How Coronavirus Is Impacting Lower Middle Market M&A Activity

Last week, Axial convened a virtual roundtable of members to review the impact of the coronavirus pandemic on lower middle…

Tags

If you are a private equity investor, you hold your portfolio companies accountable for results, and challenge them to optimize their processes to maximize those results. One of the most impactful levers an operating company has in driving toward these results (in most cases some predetermined growth target) is its sales and marketing operation.

Perhaps one of the most ironic things about the modern private equity philosophy is that so many general partners hold their portfolio companies accountable for best-in-class sales and marketing discipline — but then as a private equity firm, spend very little of their time thinking about their own pipeline and process with the same kind of systemization and rigor.

Until recently, there has been no real focus amongst private equity firms on becoming operationally excellent or disciplined from a business development perspective. And while handshakes and traditional networking are still very meaningful in private equity dealmaking, the most successful firms are formalizing business development functions — bolstered by better technology, greater sophistication, and a more institutionalized middle-market GP community.

Recently, Axial founder and CEO Peter Lehrman participated in a webinar hosted by Buyouts magazine about how PE can improve deal sourcing. Here are some of his insights.

We talk a lot with our clients about the concept of the “long tail” of sellers. There’s great data that comes out each year from Sutton Place detailing the universe of intermediaries and the number of deals they bring to market each year. The latest data shows that 70% of intermediaries completed three or less transactions in 2015. According to Sutton Place, on average, private equity firms see just under 19% of their target market deal flow. And when talking about boutique coverage, that coverage drops to 12%.

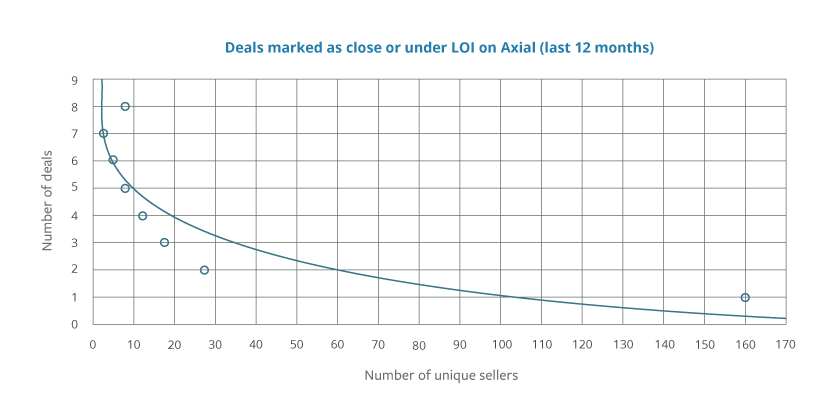

To limit this type of study to the lower middle market, we took a look at deals that either went into LOI or closed on Axial over the last 12 months (deals on Axial typically range from $500k to $15m in EBITDA).

The trend holds: very few organizations bring to market, let alone close, a large number of deals. Our data shows that only 9 investment banks have closed 8 transactions or more, while over 160 unique sellers have gone into LOI or closed a single transaction. And this is just in the last 12 months only for deals marketed on Axial alone.

What does this mean for principal investors? You cannot rely on a small number of relationships to give you the kind of broad coverage you need to ensure you see every deal in a particular industry, deal size, etc.

If you want to be investing in lower middle market companies ($500k to $15m in EBITDA) in even just a handful of industries, you have to have a framework and a strategy for how you are going to be found by these intermediaries at the right points in time.

It’s not a good use of investors’ time to be meeting with them once a month, if they are only doing one deal a year. That time should be spent elsewhere. You have to think about how to economize your time with this set of folks.

One of the first attempts to organize a business development strategy is to set priorities around the types of intermediaries a team needs to cover. To do this, a lot of our clients tend to bucket about intermediaries into three tiers.

We encourage our private equity clients to think about BD as the equivalent of their portfolio company’s sales and marketing operation.

Just as with a proper sales and marketing operation, there are several essential characteristics to an effective and ultimately successful BD operation.

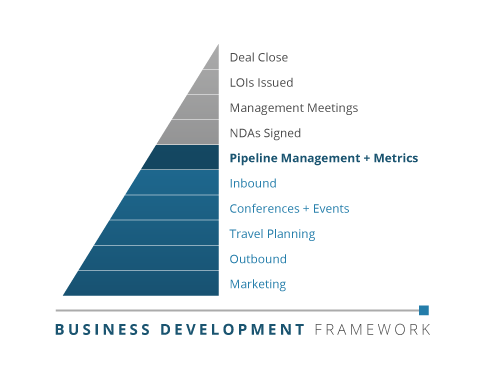

Every firm needs a framework that takes these three ideas into consideration and organizes the activity of a firm’s business development operation accordingly. What we find in working with our clients is that all too often, firms are focused on only the tip of the iceberg, i.e., the deal close.

If you are marketing to LPs or out talking about your metrics, the grey activities in the framework above is what you talk about: the flow of NDAs, number of management meetings held, LOIs signed, and deals closed. What gets much less focus is what we present in blue. These are the activities that occur underneath the surface and lay the foundation for the more visible, more scrutinized tip of the pyramid.

Here’s where GPs can take a page from the sales and marketing playbook. The activities that shape the bottom of the pyramid mirror the organization of a best-in-class sales and marketing department, with roles, resources, and investment dedicated towards the following key activities:

For private equity firms, there’s a lot to learn from a framework that has long been in place in the sales and marketing industry and most likely, is being employed by the leaders of their operating companies. Translating and incorporating these practices into the context of business development, deal sourcing, and pipeline management can become a tremendous competitive advantage for firms who are competing with many traditionally-minded investors in an fragmented but increasingly influential universe of intermediaries.