The Middle Market Review Insights on the Middle Market.

Thanks for subscribing!

Fragmented Capital Markets: What Does it Mean for Dealmakers?

Question: Assume that we define the middle market as deals between $10mm and $250mm. Assume, also, that we define an intermediary as a banker, broker, or advisor that represented a seller in a transaction. In addition, we limit ourselves to North America (i.e., the United States and Canada). How many advisors do you think closed a middle market deal in 2013?

- Fewer than 101

- 101 to 200

- 201 to 400

- 401 to 600

- More than 600

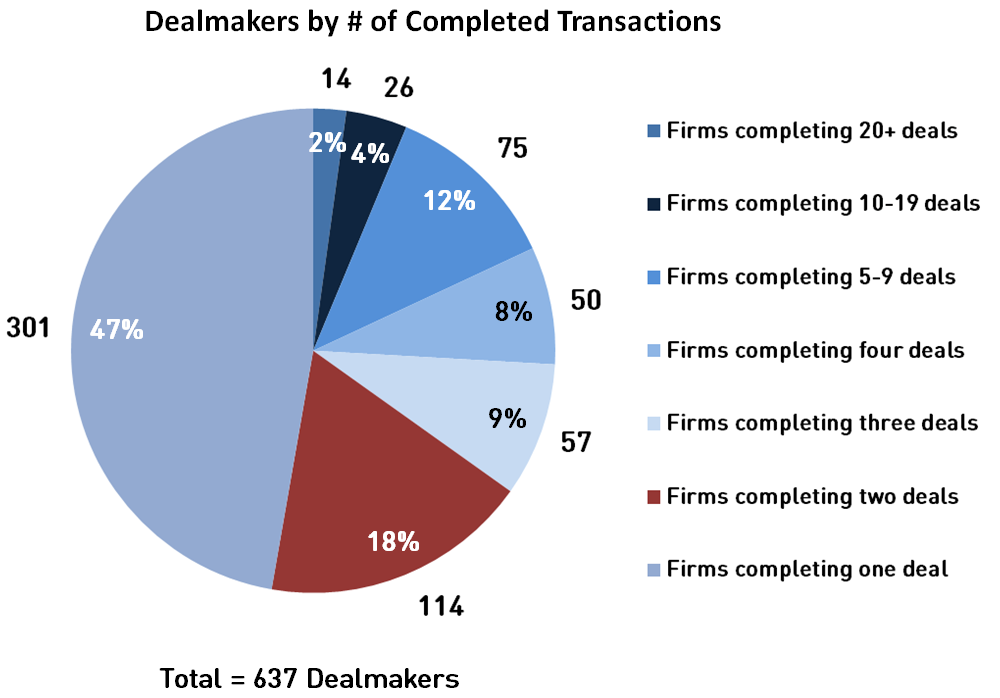

The answer was not 100 or even 300. Rather, there were 637 intermediaries that closed a middle market sellside transaction last year, evidenced by data compiled by Sutton Place Strategies (“SPS”), a deal-sourcing intelligence specialist.

Among these advisors you’ll find the staples, like Raymond James and Houlihan Lokey, each of which closed 41 deals last year.

Importantly however, there are also over 300 intermediaries that closed just one transaction last year. Indeed if you take a look at the distribution, more than 70% of players executed no more than 3 transactions over the last twelve months. What this illustrates is that there’s an extremely high degree of dispersion in the space.

Exhibit A: Dealmakers by # of Completed Transactions

What Are the Pros and Cons?

When market makers (i.e., advisors, brokers, bankers) are distributed so thinly across a limited body of investment opportunities, it makes it very challenging for a fund to capture a wide breadth of deal flow. The more fragmented the universe of deal sources and channels, the harder it becomes to touch them all. Case in point, SPS found in the same data set that middle market funds, on average, see only 23% of their target market deal flow.

Moreover, the current constraints in deal quality and quantity have been explicitly identified as a primary concern for funds in 2014. Two weeks ago, the BDO, a middle market authority, reported that 34% of fund managers identified the ability to find quality targets as their number one challenge in 2014. This is up 6% from last year’s figure, and is driven by exacerbating concerns about dealflow in the wake of a slow year for sourcing.

The combination of (1) a lack of marketplace consolidation and (2) an unmet demand for higher quality investment opportunities certainly does not position deal professionals for easy success.

Notwithstanding the above however, where there exists a lack of clarity in the marketplace, the reality that things inevitably fall through the cracks creates unique opportunities for those that think more creatively than the pack.

Under these market dynamics, a fund that utilizes strategies to source deals in a scalable way will detect investment opportunities that others can’t find.

How Do You Find Deals that Others Don’t See?

What does this kind of “distinguishing” tactic look like? To begin, investment firms will often use a database tool (e.g., Capital IQ, Factset, etc.) to filter companies. However while this enables them to screen deals, it’s also what everyone else is already doing. On the other hand, cold calling (e.g., the sourcing model) is a proven way to comb the landscape for proprietary deals, but is not scalable.

How then can a PE fund, mezzanine provider, growth investor, corporate lender, family office or independent sponsor improve both the quality and quantity of deals that they source? The answer, we believe, lies in networks. Let us explain why.

The core trend here is that whenever there exists marketplace dispersion, increased interconnectedness will typically accelerate efficiency and reduce costs for all parties.

For example, in the short-term apartment rental sector, the entry of products like Airbnb has increased options for apartment owners and improved pricing for subletters. Similarly in the job search market, the introduction and subsequent development of LinkedIn has amplified employment success for job seekers and close rates for recruiters.

The critical similarity between these two sectors and the private capital markets is the paired presence of a huge number of players plus a high degree of dispersion.

Our argument is that those tools that have the potential to deliver (a) access to a large swath of deals, (b) a wide spectrum of deal quality (meaning both auctioned and proprietary transaction opportunities) and (c) scalability are those that will set the winning investment professionals apart from the herd.

Learn More About Joining Axial

Subscribe to Middle Market Review