The Top 50 Lower Middle Market Industrials Investors & M&A Advisors [2026]

Industrials remains the dominant sector on Axial, accounting for 27% of all deals brought to market via the platform last…

A historically “in-person-only” industry, education has become available for consumption through a wide variety of mediums. The way we learn and obtain information is evolving at a rapid pace.

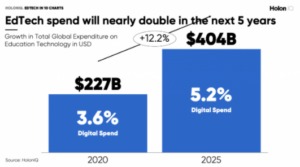

The disruption caused by COVID-19 has made EdTech – broadly defined as the incorporation of technology into education – a particularly attractive investment for private equity buyers. Even when the pandemic is in the rear-view mirror, we should continue to see major investment and innovation in the space. In fact, digital spending in education is forecast to grow from $227B in 2020 to $404B by 2025, according to Holon IQ, an education industry market intelligence platform.

The disruption caused by COVID-19 has made EdTech – broadly defined as the incorporation of technology into education – a particularly attractive investment for private equity buyers. Even when the pandemic is in the rear-view mirror, we should continue to see major investment and innovation in the space. In fact, digital spending in education is forecast to grow from $227B in 2020 to $404B by 2025, according to Holon IQ, an education industry market intelligence platform.

What are the factors driving the significant increase in digital education spend?

Growth Beyond the Pandemic

We do not expect enthusiasm for EdTech to end with the COVID-19 pandemic.

In many ways, COVID-19 merely exposed flaws in the industry. Socioeconomic disparities in education, for example, will continue to be a major problem, and digital infrastructure will play a role in solving it.

The Case for Investment in EdTech

Valuation in EdTech is wide-ranging. Chegg, a publicly traded learning platform, trades for around 22x revenue. We have seen smaller private-market deals trading at 3-10x annual recurring revenue for growing, niche companies with strong business models and strategic alignment for larger platforms.

Growth is not the only factor in valuation. Contractual nature, pricing stability, and customer churn are all fundamental elements of the valuation and attractiveness of EdTech companies. Non-recurring business models might garner a valuation based on a profitability metric like EV/EBITDA, especially if it is maturing and dependent on tech-enabled services or one-time purchases of products or services.

Synergies

We will continue to see strategic buyers looking to add complementary products and services via acquisition. Understandably, they want to gain wallet share of segments they already serve, as well as increase the platform’s total addressable markets.

In a high-growth industry, growing total addressable market (TAM) and market share is critical. In a recent instance, Copper Run Capital helped a PE-backed EdTech company find and acquire a complementary business that added new capabilities in overlapping end markets. These are the types of synergies that are proving attractive in today’s landscape.

From virtual tools used to teach toddlers to read, to language-learning programs for world travelers, EdTech’s reach is broad and growing. There are new applications and use cases coming to market on an almost daily basis.

There has never been a more exciting time to be involved in the EdTech space. It has become clear that the accelerated growth catalyzed by Covid-19 is here to stay.

Michael Shaw is a Partner and Managing Director at Copper Run. He specializes in private equity buy-side advisory.