How Coronavirus Is Impacting Lower Middle Market M&A Activity

Last week, Axial convened a virtual roundtable of members to review the impact of the coronavirus pandemic on lower middle…

The following may sound surprising, but rarely do lenders or private equity firms think about how much capital is actually spent toward deal sourcing, and what the quantifiable results are from those efforts. They know they want more deals, but don’t think about the deal sourcing process in a very cost-effective way.

Before diving into more detail, let’s first define what capital spend on deal sourcing actually means.

Capital spend on deal sourcing includes any expense toward the effort of finding more deals. That not only includes expenses toward marketing, websites, hotel booking, air travel, dinners, sponsorships, and trade shows, but more importantly, on those professionals responsible for sourcing. The latter ends up costing the most.

If a firm is lucky enough to have a dedicated business development person, it’s easy to quantify the majority of the overall deal sourcing cost via their salary. For firms without a dedicated business development function, the question becomes, how much of each individual’s time at the firm is spent on deal sourcing (Associates, VPs, Principals, MDs), and how can we quantify that? If, for example, 15% – 20% of each person’s time is dedicated to sourcing activities, that essentially translates to 15% – 20% of their salary being allocated toward that effort.

With that measurement and thought process in mind, a typical firm could end up spending a total of $450K to $1M per year on business development.

When I present that analysis to private equity firms and lenders, I will simply ask, “Based on that analysis, is it fair to say that that the firm spent $450k to $1M last year in order to see 200, 300, 400, or 500 deals?” Interestingly enough, the typical response I get is, “Well, I have never thought it about that way, but yes, that’s fair to say.”

This response is both surprising on the one hand and not surprising on the other.

On the one hand, it’s surprising because if a firm is so rigorous when it comes to the efficiency, profitability, and growth of the firms they are investing in, why not treat their own firm’s business development efforts in the same manner? According to Andrew Cialino, Head of Business Development at Axial, “Immediately upon acquiring a business, a private equity firm will oftentimes make significant changes to a portfolio company’s sales organization to drive higher revenues at lower costs. Shouldn’t a similar philosophy apply internally? To survive in today’s competitive market, private equity firms must transfer their operational rigor to their own sourcing efforts. That focus should lead to function specialization, measurement of inputs (not just outputs), and consistent iteration in strategy.”

On the other hand, it’s not very surprising because firms think about deal sourcing as very binary, focusing their energy on driving returns, doing anything they can to close a relevant deal, rather than focusing on the capital spent to do so. (Lenders typically have business development officers, and therefore tend to be a bit more scientific about the process.)

Regardless, once you’ve figured out the amount of money your firm is actually spending on sourcing, the key is to figure out ways to maximize that spend, not to detract from it.

So, are there ways to incrementally enhance the top of your deal funnel without breaking the bank?

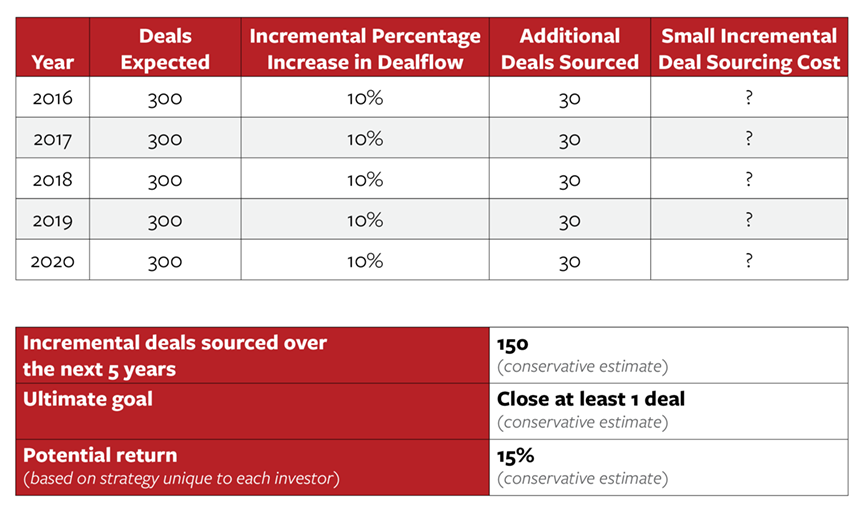

If, for example, a firm saw 300 deals last year, looking to increase deal flow by a mere 10% would mean seeing another 30 deals per year, enhancing the probability of signing one more LOI, and potentially generating another 12%-30% returns (depending on the returns a firm seeks to generate). That’s a non-insignificant amount that deserves a non-insignificant strategy.

Surprisingly, many middle market firms take a very short-term view of market coverage, mainly reevaluating coverage one year at a time. They know what’s worked last year and the year before that, so they expect to see a certain number of deals the next year and make at least one or two investments.

The question is, why are they focusing on just the next year? What about coverage over the next five years? For example, if a firm that typically sees 300 deals a year can increase their coverage 10% per year, that’s another 150 potential deals. With increased competition, along with continued proliferation of sponsors and lenders, this long-term thinking could very well be a key factor to setting your firm apart, especially since most funds have a required timeline of 5-7 years in which to deploy their capital.

I don’t know why that long-term view is not prevalent, but I do know that out of all the alternatives out there in the marketplace today, I have not found a better, more cost-effective solution other than technology. Just as robo advisors are transforming the public markets, so too are networking and sourcing platforms changing the private capital markets. It’s the tech-enabled solutions that are helping firms enable widespread coverage with relatively little human and financial capital.

I see lots of private capital market professionals who have a difficult time reconciling technology with relationship building. It’s understandable, as the industry has worked the same way for generations. Having said that, those who are not open to learning more about technology trends, could very well be left behind.

To be very clear, technology is not there to replace a firm’s current relationships, nor will it ever be equal to the quality of a firm’s current network. Rather, it is there to initiate new relationships, ultimately capturing a differentiated deal you would have never otherwise seen.