Lower Middle Market 2H Outlook: Valuations, Deal Activity & Market Trends (Part 1)

Part 1 of Axial’s 2H 2026 M&A Outlook Series Axial members entered 2026 with cautious optimism about a more stable…

The average private equity firm sees less than one-fifth of the deals that actually fit their mandate. More than 80% of relevant opportunities are never even surfaced to them, lost in a fragmented network of boutique banks and brokers.

Deal sourcing in the lower middle market is therefore one of the hardest jobs in private equity. The market is vast, the participants are fragmented, and even the strongest sourcing efforts can’t consistently deliver comprehensive coverage.

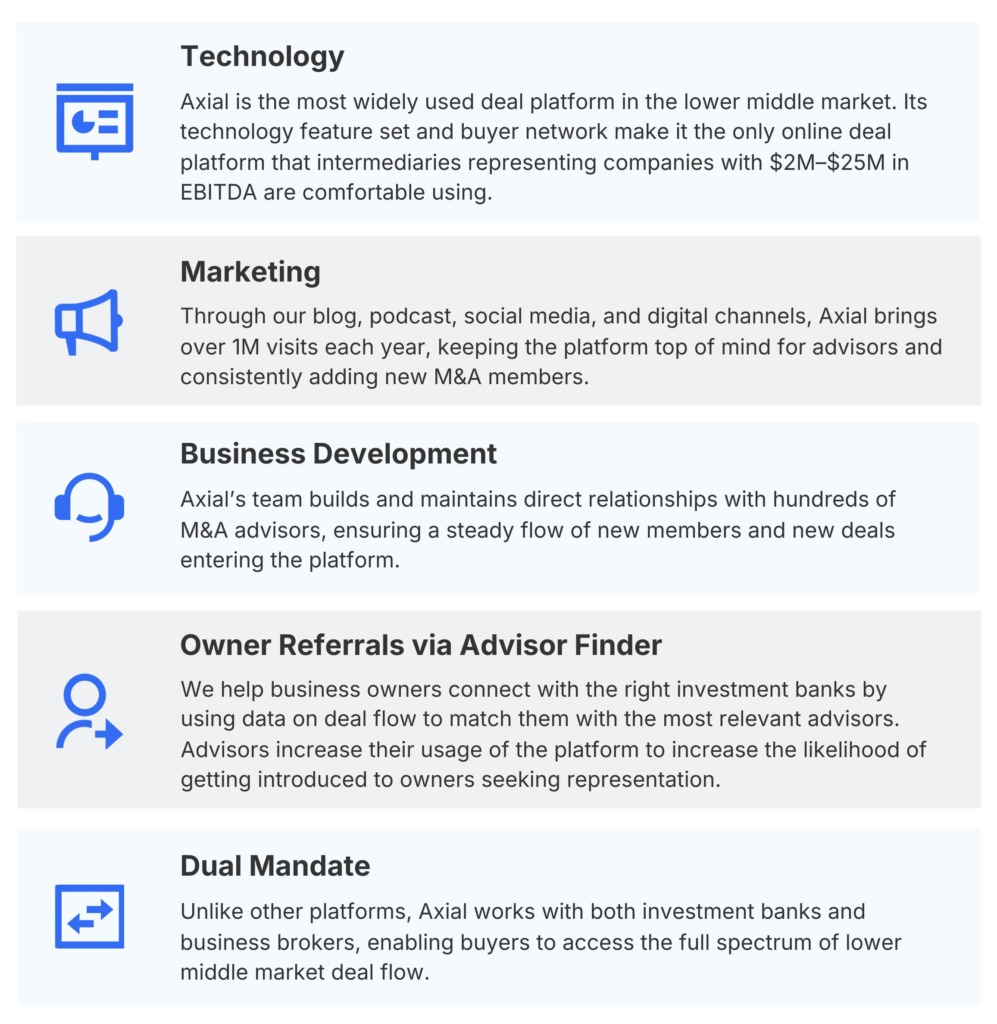

Axial was built to close this gap. By combining technology, data, and human coverage, the platform expands deal flow sourcing within the advisor-represented channel, surfacing opportunities from lesser-known firms that PE firms might otherwise miss. For funds looking to increase their odds of finding great opportunities at great prices — whether platforms or add-ons — Axial provides a systematic way to do so efficiently and economically.

Below is a snapshot from Sutton Place Strategies’ annual Private Equity Deal Origination Benchmarking report, where they survey hundreds of PE firms to gather data about their deal sourcing coverage.

The most active private equity firms are only sourcing a small portion of relevant opportunities available in the market. According to the Report, the median PE firm covers just 17.6% of its relevant deal flow. Even firms in the top quartile only reach 27.5%, and at the very best, market leaders max out around 57.1%.

Leading PE firms build their sourcing strategies around three core channels:

| Market Size | Median Coverage | Maximum Coverage | Solution | |

| Middle Market Investment Banks | ~500 | 20.4% | 63.5% | Relationships + Axial |

| Boutique Lower Middle Market Advisors | ~5,000 - 10,000 | 11.8% | 64.1% | Axial |

| Direct-to-Company (Proprietary) | ~250,000 | – | – | Data Providers & Marketing Tools |

There are a host of structural reasons why PE firms on average cover less than 20% of relevant deal flow coming from boutique lower middle market advisory firms:

Axial has one primary promise to private equity investors on its platform: maximize coverage of relevant deal flow coming from lower middle market boutique investment banks and business brokers.

| Coverage | Active Advisors | Annual Deal Flow | Location | Revenue Range | EBITDA Range |

| ~50% of LMM advisors | 2,500+ | 11,000+ | US & Canada | $3M - $250M | $500K - $25M |

Axial extends its private equity members’ marketing, business development, and technology teams, helping investors source high-quality deal opportunities without adding headcount or inflating BD budgets.

–

While Axial’s membership includes PE funds of all sizes, firms do execute different strategies depending on their size:

These are the largest players in the industry. They typically pursue upper middle market and large-cap deals, focusing on transactions that can absorb significant amounts of capital.

How they use Axial: Primarily for add-on acquisitions, where smaller targets can be folded into existing platforms.

Mid-sized funds pursue a range of deal sizes and often straddle both middle and lower middle market opportunities.

How they use Axial: Mostly for add-ons, while remaining opportunistic for platforms that fit their investment criteria.

Smaller funds, often early in their fund generations, typically focus more heavily on founder-owned and lower middle market businesses.

How they use Axial: Both for add-ons and platforms, as Axial’s coverage aligns directly with the asset sizes and strategies they pursue.

| Platform Deal Size Targets (EBITDA) | Add-On Deal Size Targets (EBITDA) | Platform Sourcing on Axial? | Add-On Sourcing via Axial? | |

| 10 Figure Funds | $20M - $50M | $1M - $20M |

|

|

| 9 Figure Funds | $10M - $20M | $1M - $10M |

|

|

| 8 Figure Funds | $3M - $10M | $1M - $5M |

|

|

–

The Sterling Group Expanded Portfolio Company Russell Landscape with Acquisition of Georgia Green

The Sterling Group Expanded Portfolio Company Russell Landscape with Acquisition of Georgia GreenIn December 2024, The Sterling Group, a Houston-based private equity firm managing a ten-figure fund, acquired Georgia Green, a Georgia-based commercial landscaping company, through its portfolio company Russell Landscape Group. The acquisition strengthened Russell’s regional presence and operational scale across the Southeast, aligning with Sterling’s focus on investing in and growing industrial service businesses through strategic platform expansion.

Georgia Green was represented by John Marsh of Marsh Creek Advisors, an Axial sell-side member since 2020. The Sterling Group, an Axial member since 2010, pursued the deal on September 10th, 2024. The LOI was executed on November 9th, following a 60-day evaluation period, with the transaction successfully closing just 41 days later, on December 20, 2024.

Sleeping Giant Capital, an eight-figure PE fund and Axial buyside member since 2021, acquired Rep-Lite, a provider of outsourced commercial and service personnel to life sciences companies, as the first investment in its Human Capital platform.

Woodbridge, an Axial sell-side member since 2010, advised Rep-Lite on the transaction. The company delivers scalable, compliant staffing solutions to medical device, pharmaceutical, and biotech clients, offering an efficient alternative to traditional hiring models.

Sleeping Giant was able to leverage Axial to support its thesis of acquiring operationally resilient, people-centric businesses, identifying Rep-Lite as a strong platform fit. The LOI was executed on November 5, 2024, with Sleeping Giant successfully closing its first Axial-sourced deal 167 days later, on April 21, 2025.

–

Blackstone, a global private equity firm with over 100 portfolio companies, sourced the acquisition of an $18M EBITDA specialty financing provider through an unlikely channel: a Milwaukee-based real estate broker. The deal highlights why Blackstone joined Axial—to bridge the gap between its lower middle market interests and smaller advisors or banks who may not otherwise know who to contact within the firm. Axial enabled that connection, resulting in a successful transaction outside of Blackstone’s typical sourcing networks.

–

| Transaction Date | Business Details | Revenue | EBITDA |

| June 2025 | Computer Hardware Consulting Services | $11.3M | $800K |

| July 2023 | Supplier of Payment Equipment | $19.2M | $3.6M |

| November 2022 | IT Managed Services | $2.7M | $916K |

| August 2022 | Power Protection Products Supplier | $4.4M | $270K |

| December 2021 | Distributor of Server Racks & Cabinets | $13.0M | $2.0M |

A Dallas-based private equity firm with a team of just ten professionals has closed five transactions through Axial since 2021, targeting lower middle market companies across services, distribution, manufacturing, and tech-enabled sectors. The firm leverages Axial to access a steady pipeline of qualified opportunities that align with its strategy of providing liquidity to founders and supporting long-term growth in scalable businesses.

| 8 Figure Funds | 9 Figure Funds | 10 Figure Funds |

|---|---|---|

|

|

|

|

|

|

|

|

|

|

|

|

|