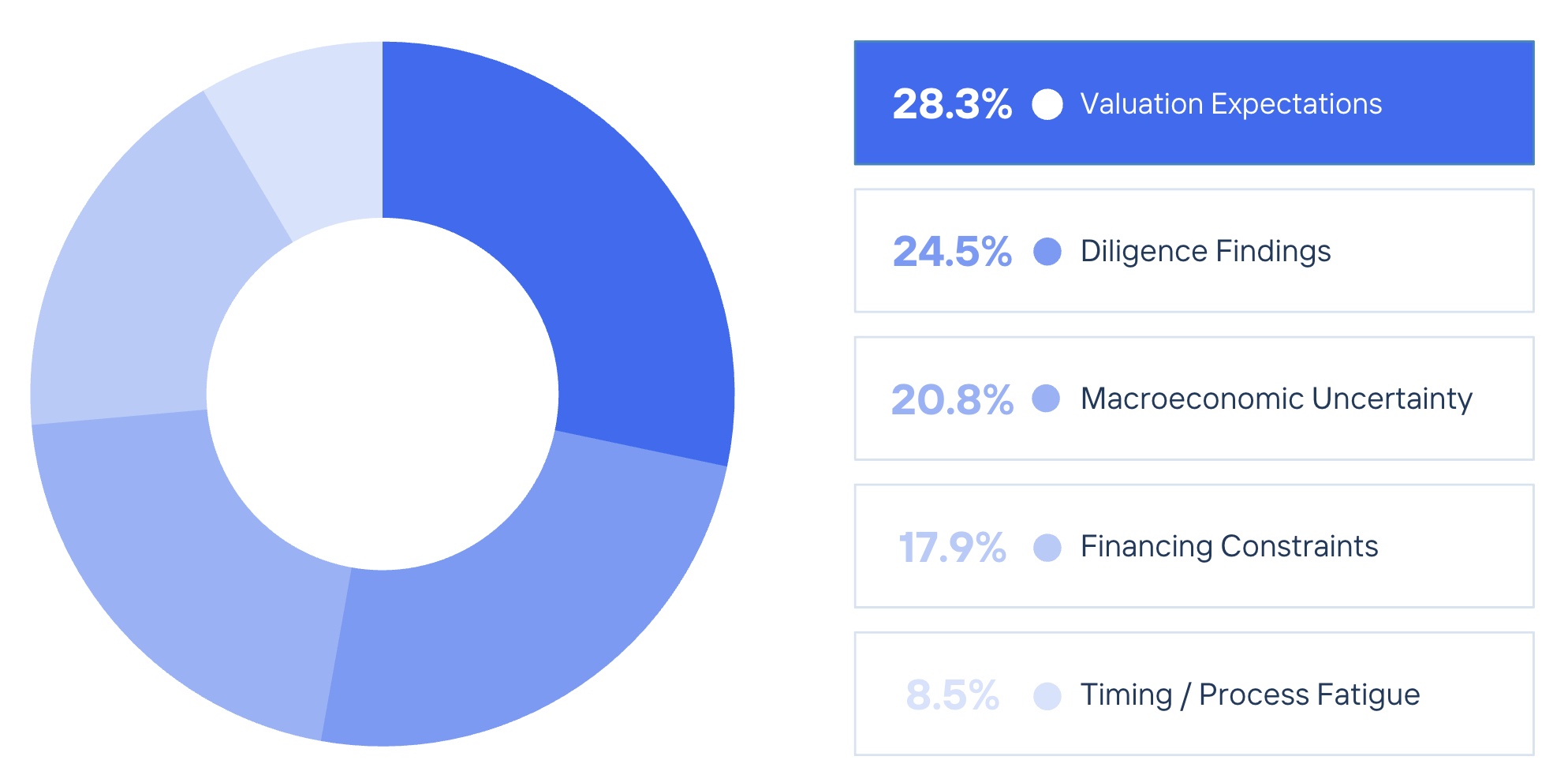

What is the single biggest reason deals failed to close in 2025?

The leading cause of deal failures in 2025 was valuation expectations, cited by 28.3% of respondents, narrowly ahead of diligence findings (24.5%). Macroeconomic uncertainty (20.8%) and financing constraints (17.9%) also played significant roles, underscoring external pressures and challenges with capital availability. These factors appear throughout the survey and are further explored in the sections that follow.

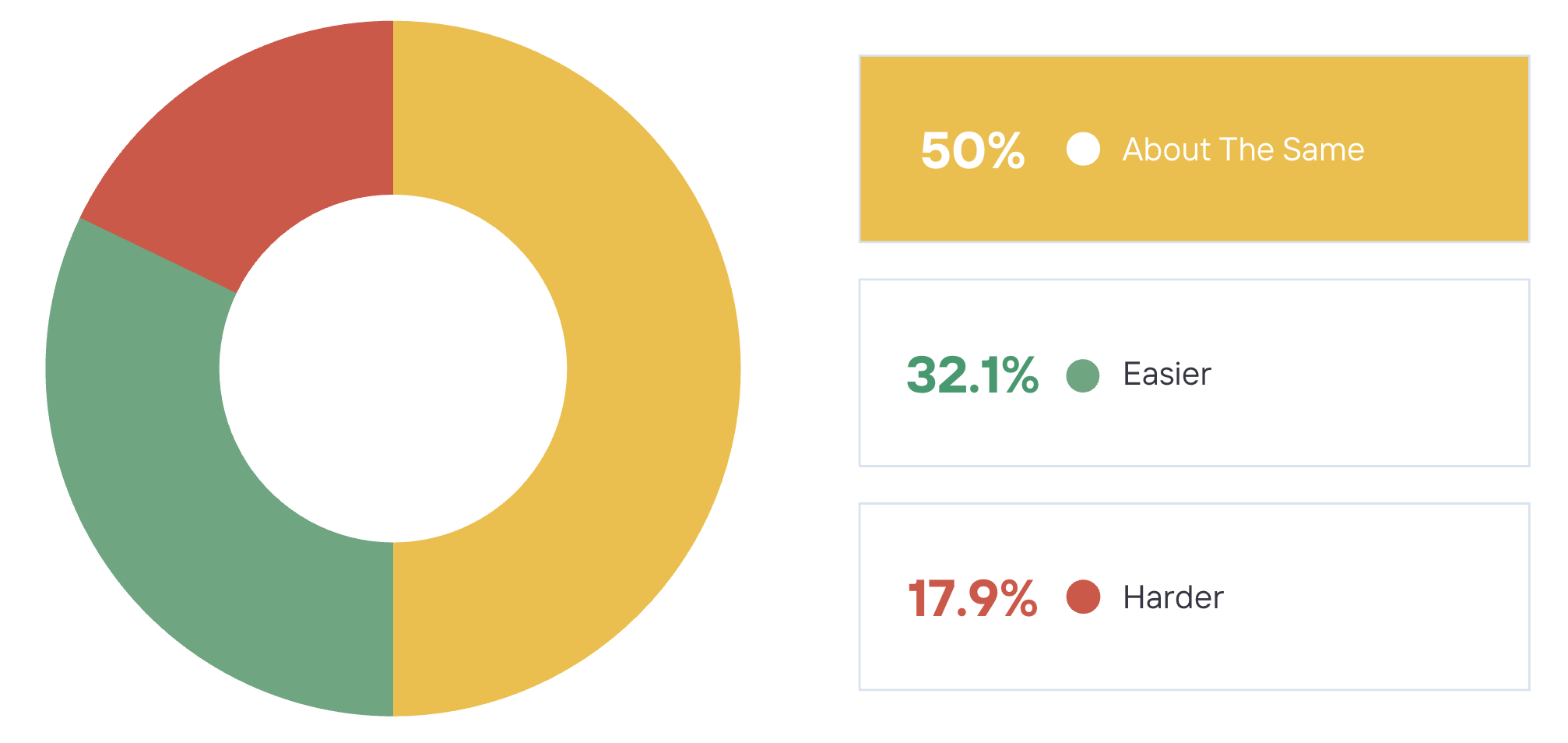

Compared to 2025, how difficult do you expect it will be to close M&A transactions in 2026?

Investor sentiment suggests a more stable deal environment heading into 2026. Half of respondents expect closing conditions to remain about the same as in 2025, while 32.1% anticipate an easier path to getting deals done. Just 17.9% expect conditions to worsen.

This marks a clear shift from mid-2025 sentiment, when 56.2% of investors reported that getting deals done had become harder, and just 6.2% experienced an easier environment.

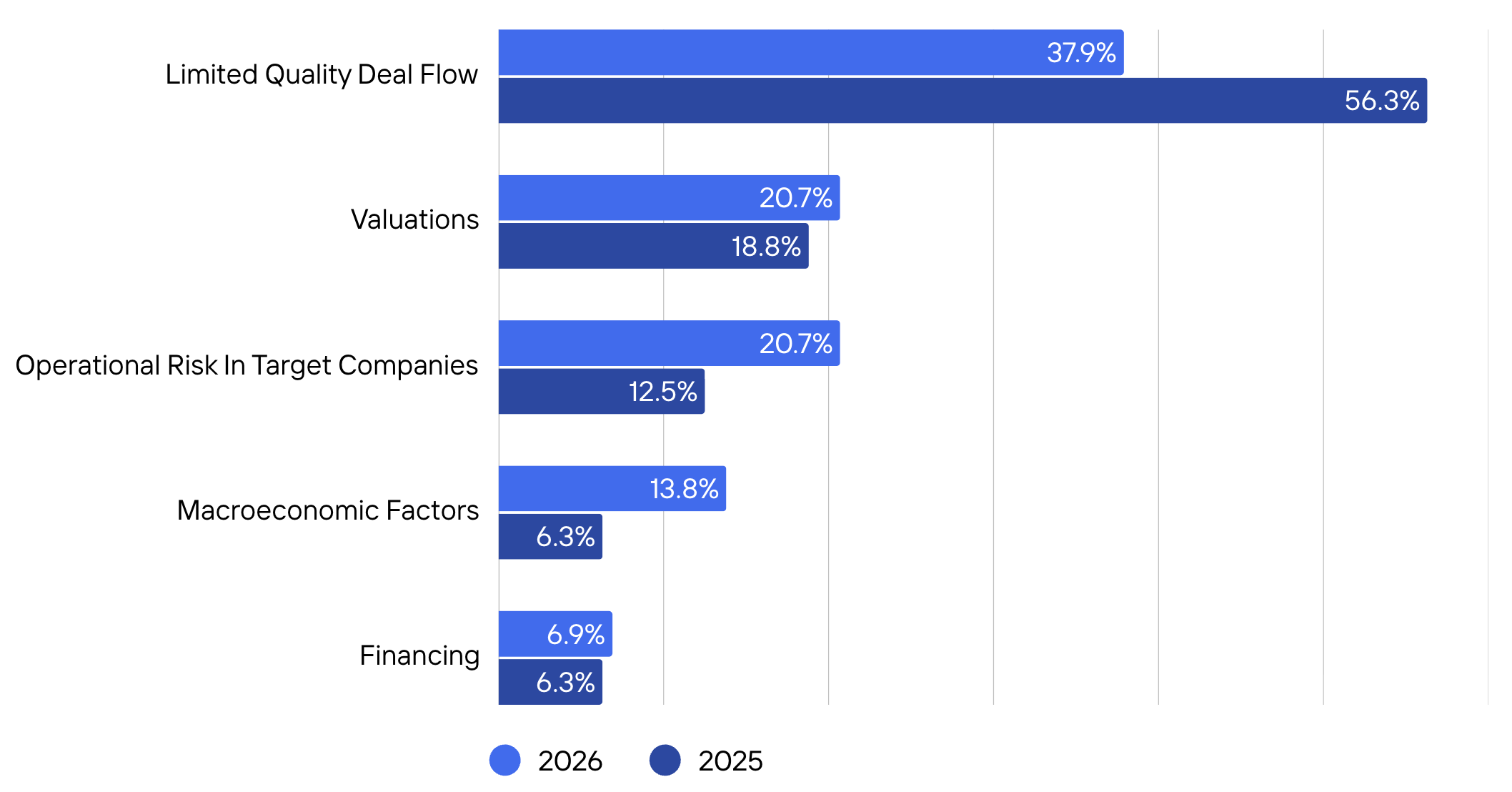

What do you anticipate the top constraint on deploying capital will be?

Limited quality deal flow continues to be the top constraint on deploying capital, cited by 37.9% of investors in 2026, though notably down from 56.3% in 2025.

At the same time, other challenges are becoming more pronounced. Concerns around operational risk (20.7%, up from 12.5%) and macroeconomic factors (13.8%, up from 6.3%) have increased, suggesting investors are shifting focus from simply finding deals to underwriting them more carefully. Valuations remain a consistent consideration, while financing constraints appear relatively stable.

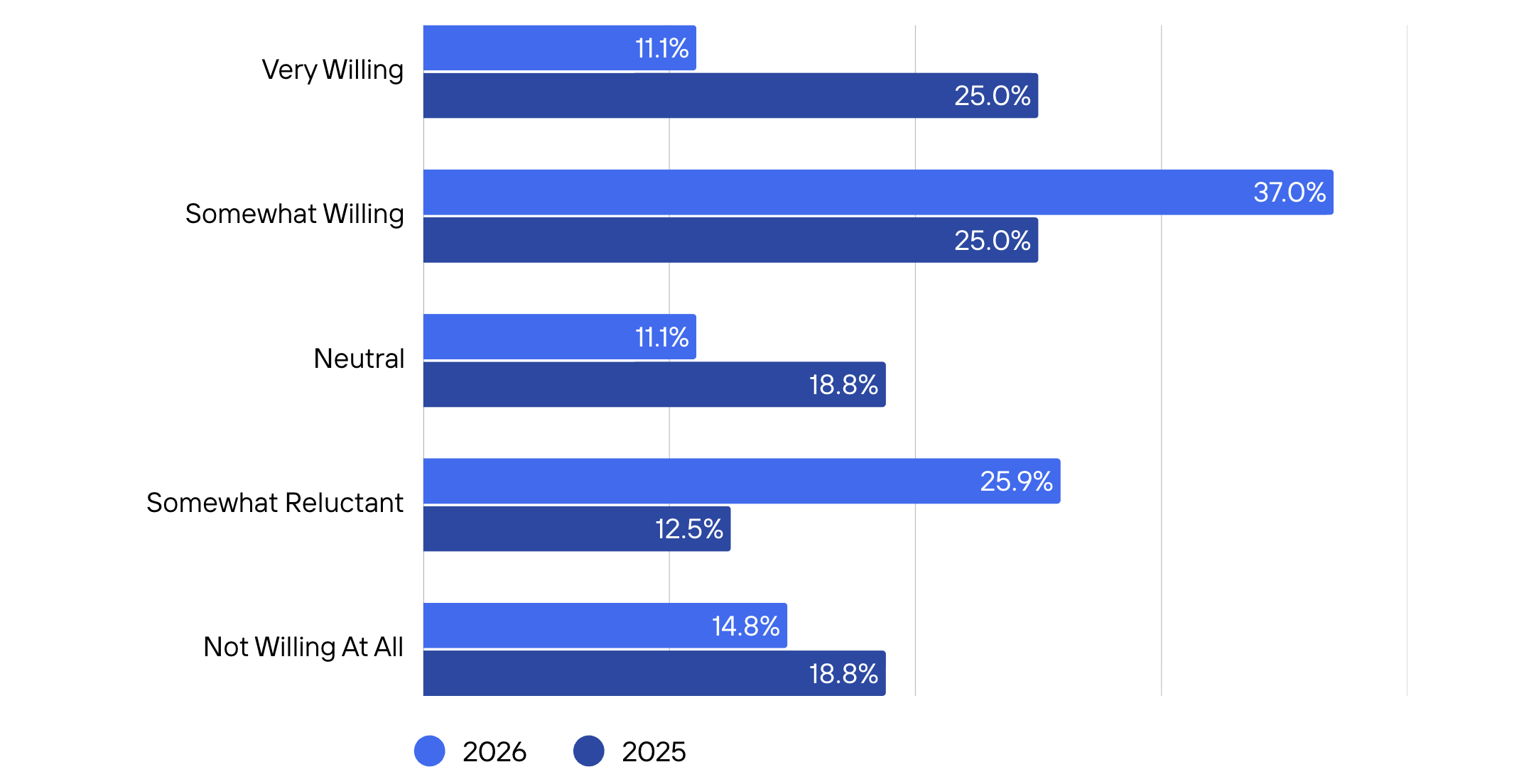

How willing are you to stretch on valuation for a high-quality asset?

Compared to mid-2025, investors appear slightly more measured in their willingness to stretch on valuation. The share of respondents who are very willing to pay up for a high-quality asset dropped to 11.1% (from 25.0%), while those somewhat willing increased to 37.0% (from 25.0%).

At the same time, reluctance has risen. 25.9% of buyers are now somewhat reluctant (up from 12.5%), signaling a shift toward more disciplined underwriting, even for high-quality opportunities.

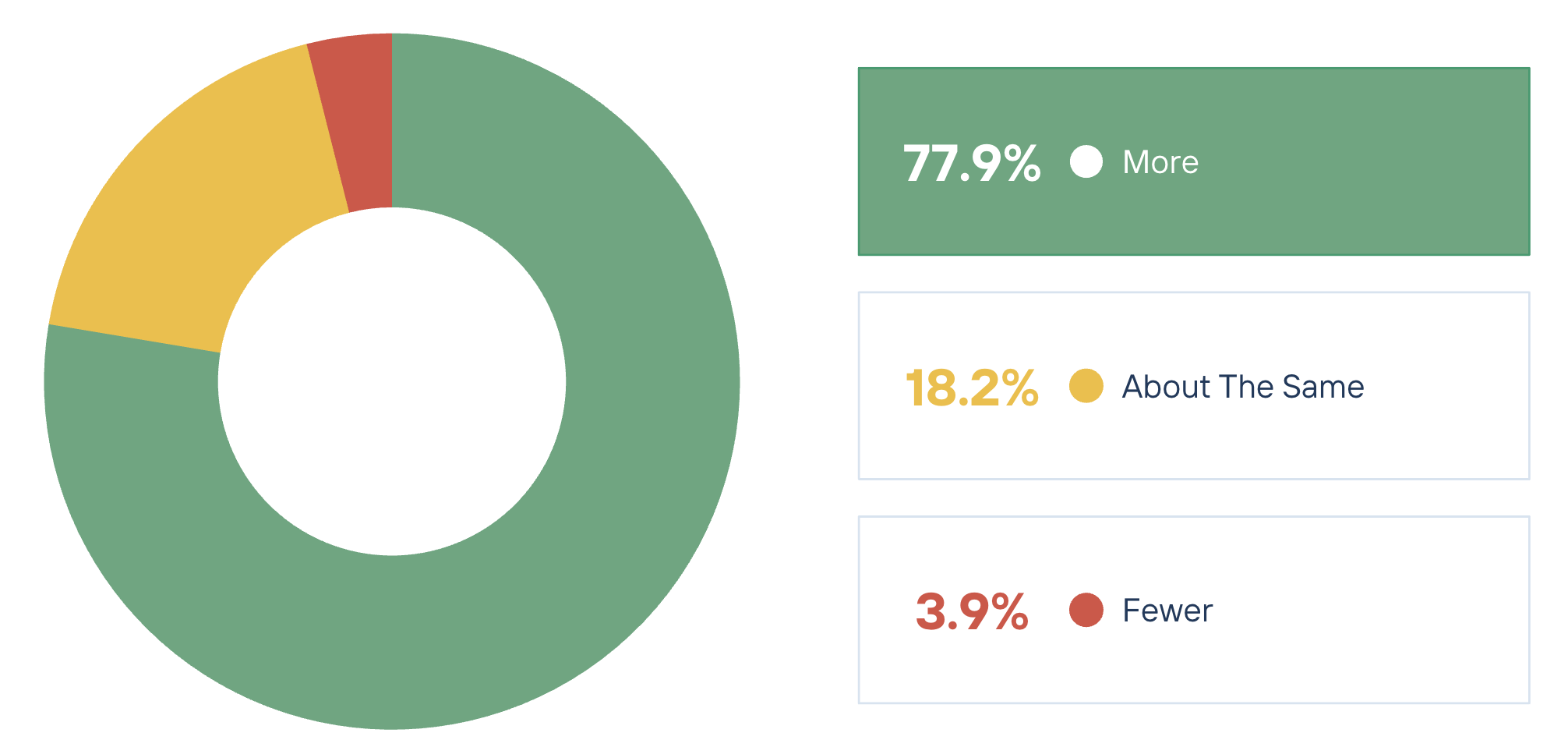

Do you expect to win more or fewer client engagements in 2026 compared to 2025?

M&A advisors are broadly optimistic about engagement activity in 2026. 77.9% expect to win more client engagements than in 2025, while just 3.9% anticipate fewer, and 18.2% expect activity to remain about the same.

Compared to mid-2025, when 57.9% of advisors expected engagement levels to remain flat and none anticipated a decline, sentiment now points to an increase in sell-side activity.

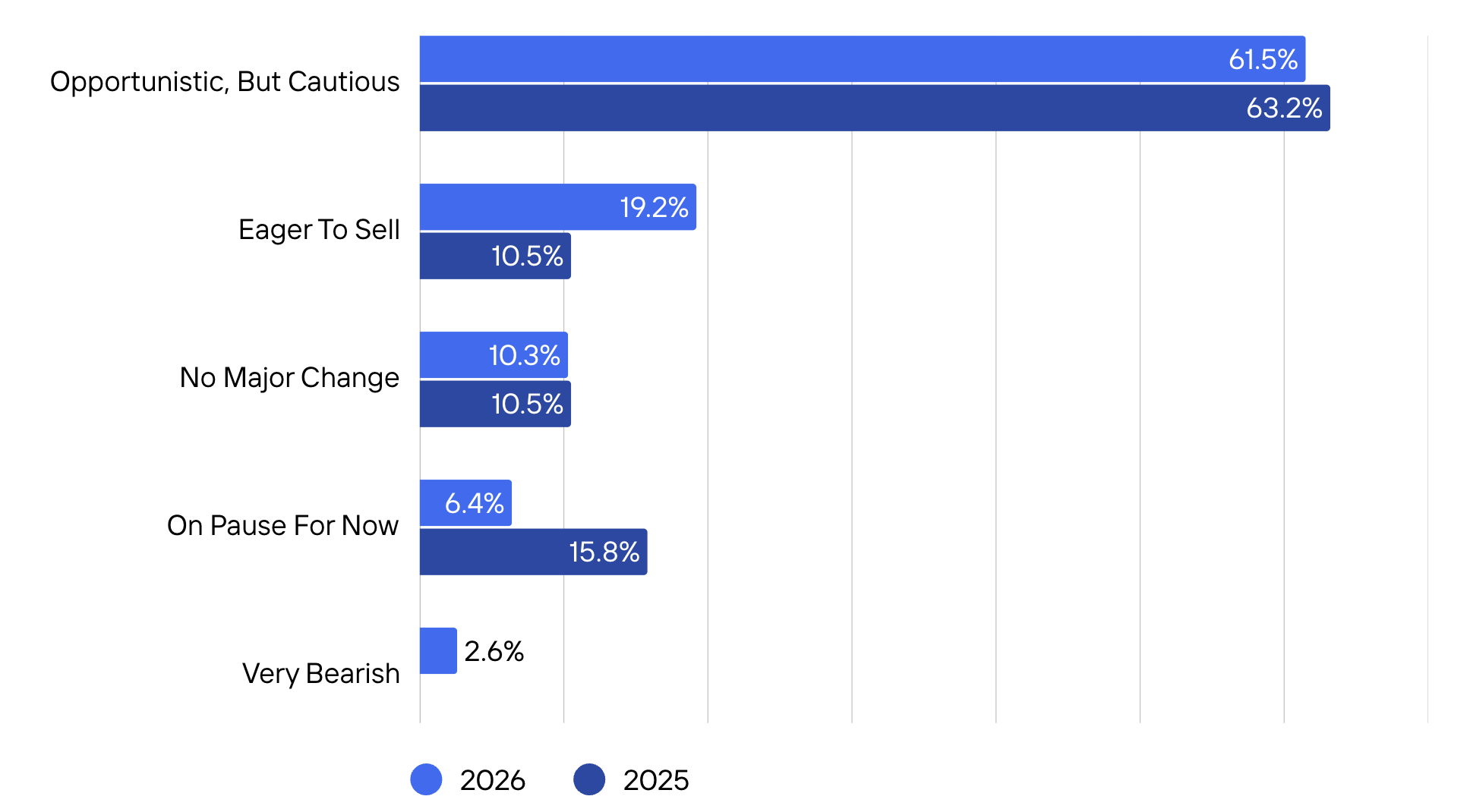

How would you describe seller sentiment right now?

Seller sentiment continues to be “opportunistic, but cautious,” cited by 61.5% of advisors in 2026, roughly in line with 63.2% in mid-2025. Notably, fewer sellers are pausing processes (6.4% vs. 15.8% in mid-2025), while the share of eager sellers has increased to 19.2% (from 10.5%).

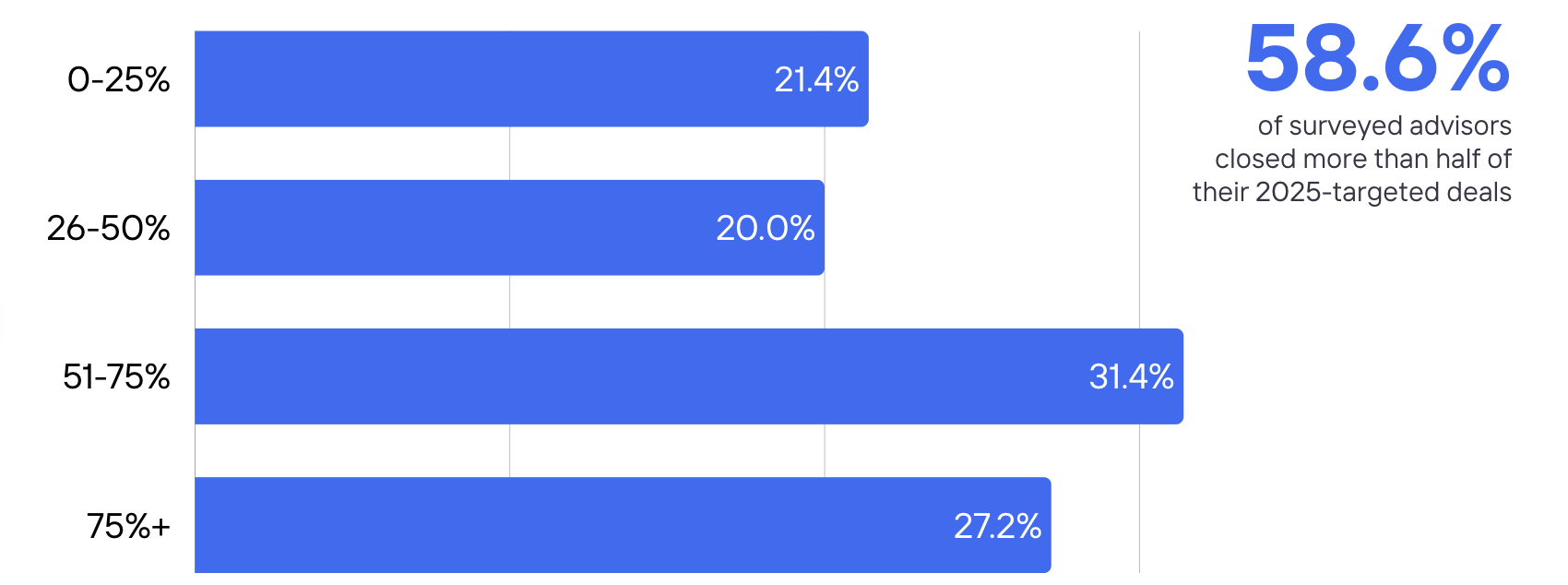

What percentage of deals with a target close date in 2025 ultimately closed?

Looking back on 2025, 58.6% of advisors reported that more than half of their deals closed, including 27.2% who closed over 75% of processes. At the same time, 41.4% reported closing half or fewer of their deals, highlighting the continued execution challenges across the market.

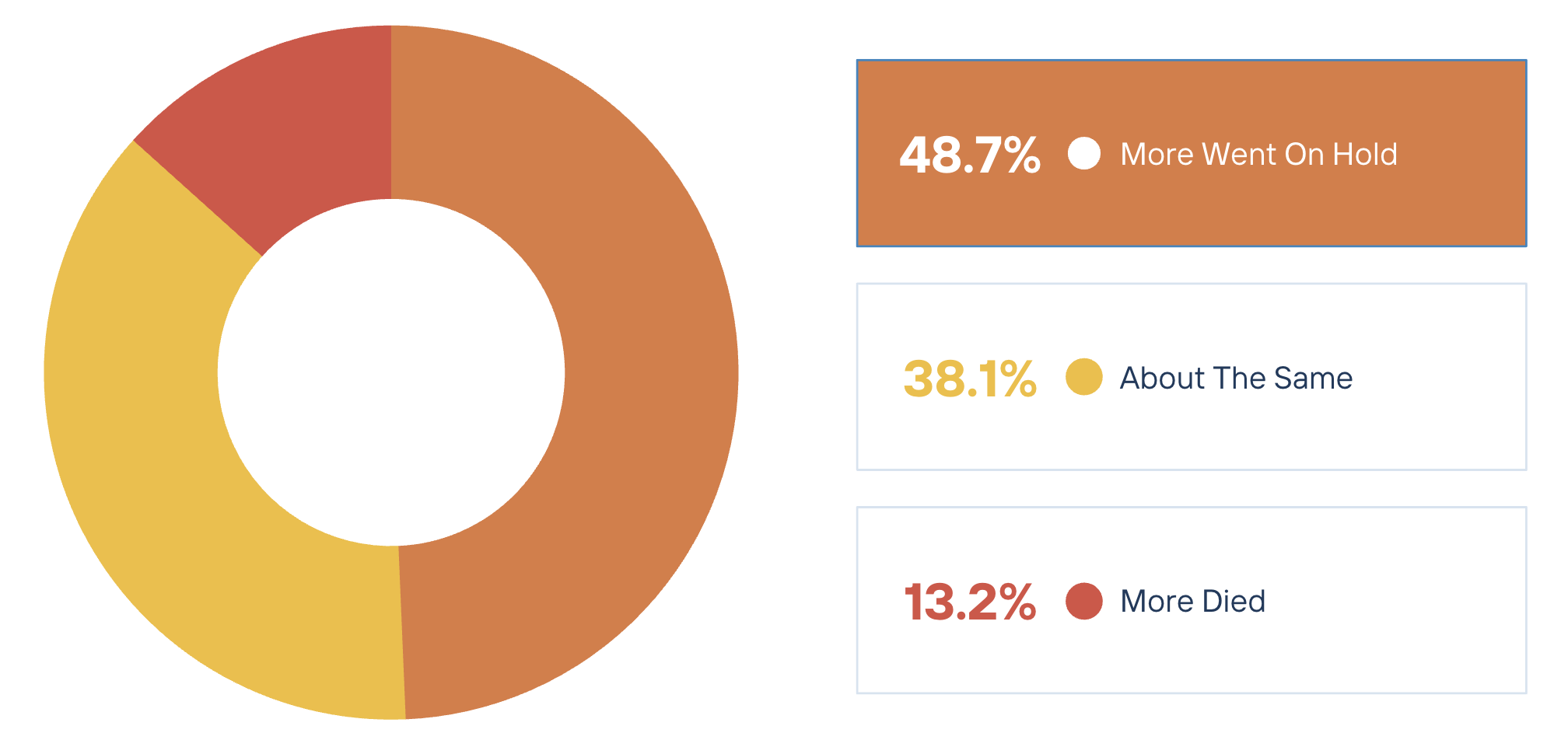

Of the deals that didn’t close as intended, did more die or go on hold?

Among deals that didn’t close as intended, advisors report that more are going on hold than dying outright. Nearly half (48.7%) indicated more deals were paused, compared to just 13.2% that saw more deals fall apart, while 38.1% reported no meaningful difference between the two.

Below, advisors share additional context on what’s driving these outcomes, with common themes including macroeconomic uncertainty, valuation misalignment, and seller readiness challenges. Many noted that deals are being paused due to financial preparedness issues or shifting expectations, rather than a lack of buyer interest, while others pointed to financing dynamics and external market conditions as contributing factors.

What are you seeing as the cause(s) of deals dying or going on hold?

| Member + Firm | Quote |

|---|---|

| Leonardo Ferreira, Hill View Partners | The macroeconomic environment, of course, has reasons for hesitation (i.e., geopolitical tensions, tariffs, labor/immigration); however, at its core, people are looking for steadier grounds to run a process while still running a business. |

| Carson Bomar, Exit Game Plan | Deals placed on hold are paused for readiness or alignment (financials not current, pre-revenue status, or seller expectation gaps), not lack of buyer interest. |

| Brian Mazar, American Fortune Mergers & Acquisitions, Inc | They are not dying, due to certain conditions, the unsold deals are taking longer to sell. |

| Cody Clemens, ASA Ventures Group | 2025 was a year defined by its uncertain start that carried into the rest of the year. It was a year when everyone was more focused on positioning amid tariffs and other strategic considerations. The volatility disrupted many industries, pausing sell-side deals, and led buyers to put new deals on hold as current portfolio companies began to underperform. |

| Oliver Bogner, The Advisory | QofE not coming back to reflect what the owner views as true adjusted EBITDA, and their not interested in a renegotiating price. |

| Michael Vann, The Vann Group, LLC | In every instance where we've had a deal put on hold or die, it's been either seller-related, circumstances beyond either party's control (i.e., change in SBA terms), or the seller's life circumstances have drastically changed. It hasn't been deal-related. |

| Trevin Rasmussen, Bristol Group | The struggle for sellers to understand valuation and set realistic expectations is causing some deals to go on hold. |

| Vipin Singh, Murphy Business Sales | General economic uncertainty, rising labor costs, frequent policy changes, seller fatigue, owner dependence, and messy financials are among the reasons deals are dying or going on hold. |

| Brandon Maddox, CRI M&A Advisors | Fairly even split between seller expectations and financing issues on the buyer side. |

| Pratik Mehta, Everyday Exits Inc. | The changing macroeconomic events have ultimately started to impact lender appetite and require alterations to deal structures. |

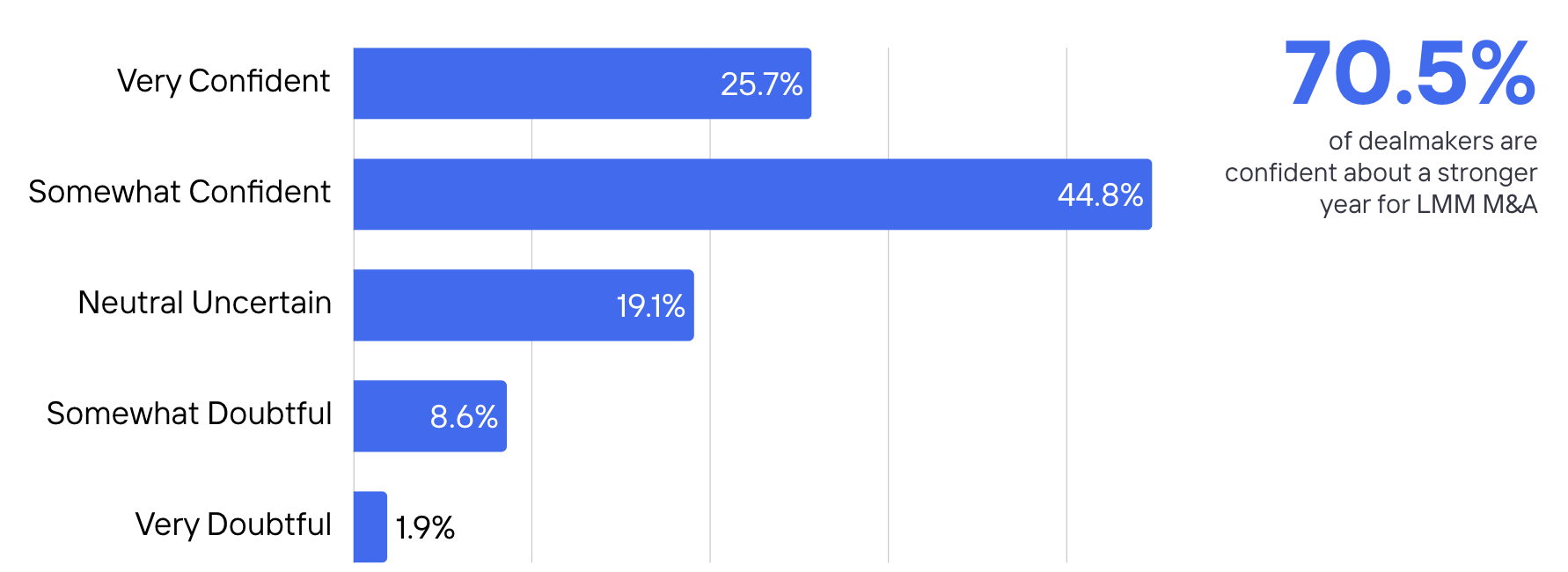

How confident are you that 2026 will be a stronger year for lower middle market M&A than 2025?

Dealmakers are largely optimistic that 2026 will outperform 2025, with 70.5% expressing confidence—including 25.7% who are very confident and 44.8% somewhat confident. Meanwhile, 19.1% remain neutral or uncertain, and just 10.5% express doubt.

The data reflects a market leaning positive, though not without reservations. Below are select quotes from the surveyed dealmakers that provide additional context for their confidence level for 2026.

| Member + Firm | Confidence Level | Quote |

|---|---|---|

| Sarah Goodman, Eminence M&A Strategies, LLC | Somewhat Confident | We're seeing a lot of seller motivation and liquidity that needs to be put to work. I think the looming threat of AI has many who experienced the .com boom and busts wary of another cycle, and whether this threat is real or not doesn't really matter. In the seller's mind, they hear a clock ticking. |

| Joe Bieshelt, The Venture North Group | Neutral / Uncertain | I would usually be optimistic, but I feel increasing uncertainty in the markets to support growth. |

| Mathew Burpee, Kepler Capital | Somewhat Confident | I believe sell-side valuation expectations have come down significantly from their 2021 highs, creating more opportunities for buyers and sellers to align on a fair price. |

| Eric Golden, Fluential Partners | Very Confident | 2025 was quite slow for M&A; this year, both buyers and sellers realize they need to move forward despite ongoing uncertainty. |

| B. Carter Looney, Legacy Founder Group | Somewhat Doubtful | There is an enormous amount of companies on the market and plenty of dry powder, but very few businesses have what it takes (QoE, transparency, owner independence, etc.) to justify the prices owners are expecting. |

| Jake Boyd, Great Plains Capital Partners | Somewhat Confident | Based on the first two months of the year, which have started off with what seems like an increase in eagerness from both buyers and sellers, I'm confident 2026 will be a better climate overall than 2025. |

| Dennis Huang, Polychrome | Neutral / Uncertain | Our focus is in software, and AI is challenging all of our old assumptions and theses. It will be much harder to take bets on anything other than stellar businesses. |

| Leonardo Ferreira, Hill View Partners | Very Confident | So long as macro-uncertainty doesn't worsen, the level of uncertainty will eventually become the norm and be factored into how businesses operate on a daily basis. If it rains every day, it isn't 'another rainy day', it's just the weather. |

| Anonymous Corporation | Somewhat Doubtful | The global geopolitical landscape, the Iran conflict, trade/tariffs, and the dollar's valuation are making every business deal extremely risky, especially U.S.-based deals involving international supply chains. |

| Thomas Ince, LP First Capital | Somewhat Confident | The rise of pooled vehicles focusing on the Independent Sponsor market, along with macro trends such as falling interest rates and the development of agentic AI, will make 2026 a hotter market for IS's than 2025. |

Taken together, dealmaker commentary points to a market supported by strong tailwinds—including ample capital availability, improving financing conditions, and a growing supply of motivated sellers—but still constrained by valuation alignment and macro uncertainty.

As Vlad Ilyusha of Light3 Capital Group puts it, “All the ingredients are there: record dry powder that’s aging out, financing conditions improving, and a huge wave of boomer-owned businesses that can’t wait forever. The back half of 2025 already felt like a gear shift, with buyer engagement picking up and processes moving faster. The question is whether buyers and sellers can get aligned on value.”

While confidence in 2026 is building, many dealmakers emphasized that pricing expectations and overall alignment between buyers and sellers will be key to translating improved sentiment into completed transactions.

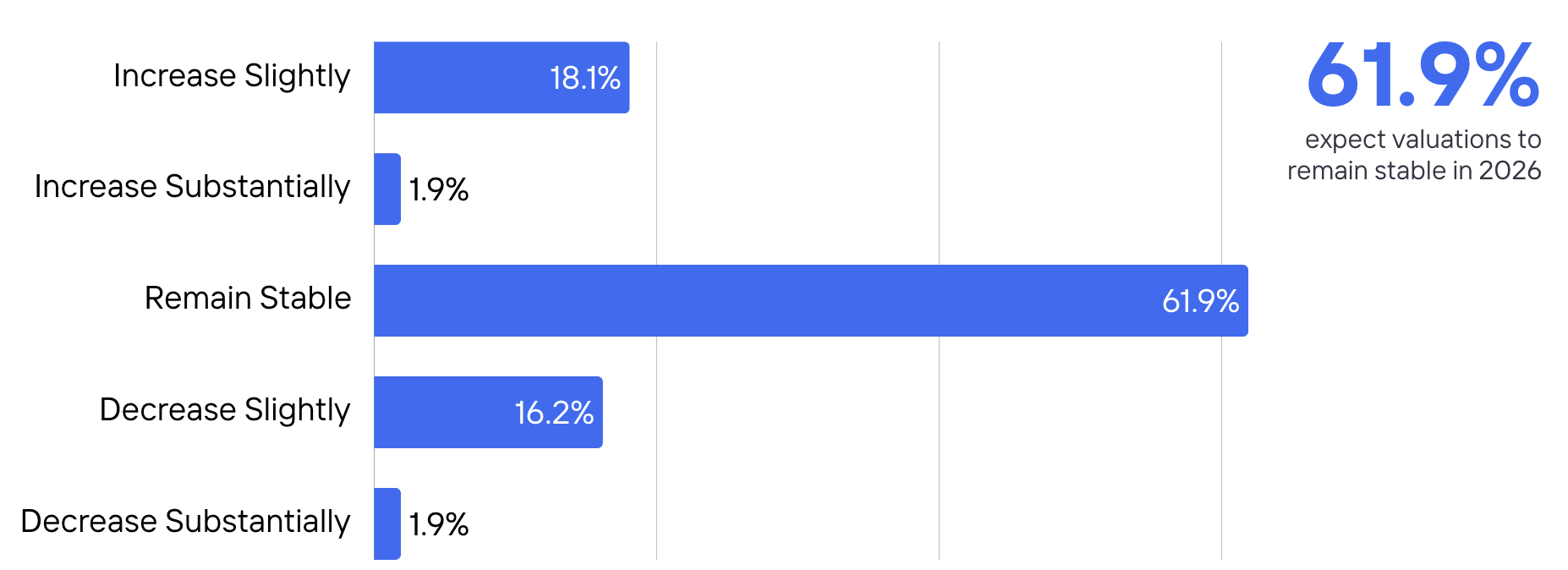

What is your expectation for valuation multiples in 2026 relative to 2025?

Most dealmakers expect valuation multiples to hold steady in 2026. A clear majority (61.9%) anticipate valuations will remain stable relative to 2025, while sentiment on directional movement is mixed—18.1% expect slight increases, and 18.1% expect slight decreases. Very few respondents expect more dramatic shifts in either direction.

The table below features commentary from a selection of respondents on what they believe will drive valuation trends in 2026.

| Member + Firm | Valuation Expectation | Quote |

|---|---|---|

| Adam Wells, Helium Capital | Remain Stable | If more companies hit the market, it'll be supply-driven, which will depress valuations (buyer's market) |

| Jake Boyd, Great Plains Capital Partners | Increase Slightly | Interest rates lowering, even slightly, always helps valuations because lenders can lend slightly more. Buyers across all different buckets are as eager as ever to find good businesses to buy. More and more buyers are actively searching than ever before. A more competitive buyer landscape, combined with slightly better rates should elicit higher multiples. |

| Ryan Mingus, TUSK Practice Sales | Remain Stable | There is still a lot of macroeconomic uncertainty, so even if the lending environment improves drastically, there is uncertainty. |

| Jeff Huenink, BlueTerra | Decrease Slightly | I think AI will change the market in many ways. |

| Hal Feder, Murphy Business | Remain Stable | Buyer demand and lack of businesses for sale inventory will underpin weaker financials ... multiples should hold steady |

| Sundeep Gill GillAgency | Remain Stable | The shift is mainly due to AI. Business owners are conducting their own search via AI to see what their businesses are worth and relying less on M&A advisors, which seems to ground them. |

| Carson Bomar, Exit Game Plan | Increase Slightly | The frequency and depth of buy/sell discussions we’re having on a daily basis are materially higher than a year ago. Historically, that level of engagement has been a leading indicator of transaction volume, which typically leads to increases in valuation. |

| Ron Buck, Murphy Business Sales | Remain Stable | Valuation multiples tend to stay consistent over time; it is the EBITDA that changes. |

| William Oates, Alliant Capital Advisors LLC | Increase Substantially | A general shift to a stronger economy in 2025 raised earnings levels. Improvements in technologies, investments in new equipment, and personnel contribute to the perception that 2025 earnings are the "new norm" or a bottom line that will be built on for the next few years. |

| Lane Carrick, Optima Mergers & Acquisitions | Remain Stable | I don't see a shift in valuations. Just a shift in seller interest. |

Dealmaker commentary reinforces the expectation of relative stability in valuation multiples, though the underlying drivers vary. Some point to increased buyer competition and improving financing conditions as supportive of pricing, while others highlight macroeconomic uncertainty, potential increases in deal supply, and evolving buyer selectivity as moderating forces.

To better understand how these dynamics are evolving, we asked dealmakers to identify the factors exerting the greatest upward and downward pressure on valuations today—and how those forces compare to mid-2025.

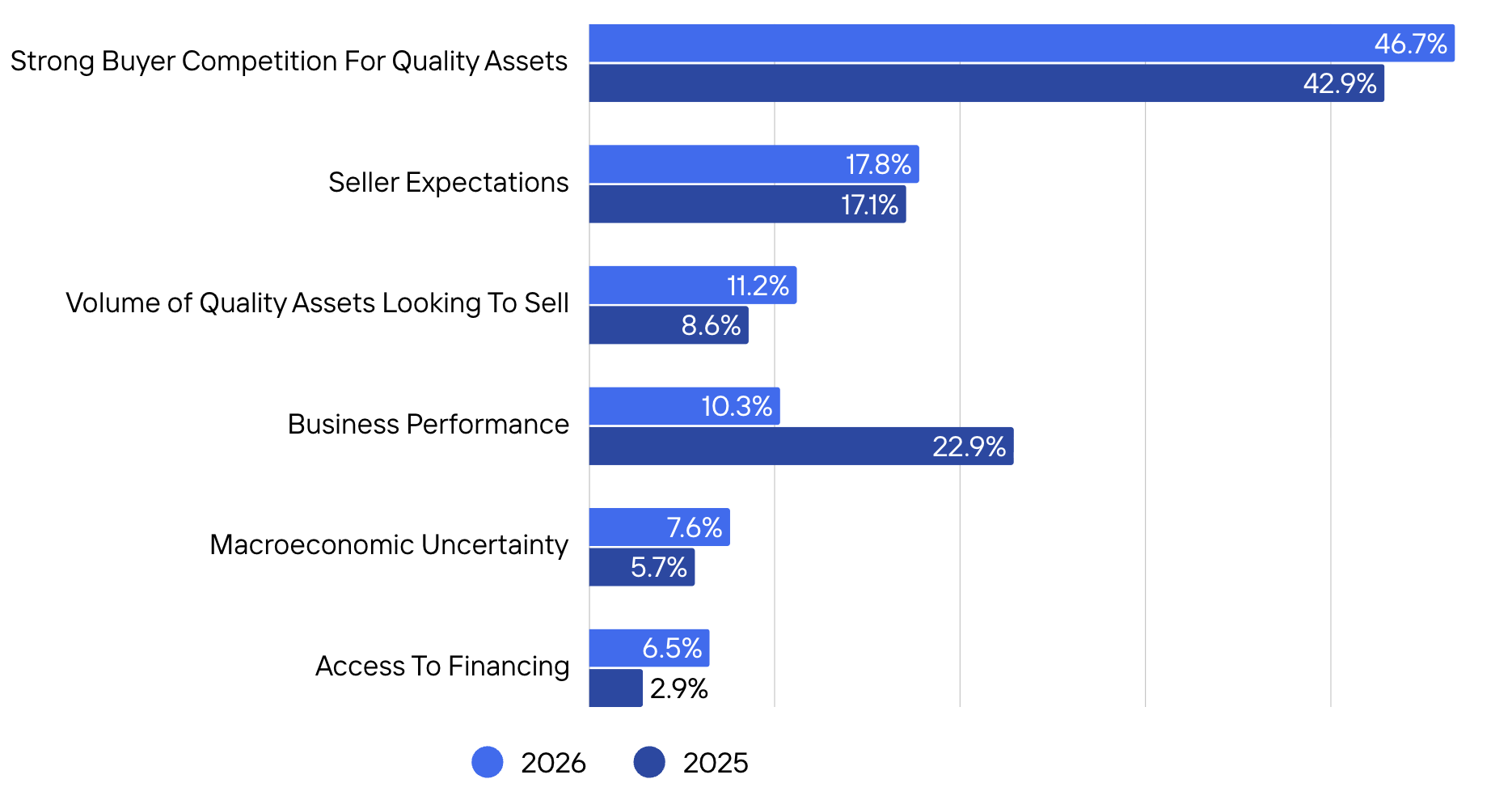

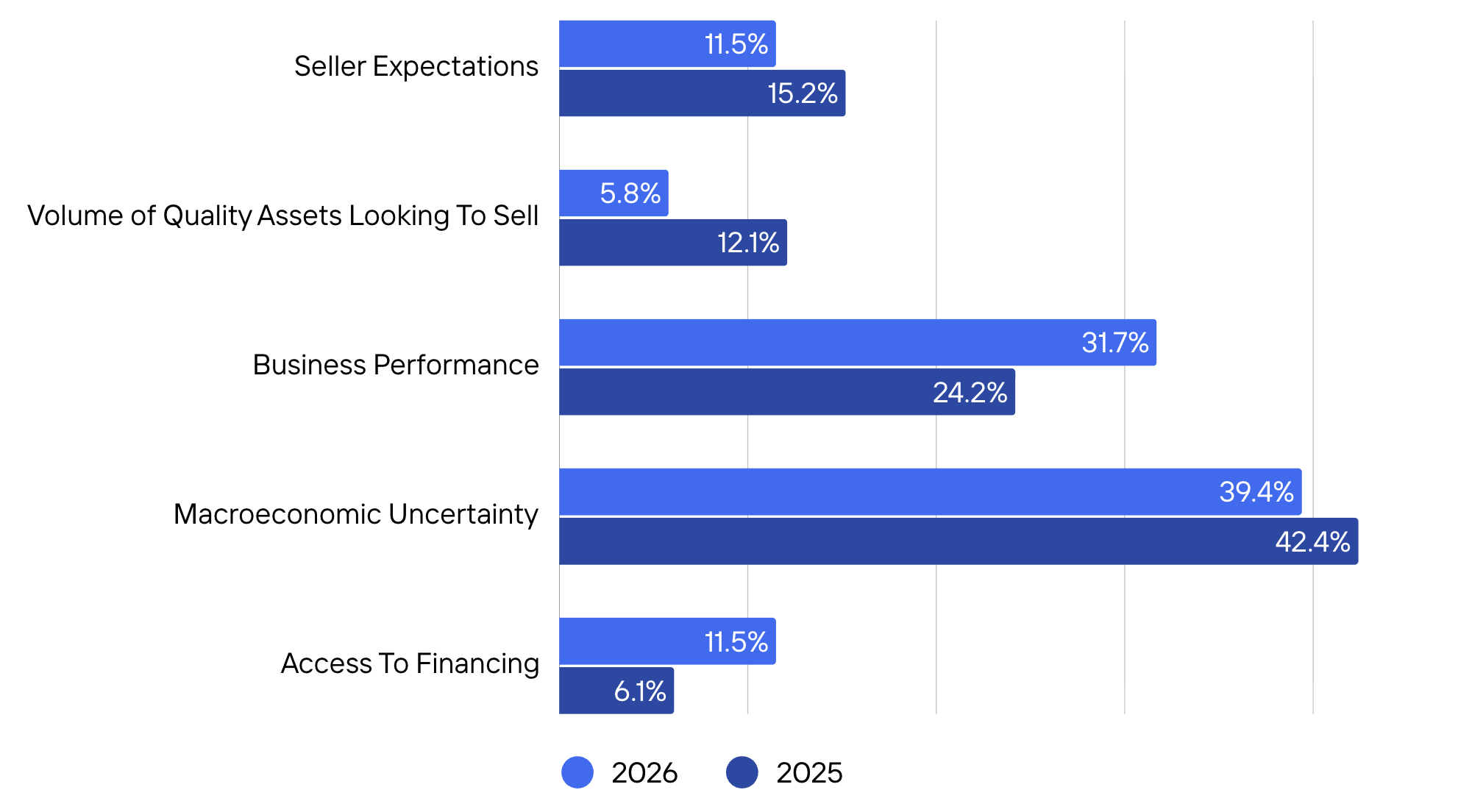

Which factor is having the greatest upward pressure on valuations right now?

Which factor is having the greatest downward pressure on valuations right now?

Surveyed Axial dealmakers point to strong buyer competition for quality assets as the primary driver of upward valuation pressure (46.7% in 2026, up from 42.9% in 2025). Meanwhile, macroeconomic uncertainty was again the most commonly cited factor applying downward pressure (39.4% vs. 42.4% in 2025), followed by business performance (31.7%, up from 24.2%). The responses suggest a market balancing optimism around high-quality opportunities with caution tied to external volatility and business performance.

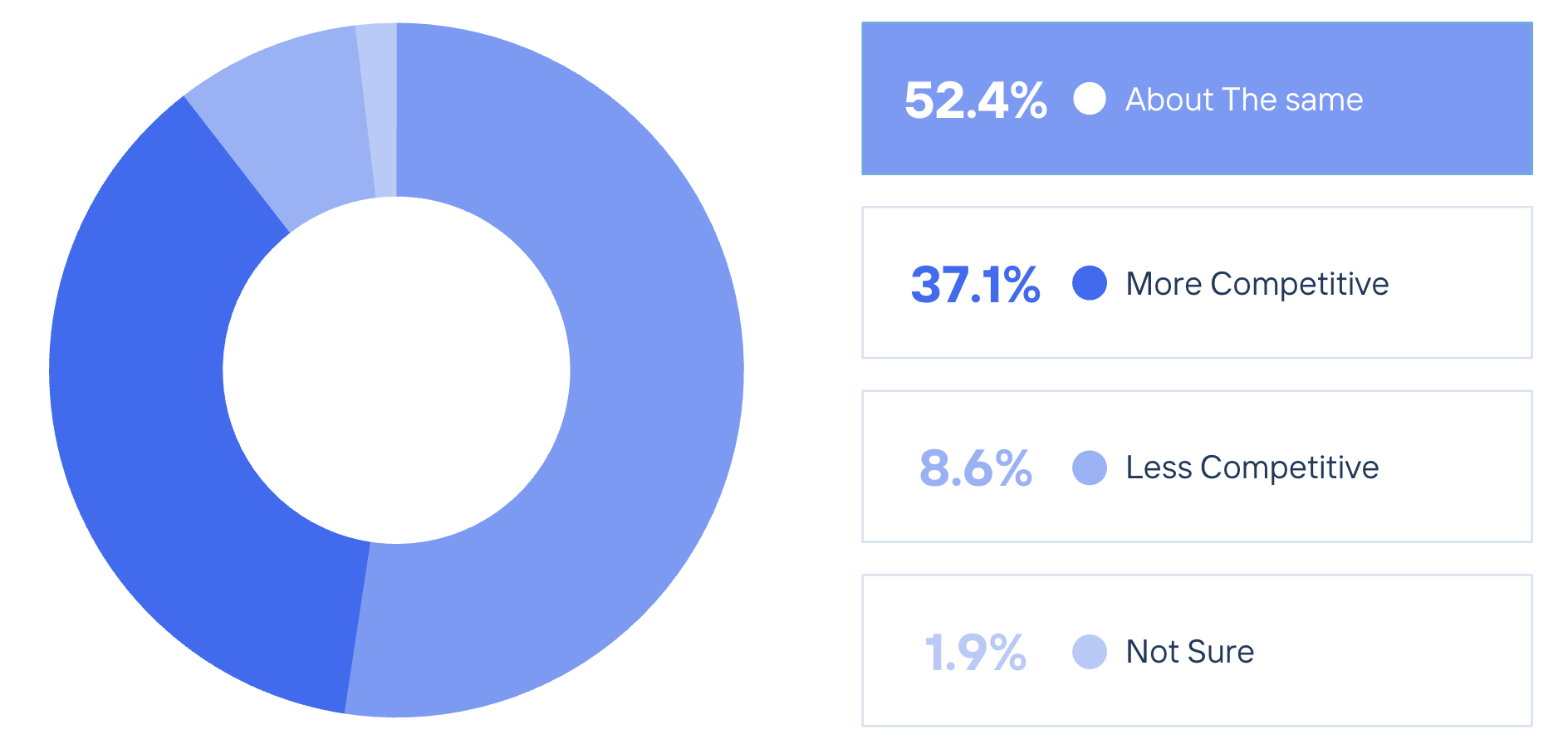

Compared to 2025, how much investor competition do you expect in deal processes in 2026?

A majority (52.4%) expect investor competition to remain about the same as in 2025, while a meaningful 37.1% anticipate a more competitive landscape, and just 8.6% expect less competition. This suggests that while competition may not intensify materially across the board, a meaningful portion of the market is preparing for increased investor interest.

Looking ahead, surveyed Axial dealmakers are closely monitoring a mix of technological disruption, shifting capital dynamics, and evolving seller behavior. Themes such as the rise of AI, increased deal supply from aging business owners, and new sources of buyer capital are expected to shape activity, while interest rates, sector-specific tailwinds, and operational efficiency gains could influence both deal flow and valuations.

Below, dealmakers share the trends they’re watching most closely as 2026 unfolds.

| Member + Firm | Quote |

|---|---|

| Justin Schaffer, JTW Advisors | The new verticals buyers are expanding into. |

| Michael Vann, The Vann Group, LLC | Artificial intelligence. Not so much the use of it, but the rise of the AI-first advisors. For relationship-based businesses, it usually doesn't end well when technology is the product rather than the tool. |

| Paul W. Harrison, Emerald Coast Luxury Transportation LLC | Watch more closely for deal-size preferences and capital availability to help sellers improve their value in the short term, if needed to meet valuation expectations. |

| Charles MacPherson, Inbar Group, Inc. | Interest rates. Lower interest rates make marginally profitable companies more profitable, easing cash flow pressure. |

| Robert Aldana, Bayshore Acquisitions | I’m watching how broadband funding (BEAD and related programs) translates into actual construction work and contractor capacity. Many telecom contractors expanded during the funding announcement phase, and 2026 will reveal which companies have the systems, crews, and capital to execute at scale. |

| Thomas Ince, LP First Capital | Agentic AI will be a major disruptor to many industries. This will present both challenges and great opportunities. |

| Kevin Coleman, Cape Redan Capital | We are cautiously optimistic that founders/owners of growth businesses will have constructive valuation expectations for the right partner/acquirer. |

| Vlad Ilyusha, Light3 Capital Group | The baby boomer exit wave is real and accelerating. Every year, more owners in their late 60s and 70s simply can't wait for a "better" market. That's going to steadily increase deal supply, whether conditions are perfect or not. The advisors who are out in front, building relationships with these owners now, will have a massive pipeline advantage. |

| B. Carter Looney, Legacy Founder Group | Looking at the EtA movement and its access to equity for their deals. This could make a significant difference in easing downside price pressure. |

| Reggie Young, Exit Advisor | Investor pooling—through searcher syndicates, independent sponsor capital stacks, and small private investor groups—will become more common as buyers spread risk and increase purchasing power. |

| Dennis Huang, Polychrome | AI continues to be a huge trend, and seeing how it continues to change the software landscape. I think 2026 is going to be a tremendously rocky year. |

| Edwin Gehres, Navvee | I'm watching how well businesses are leveraging technology trends and streamlining efficiencies to maximize profits. The tools available now can already dramatically increase efficiency, especially for smaller companies. |

Across the data and dealmaker commentary, a consistent picture emerges: capital is ready, sellers are increasingly motivated, and activity is picking up. But execution will continue to depend on discipline, particularly around valuation expectations, underwriting rigor, and navigating macro uncertainty.

Those who can bridge the gap between opportunity and alignment may be well positioned to benefit from a more active—and potentially more productive—2026.