Top 25 Lower Middle Market Investment Banks | Q2 2026

Axial is excited to release our Q2 2026 Lower Middle Market Investment Banking League Tables. To compile this list, we…

Since 2022, Axial has surveyed M&A advisors, investment bankers, and business brokers in its network to track how fee structures and engagement practices are evolving across the lower middle market. The goal is simple: bring greater transparency to a market where advisory fees and engagement practices are often difficult to compare.

The 2026 edition is based on 331 responses from M&A advisors collected in Q2 2026. Participants were asked about their most commonly used fee structures, engagement terms, and the market conditions shaping their advisory practices.

The findings above highlight a few of the most notable trends from this year’s survey, but they only scratch the surface. The full 2026 M&A Fee Guide includes detailed benchmarking data on engagement fees, success fee structures, capital raising mandates, expense reimbursement policies, and advisor perspectives on the opportunities and challenges shaping today’s deal environment.

Axial’s exit consultants introduce you to the right M&A advisor to help you secure the best terms for your business sale. With more than 16 years of unparalleled access to the small business M&A landscape, we have the largest network of pre-vetted M&A advisors and the right resources to guide you through every step of your exit journey.

Below are select results from this year’s survey, followed by perspectives from M&A advisors who reviewed an advance copy of the guide and shared their thoughts on the report’s biggest surprises, expected trends, and overarching themes.

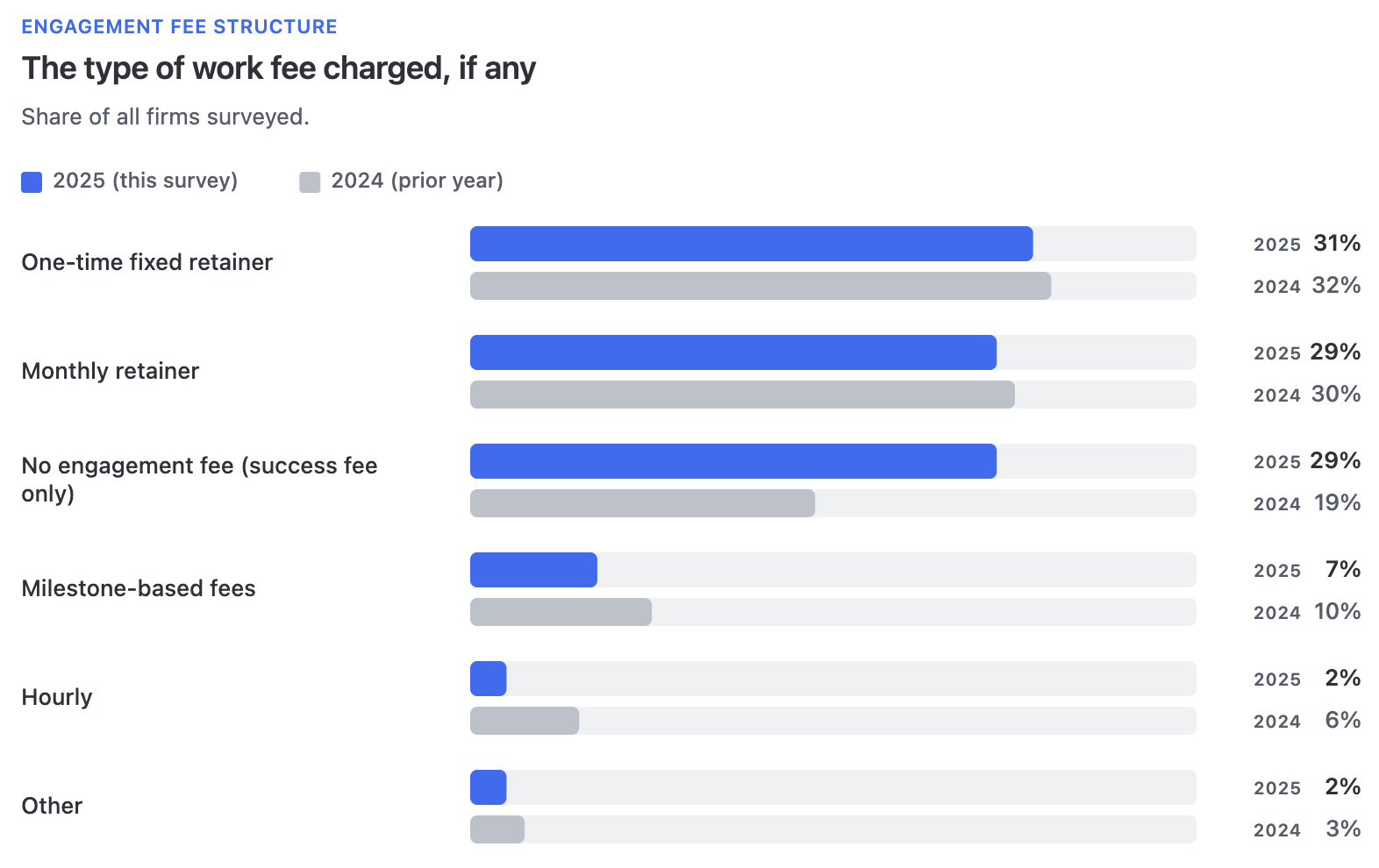

The biggest shift in engagement fee structure this year is the rise of success-fee-only arrangements. Nearly a third of survey respondents now charge no upfront work fee at all, up from 19% in 2024. Meanwhile, one-time fixed retainers (31%) and monthly retainers (29%) held roughly steady year over year.

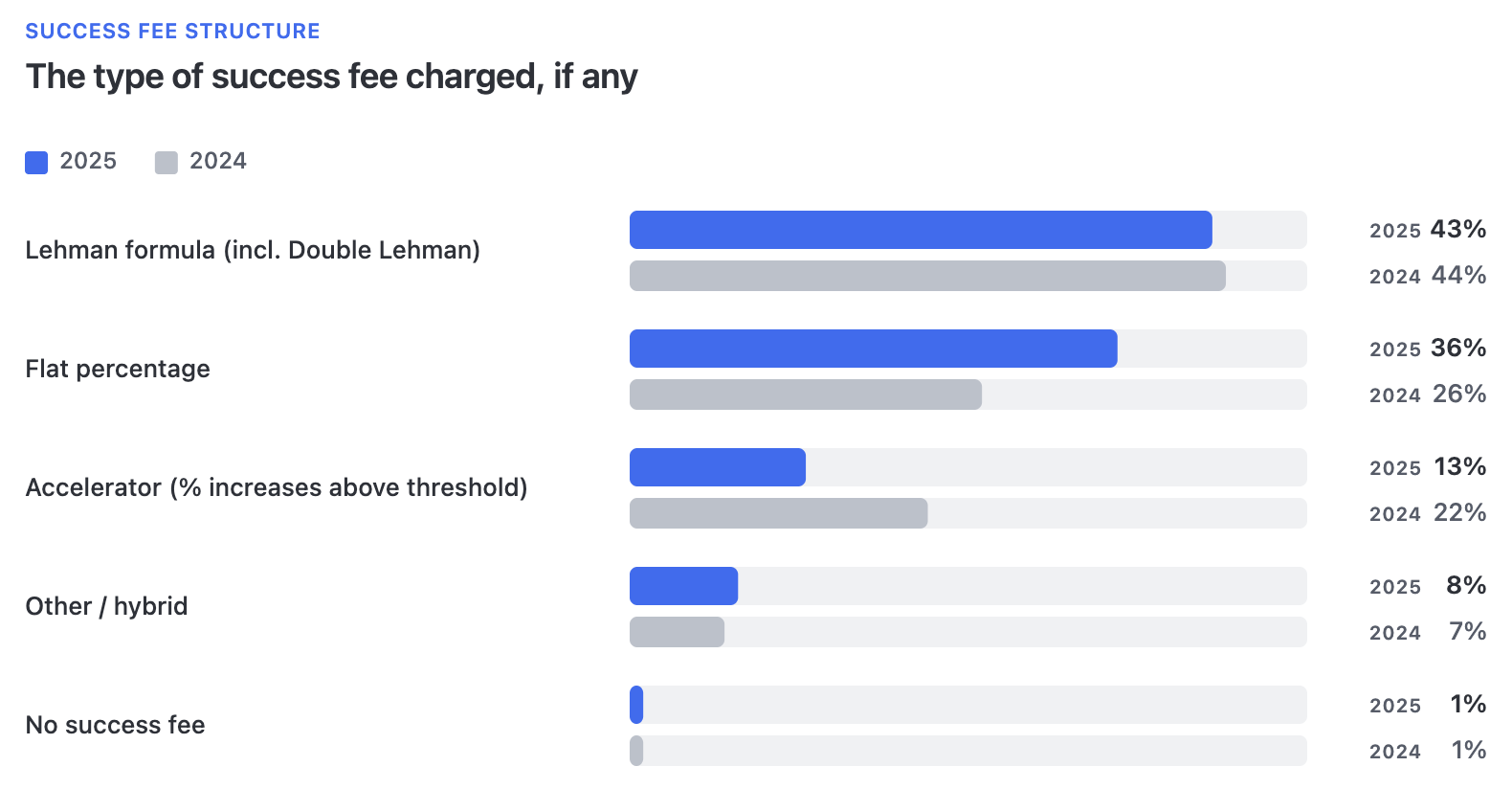

Success fee structures remain concentrated around two approaches: Lehman-style formulas and flat-percentage arrangements. Together, these structures account for 79% of survey responses, while accelerator models and hybrid approaches represent a much smaller share.

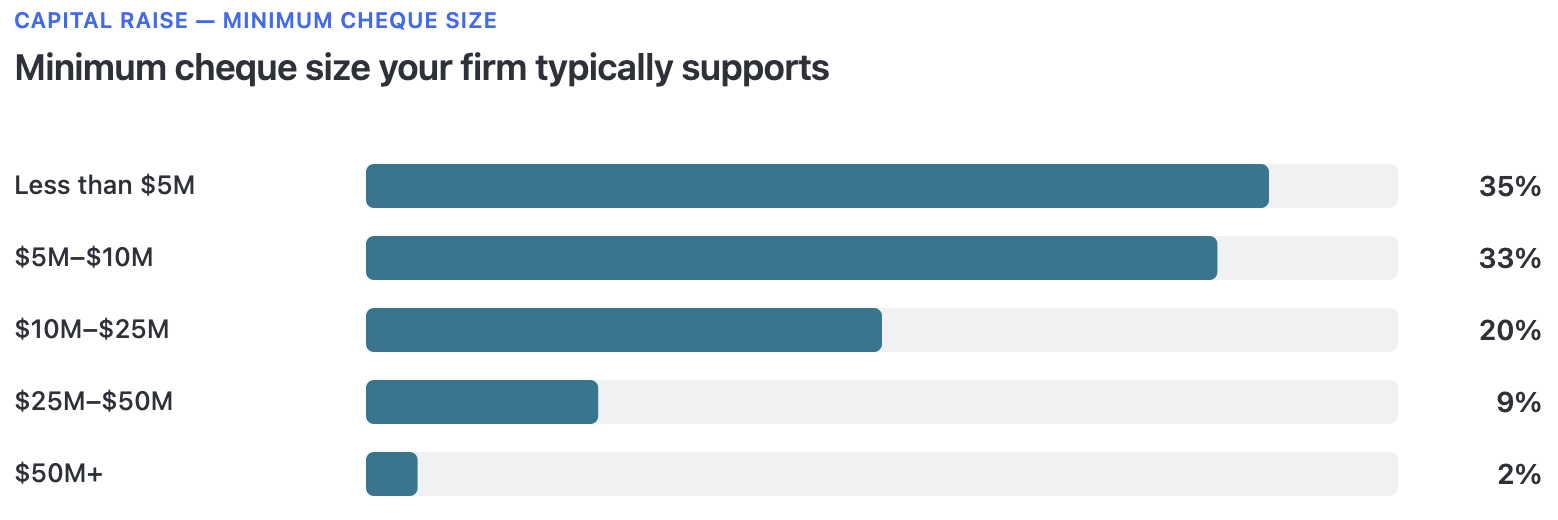

Capital raising mandates among survey respondents tend to skew toward smaller transaction sizes. More than two-thirds (68%) of respondents reported a typical minimum cheque size of less than $10 million. Only 11% reported a minimum cheque size of more than $25 million.

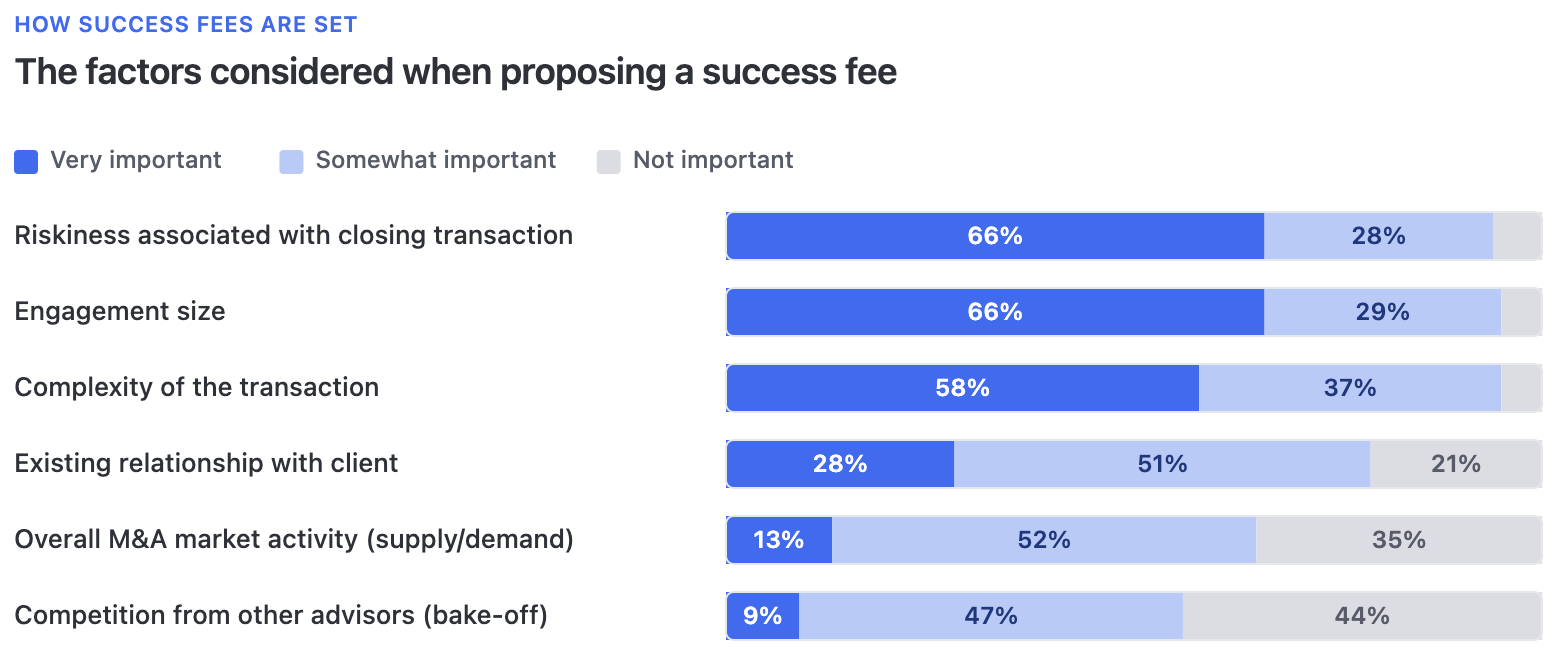

Success fees are primarily driven by deal-specific considerations rather than external market factors. Among survey respondents, transaction risk, engagement size, and deal complexity ranked as the most important inputs when proposing a success fee, while overall M&A market activity and competitive pricing pressure ranked near the bottom.

To add context to this year’s findings, Axial shared an advance copy of the 2026 M&A Fee Guide with a group of participating advisors and asked for their reactions. Their responses highlight many of the same themes reflected in the survey data: increased competition, longer deal timelines, growing fee pressure, and the evolving role of AI in the M&A process.

“The jump in success-fee-only arrangements. Nearly a third of advisors now work without upfront fees, up from 19% last year. The report also notes that deals are taking longer, falling apart more often, and requiring significantly more hands-on process management. Those two trends are in tension. An advisor accepting 100% fee-at-close in a market where close rates are declining is making a significant bet.”

– Joe Surber, BluGrowth Partners

“I’m surprised to see such a large percentage of firms using a flat fee or decreasing rate. Some of our most successful opportunities and happiest clients have had an accelerating-rate fee. It aligns our success with our clients’ and creates a more exciting, competitive internal atmosphere as the deal size (and fee size) increases.”

– Drew Langford, Trailhead Partners

“Seeing the impact of valuation gaps wasn’t a shock at all. Advisors pointing out wide bid-ask spreads—with buyers staying disciplined while sellers anchor to older, pre-uncertainty valuations—is exactly what we are dealing with on a daily basis right now.”

– Van Moody, Lion Business Brokers

“We are not at all surprised by the changes AI is having on the marketplace in terms of widening the buy-sell valuation gap. Sellers are becoming more comfortable using AI to substitute for bona fide business valuations. Advisors are now having to spend more time justifying their valuations and price expectations while also establishing credibility with sellers.”

– Josh Matte, XPS Group

“I’m not surprised to find over a quarter of firms charging breakup fees. Owners are inundated with outreach from buyers and intermediaries, causing many to keep one foot out the door and believe a better option may be just around the corner. In reality, we know how fickle most proprietary offers really are.”

– Drew Langford, Trailhead Partners

“The broader takeaway I see is that the market is becoming more competitive and more complicated at the same time. Deals are harder to close, sellers are often less prepared, buyers are more disciplined, and AI is creating both confusion and pricing pressure. Yet success fees are holding up, which tells me that real execution still matters. The advisors who can prepare owners, defend value, manage diligence, and find the right buyer will continue to be worth their fee.”

– Brian Stephens, Legacy Venture Group

“The main takeaway is that advisors are simplifying their structures to get deals signed. While Lehman formulas are still the most common, seeing flat-percentage fees rise from 26% to 36% shows a shift toward cleaner alignment with founders. Additionally, the fact that 77% of advisors deduct engagement fees from the final success fee shows this is now the definitive market standard.”

– Van Moody, Lion Business Brokers

“While AI is impacting our clients’ business and, to some extent, our business, I do not expect a change in fees or other terms of our engagements anytime soon, other than to lower or eliminate retainers, which were justified by the labor-intensive nature of some of the advisor’s activities.”

– Cristian Anastasiu, Excendio Advisors

“I have been doing sell-side M&A for two decades. At the end of the day, hunters eat steak and farmers eat corn. If you are waiting for the phone to ring, or expect AI to magically increase your deal flow, enjoy your corn.”

– Jack Farris, Farris Capital Partners

Access the full report for additional benchmarking data on engagement fees, success fee structures, capital raising mandates, and engagement terms.